Idaho Jury Instruction — 10.10.5 Real Estate Held Primarily For Sale is a legal guideline that covers the classification and tax treatment of real estate properties that are primarily held for sale. This instruction is crucial for jury members to understand the parameters on which a property can be categorized as being held primarily for sale and the resulting tax implications. The Idaho Jury Instruction — 10.10.5 Real Estate Held Primarily For Sale is designed to ensure clarity in evaluating whether a property is held primarily for sale or for investment purposes. It helps define the circumstances under which a property can be considered as being held primarily for sale, leading to different tax treatment. Keywords: Idaho, jury instruction, real estate, held primarily, sale, tax treatment, classification, investment, properties. Different Types of Idaho Jury Instruction — 10.10.5 Real Estate Held Primarily For Sale: 1. Residential Properties: This category encompasses single-family homes, townhouses, condominiums, and any other residential property being held primarily for sale. The instruction sheds light on the necessary criteria for determining whether a residential property falls under the "held primarily for sale" classification. 2. Commercial Properties: Commercial properties, such as office buildings, shopping centers, and industrial facilities, can also be held primarily for sale. The instruction establishes the specific factors that should be considered when evaluating whether a commercial property meets the criteria for classification. 3. Land and Development Projects: Apart from built structures, vacant land and real estate development projects can fall under the "held primarily for sale" category. The instruction provides guidance on assessing the intentions, actions, and duration required to classify such properties for tax purposes. 4. Investment Properties: The jury instruction also distinguishes between real estate properties held primarily for investment purposes versus those held primarily for sale. It clarifies the criteria for identifying investments and helps differentiate them from properties intended for resale. 5. Tax Implications: Understanding the tax treatment of real estate held primarily for sale is critical for jury members. The instruction highlights the potential impacts on property taxes, capital gains taxes, and other tax liabilities when a property is deemed to be held primarily for sale. In summary, Idaho Jury Instruction — 10.10.5 Real Estate Held Primarily For Sale provides comprehensive guidelines for jury members to evaluate real estate properties' classification and tax treatment. By considering relevant keywords and covering various property types, this content offers a detailed description of the instruction and its different types.

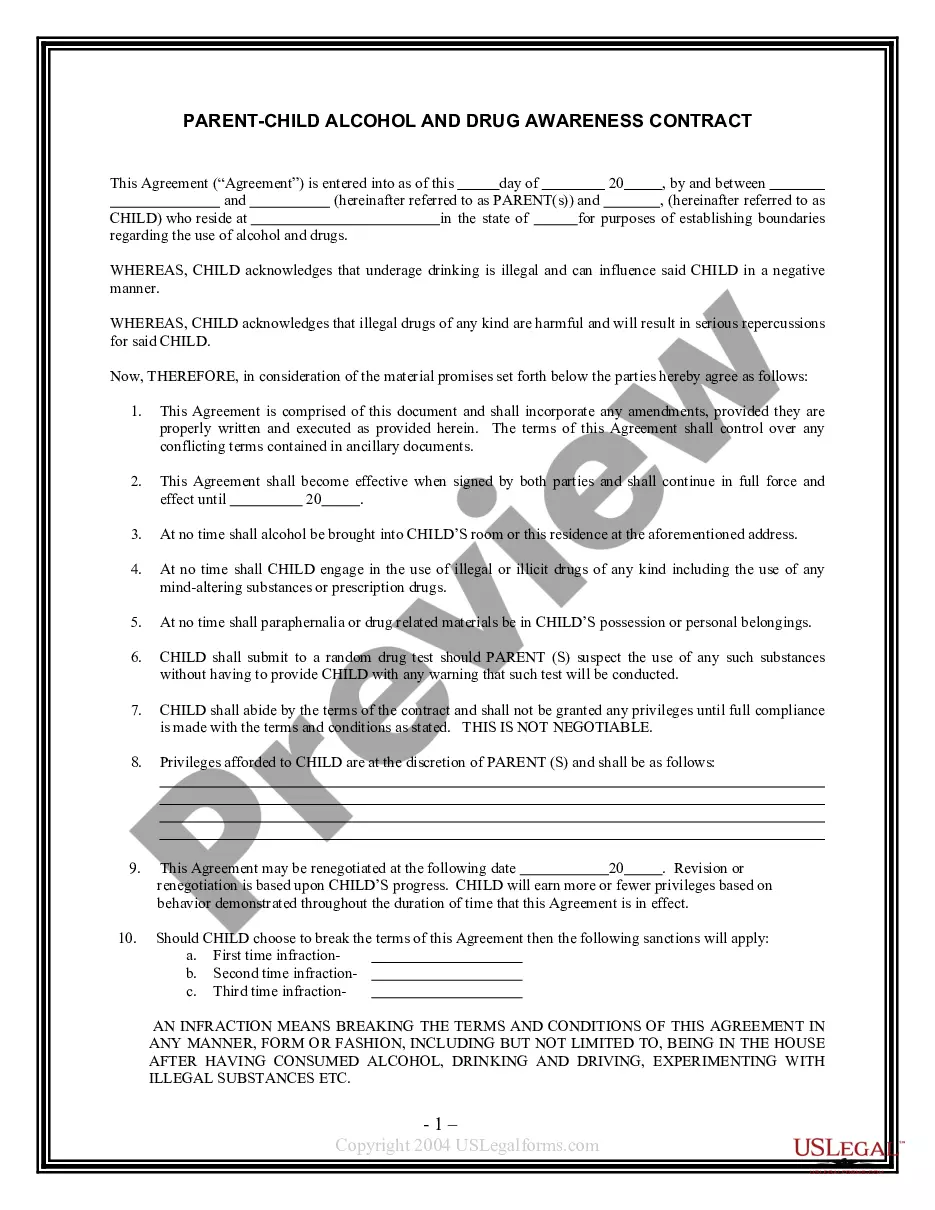

Idaho Jury Instruction - 10.10.5 Real Estate Held Primarily For Sale

Description

How to fill out Idaho Jury Instruction - 10.10.5 Real Estate Held Primarily For Sale?

You can commit several hours online looking for the legal papers design that meets the federal and state specifications you want. US Legal Forms provides 1000s of legal kinds that happen to be examined by specialists. It is possible to acquire or print the Idaho Jury Instruction - 10.10.5 Real Estate Held Primarily For Sale from my services.

If you have a US Legal Forms accounts, it is possible to log in and click the Download key. Following that, it is possible to complete, edit, print, or sign the Idaho Jury Instruction - 10.10.5 Real Estate Held Primarily For Sale. Every single legal papers design you get is yours for a long time. To get an additional version for any bought kind, visit the My Forms tab and click the corresponding key.

If you are using the US Legal Forms internet site initially, stick to the simple guidelines listed below:

- First, make sure that you have chosen the best papers design for your state/area that you pick. Look at the kind outline to ensure you have chosen the appropriate kind. If available, make use of the Preview key to check through the papers design at the same time.

- In order to discover an additional edition of your kind, make use of the Look for industry to obtain the design that suits you and specifications.

- After you have located the design you need, click Acquire now to carry on.

- Select the pricing prepare you need, enter your credentials, and register for a merchant account on US Legal Forms.

- Comprehensive the purchase. You may use your charge card or PayPal accounts to fund the legal kind.

- Select the structure of your papers and acquire it for your device.

- Make modifications for your papers if required. You can complete, edit and sign and print Idaho Jury Instruction - 10.10.5 Real Estate Held Primarily For Sale.

Download and print 1000s of papers templates making use of the US Legal Forms website, that provides the largest collection of legal kinds. Use expert and state-specific templates to tackle your company or person requires.