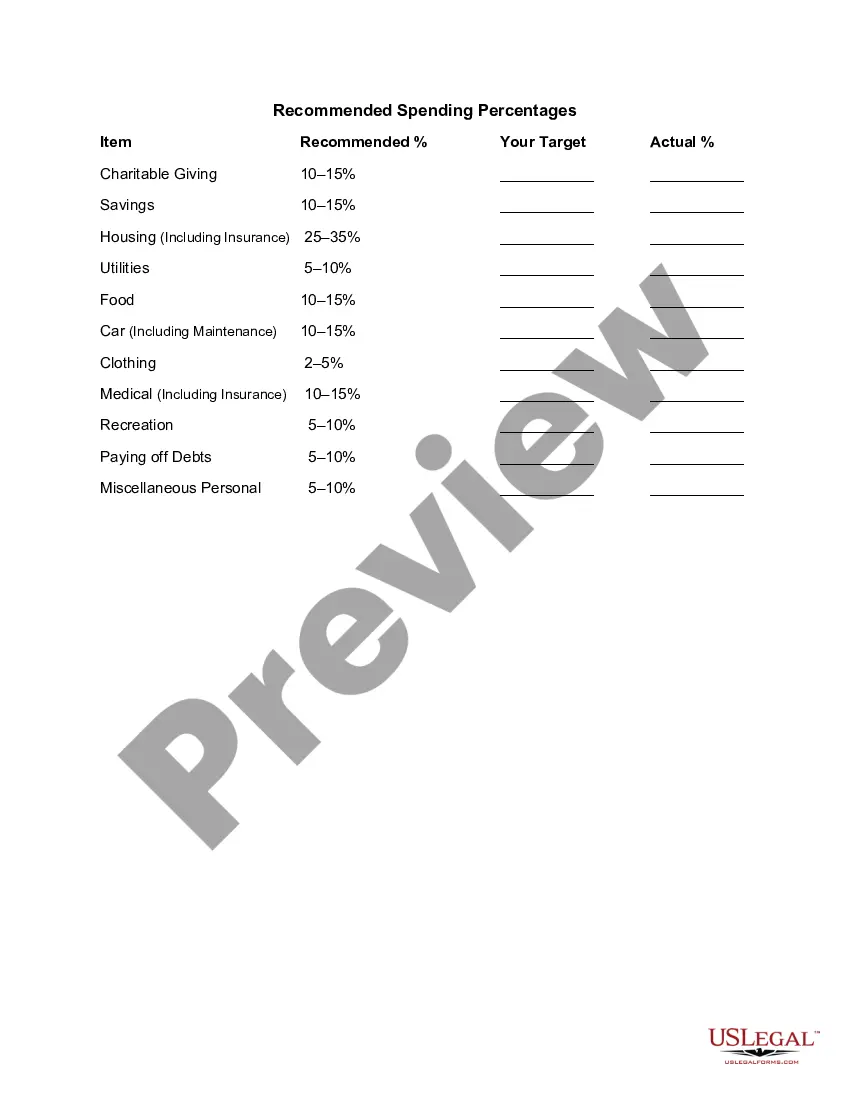

Idaho Recommended Spending Percentages serve as a financial guideline for individuals and households in the state of Idaho. These percentages are designed to help residents allocate their income effectively and responsibly, ensuring a balanced budget and financial stability. By following these recommendations, individuals can achieve financial goals, manage debt, and avoid overspending. One of the primary types of Idaho Recommended Spending Percentages is the "50-30-20 Rule." This rule suggests allocating 50% of income towards essential expenses, 30% towards discretionary expenses, and 20% towards savings and debt repayment. Essential expenses may include housing, utilities, transportation, groceries, and healthcare. Discretionary expenses cover items like dining out, entertainment, vacations, and non-essential shopping. The remaining 20% should be dedicated to building an emergency fund, paying off debt, or investing for the future. Additionally, Idaho Recommended Spending Percentages may include guidelines for specific categories, such as housing, transportation, and healthcare. For example, it is commonly advised that housing costs should not exceed 30% of an individual's income, including rent or mortgage payments, property taxes, insurance, and maintenance. Transportation expenses should ideally stay within 15-20% of income, including car payments, fuel, insurance, and maintenance. Healthcare expenses, which can vary greatly depending on personal circumstances, are typically recommended being around 5-10% of income. Following these Idaho Recommended Spending Percentages helps individuals maintain a healthy financial balance, avoid excessive debt, and work towards long-term financial stability. However, it's important to note that these percentages are not strict rules but rather general guidelines. Personal circumstances and priorities may require adjustments to these recommendations. Additionally, seeking professional financial advice or utilizing budgeting tools can provide more customized guidance based on one's specific situation.

Idaho Recommended Spending Percentages

Description

How to fill out Idaho Recommended Spending Percentages?

US Legal Forms - among the greatest libraries of lawful kinds in America - provides an array of lawful file layouts you may down load or print out. Utilizing the site, you will get a large number of kinds for enterprise and person purposes, categorized by groups, claims, or search phrases.You will discover the most up-to-date versions of kinds such as the Idaho Recommended Spending Percentages within minutes.

If you have a monthly subscription, log in and down load Idaho Recommended Spending Percentages from your US Legal Forms local library. The Acquire switch will show up on each kind you view. You gain access to all in the past saved kinds inside the My Forms tab of your own accounts.

If you wish to use US Legal Forms the very first time, listed here are easy guidelines to obtain started:

- Be sure to have selected the right kind for your personal city/county. Go through the Preview switch to examine the form`s content. Read the kind description to actually have chosen the right kind.

- If the kind doesn`t fit your needs, utilize the Research industry near the top of the display to find the the one that does.

- Should you be content with the shape, affirm your decision by clicking the Purchase now switch. Then, choose the prices strategy you like and supply your qualifications to sign up for the accounts.

- Method the transaction. Make use of Visa or Mastercard or PayPal accounts to complete the transaction.

- Choose the format and down load the shape in your product.

- Make changes. Complete, revise and print out and indication the saved Idaho Recommended Spending Percentages.

Each and every template you added to your bank account does not have an expiration particular date and it is your own property permanently. So, in order to down load or print out another copy, just proceed to the My Forms area and click on around the kind you will need.

Obtain access to the Idaho Recommended Spending Percentages with US Legal Forms, the most extensive local library of lawful file layouts. Use a large number of skilled and status-specific layouts that meet up with your company or person needs and needs.