Idaho Challenge to Credit Report of Experian, TransUnion, and/or Equifax

Description

How to fill out Challenge To Credit Report Of Experian, TransUnion, And/or Equifax?

If you want to full, download, or print authorized document templates, use US Legal Forms, the biggest selection of authorized types, which can be found on-line. Utilize the site`s simple and convenient search to find the files you require. Numerous templates for company and person uses are categorized by groups and states, or keywords and phrases. Use US Legal Forms to find the Idaho Challenge to Credit Report of Experian, TransUnion, and/or Equifax in a few mouse clicks.

When you are previously a US Legal Forms consumer, log in to the account and then click the Download button to get the Idaho Challenge to Credit Report of Experian, TransUnion, and/or Equifax. Also you can entry types you formerly delivered electronically inside the My Forms tab of your account.

If you are using US Legal Forms the first time, follow the instructions below:

- Step 1. Make sure you have selected the form for your right town/land.

- Step 2. Utilize the Review method to examine the form`s information. Never forget to read through the information.

- Step 3. When you are unhappy together with the kind, utilize the Look for industry near the top of the monitor to find other types in the authorized kind web template.

- Step 4. After you have identified the form you require, select the Purchase now button. Select the costs prepare you choose and include your accreditations to register for the account.

- Step 5. Procedure the purchase. You can use your charge card or PayPal account to perform the purchase.

- Step 6. Find the formatting in the authorized kind and download it on your own product.

- Step 7. Full, edit and print or indicator the Idaho Challenge to Credit Report of Experian, TransUnion, and/or Equifax.

Every authorized document web template you get is the one you have for a long time. You have acces to each and every kind you delivered electronically in your acccount. Click the My Forms section and select a kind to print or download again.

Be competitive and download, and print the Idaho Challenge to Credit Report of Experian, TransUnion, and/or Equifax with US Legal Forms. There are many professional and state-distinct types you can use to your company or person demands.

Form popularity

FAQ

More companies use Experian for credit reporting than use Equifax. This alone does not make Experian better, but it does indicate that any particular debt is more likely to appear on an Experian reports.

To freeze your credit, you have to contact each of the three credit bureaus individually. Placing a credit freeze is free for you and your children, as is lifting it when applying for new credit.

