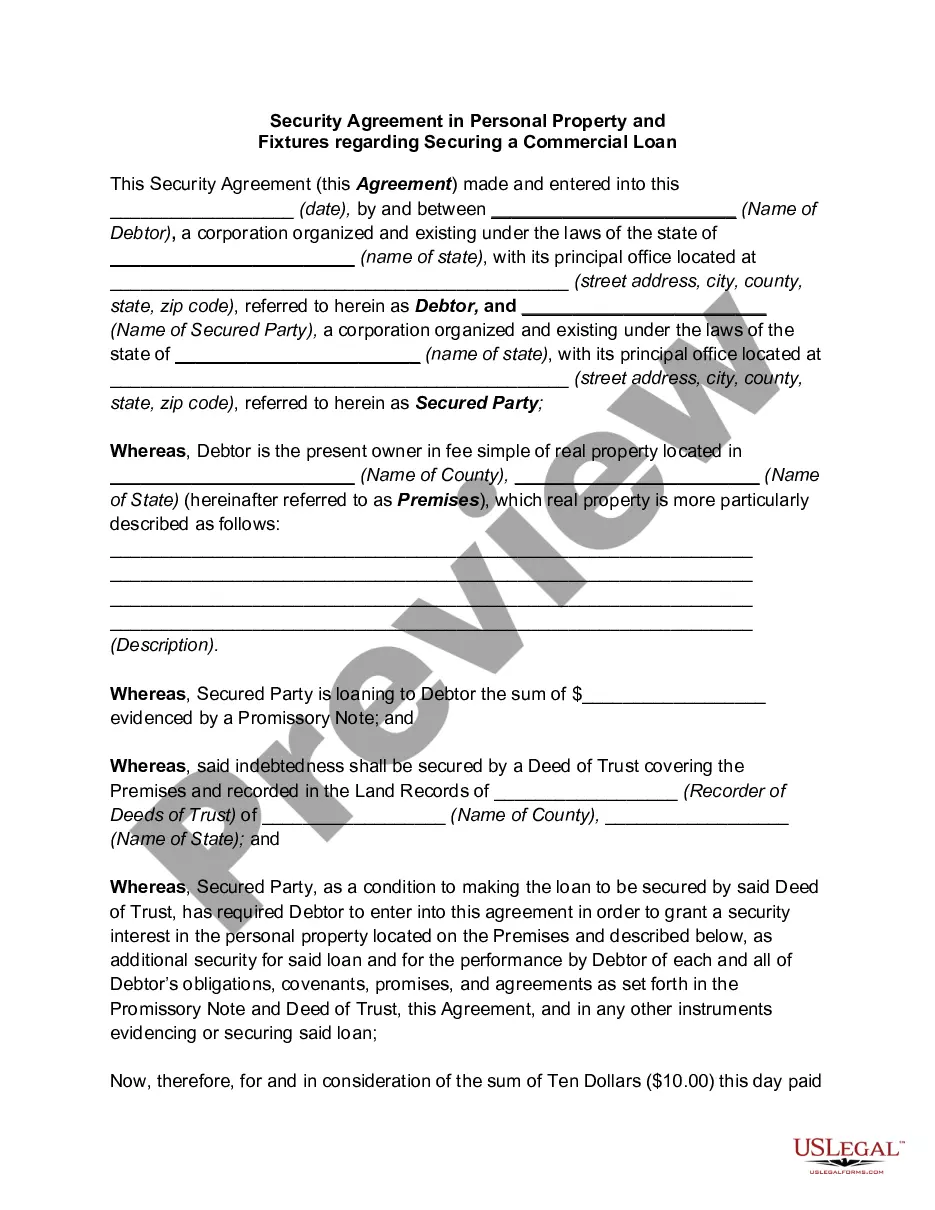

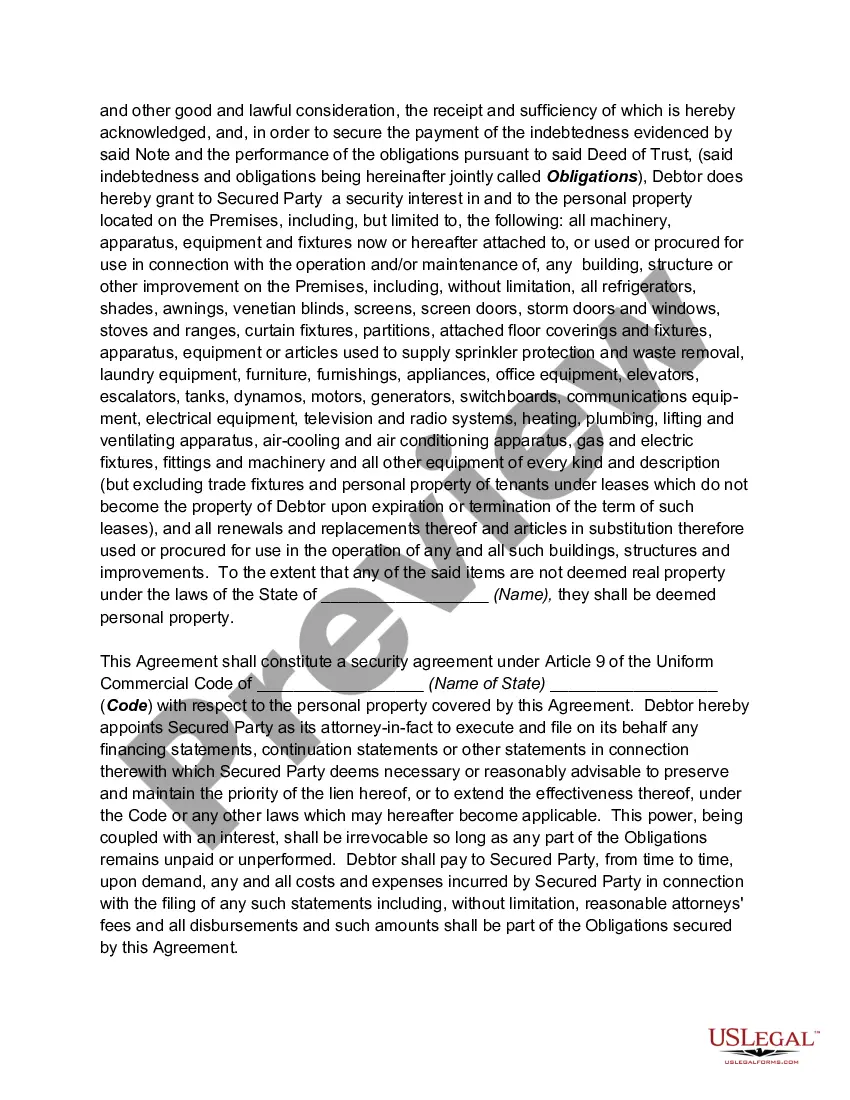

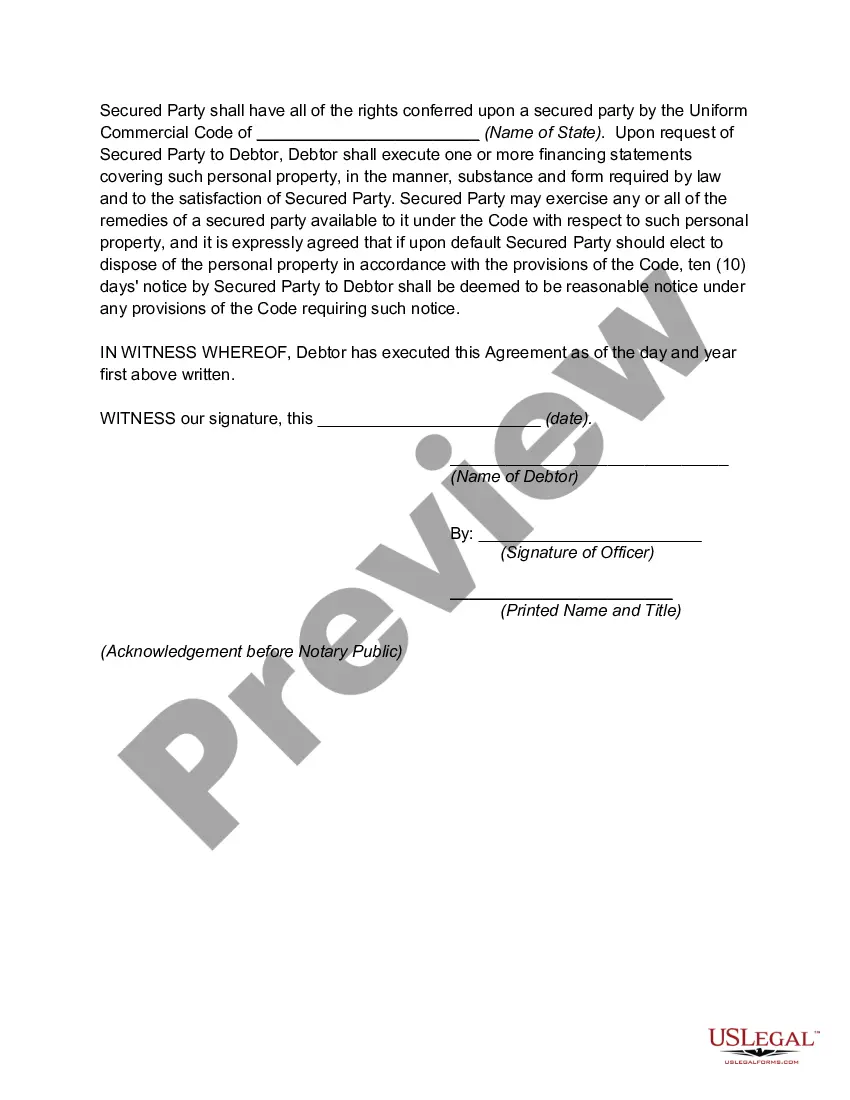

Idaho Security Agreement in Personal Property Fixtures is a crucial legal document that plays a significant role in securing a commercial loan. This agreement involves the pledge of personal property fixtures as collateral, ensuring the lender's interest if the borrower defaults on loan repayment. The following are the different types of Idaho Security Agreement in Personal Property Fixtures relevant to securing a commercial loan: 1. Real Estate Security Agreement: This type of security agreement involves fixtures attached to the real property that serves as collateral for the commercial loan. It includes permanently installed machinery, equipment, or structures that contribute to the property's functionality. 2. Chattel Security Agreement: Chattel is movable personal property such as furniture, inventory, or vehicles used for commercial purposes. In this type of agreement, the borrower pledges their chattel as collateral for the loan, providing an additional layer of security for the lender. 3. Equipment Security Agreement: This agreement secures the commercial loan by using specific equipment, machinery, or vehicles owned by the borrower as collateral. The lender holds a security interest in the equipment until the loan is fully repaid. 