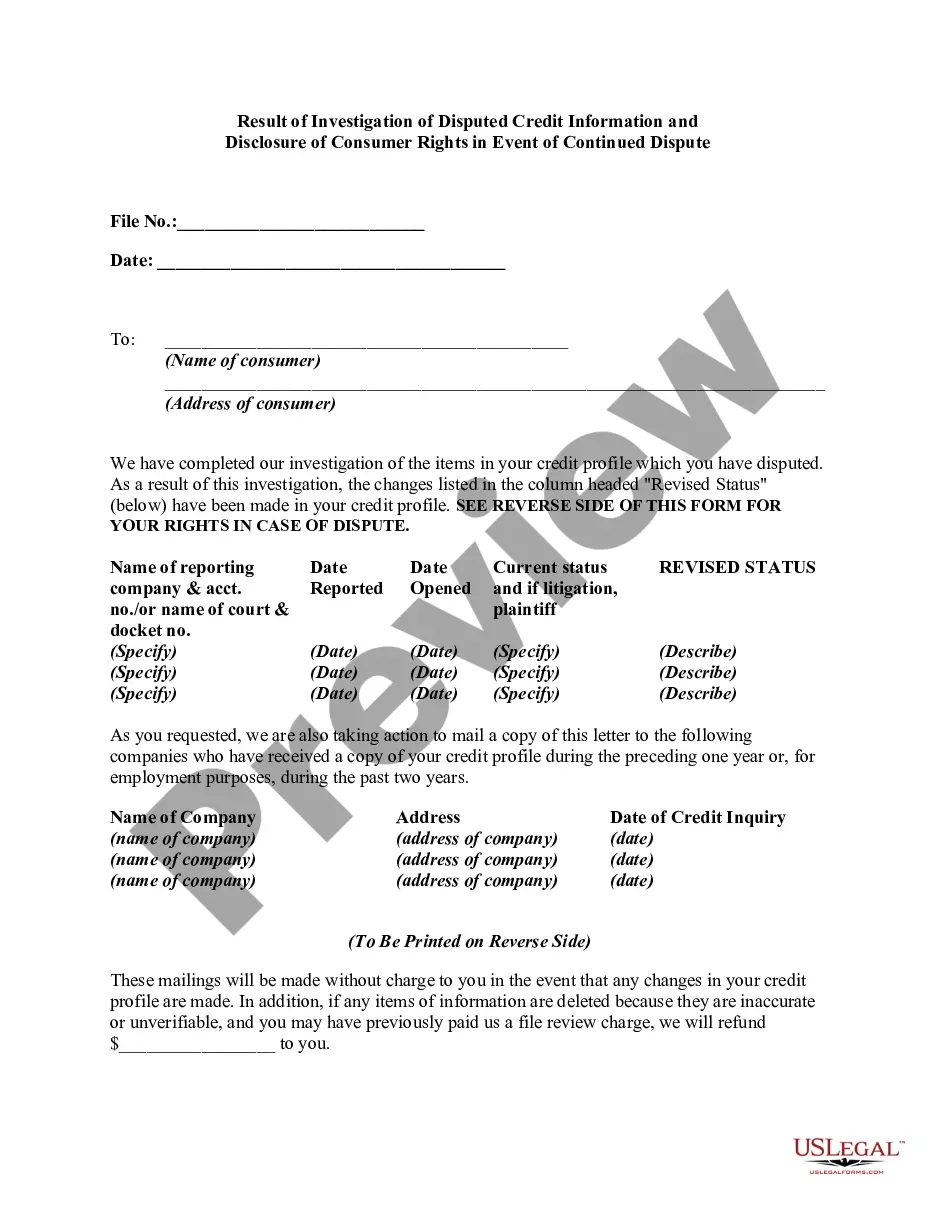

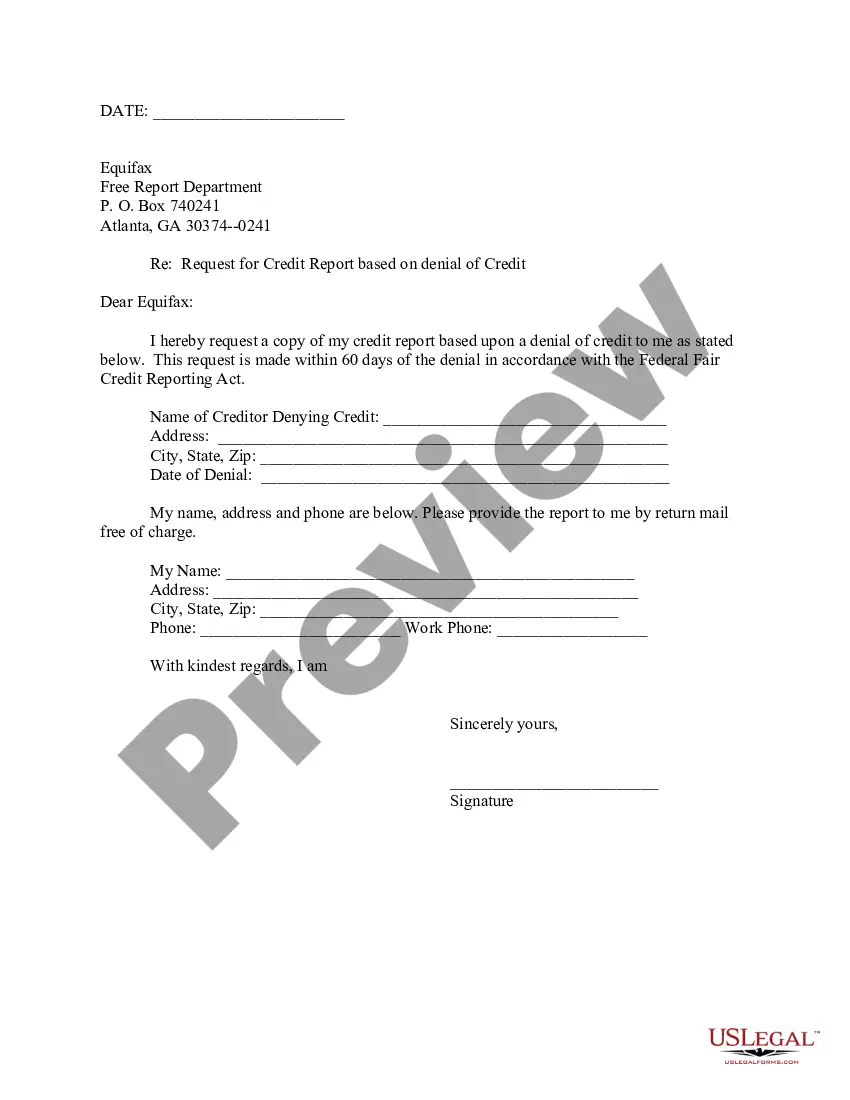

If you identify an error on your credit report, you should start by disputing that information with the credit reporting company (Experian, Equifax, and/or Transunion). You should explain in writing what you think is wrong, why, and include copies of documents that support your dispute.

FICO ® Scores are the most widely used credit scores?90% of top lenders use FICO ® Scores. Every year, lenders access billions of FICO ® Scores to help them understand people's credit risk and make better?informed lending decisions.

When you are applying for a mortgage to buy a home, lenders will typically look at all of your credit history reports from the three major credit bureaus ? Experian, Equifax, and TransUnion. In most cases, mortgage lenders will look at your FICO score. There are different FICO scoring models.

Although Experian is the largest credit bureau in the U.S., TransUnion and Equifax are widely considered to be just as accurate and important.

Lenders typically use your FICO® Score to gauge your creditworthiness. Compared to TransUnion's algorithm, Equifax's algorithm more closely resembles the FICO® model. Therefore, your Equifax score may better predict whether you'll qualify for a loan. Your Equifax score won't be a tell-all, though.

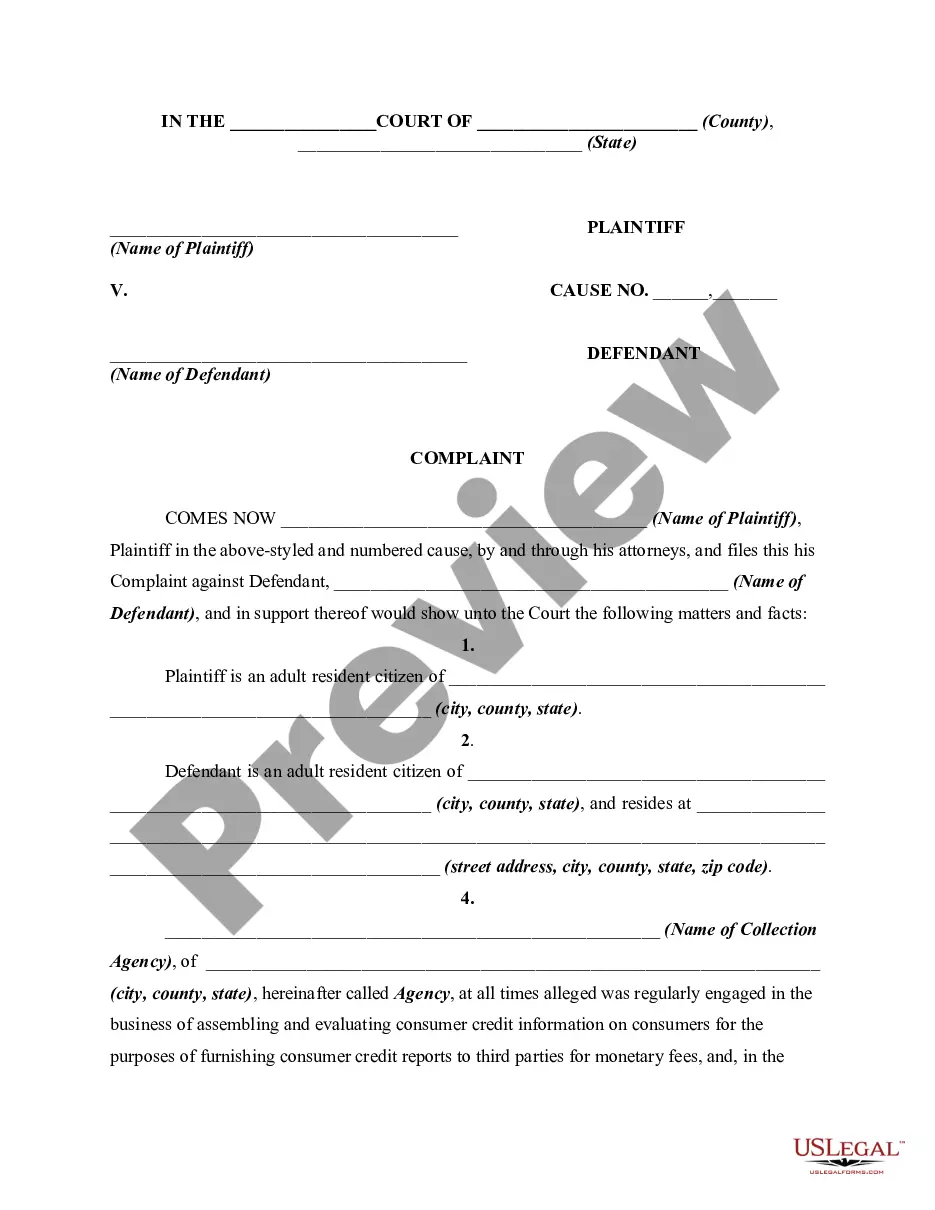

The law was passed in 1970 and amended twice. It is primarily aimed at the three major credit reporting agencies ? Experian, Equifax and TransUnion ? because of the widespread use of the information those bureaus collect and sell.