4. Inventory Security Agreement: When a borrower needs a commercial loan and has valuable inventory as part of their business, they may use it as collateral by entering into an inventory security agreement. This agreement grants the lender a security interest in the inventory until the loan is paid off. 5. Accounts Receivable Security Agreement: To secure a commercial loan, businesses with substantial accounts receivable can enter into this type of agreement. Accounts receivable, which represents outstanding payments owed to the business, is pledged as collateral, providing assurance to the lender. It is essential to note that these different types of Idaho Security Agreement in Personal Property Fixtures serve the purpose of securing a commercial loan through varying forms of collateral. Borrowers should carefully review and understand the terms and conditions laid out in each agreement and seek legal guidance to ensure compliance with Idaho laws and regulations.

Idaho Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan

Description

How to fill out Idaho Security Agreement In Personal Property Fixtures Regarding Securing A Commercial Loan?

Have you been inside a situation where you require documents for either company or person uses nearly every day? There are a variety of legitimate file layouts accessible on the Internet, but locating ones you can depend on isn`t simple. US Legal Forms offers a huge number of kind layouts, just like the Idaho Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan, which can be composed to fulfill federal and state demands.

In case you are previously acquainted with US Legal Forms website and get an account, merely log in. Afterward, it is possible to obtain the Idaho Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan web template.

If you do not offer an account and wish to start using US Legal Forms, follow these steps:

- Get the kind you will need and ensure it is to the proper town/region.

- Utilize the Preview button to check the form.

- Browse the explanation to actually have chosen the right kind.

- In case the kind isn`t what you`re seeking, use the Research industry to find the kind that meets your requirements and demands.

- If you get the proper kind, just click Get now.

- Pick the pricing prepare you desire, fill in the specified information and facts to generate your bank account, and buy the transaction with your PayPal or charge card.

- Choose a convenient paper structure and obtain your version.

Locate all the file layouts you possess purchased in the My Forms menu. You can aquire a additional version of Idaho Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan anytime, if needed. Just select the necessary kind to obtain or produce the file web template.

Use US Legal Forms, one of the most considerable assortment of legitimate varieties, to save some time and stay away from blunders. The service offers expertly produced legitimate file layouts that can be used for a range of uses. Generate an account on US Legal Forms and start making your daily life easier.