Idaho Split-Dollar Life Insurance

Description

How to fill out Split-Dollar Life Insurance?

You are able to devote hours online attempting to find the authorized papers template which fits the state and federal demands you will need. US Legal Forms provides thousands of authorized kinds that happen to be analyzed by professionals. It is simple to acquire or produce the Idaho Split-Dollar Life Insurance from your service.

If you already have a US Legal Forms account, you may log in and click the Acquire button. Afterward, you may total, modify, produce, or signal the Idaho Split-Dollar Life Insurance. Every single authorized papers template you acquire is your own property permanently. To acquire yet another version of any obtained develop, proceed to the My Forms tab and click the related button.

If you use the US Legal Forms site the first time, keep to the basic instructions listed below:

- First, ensure that you have selected the right papers template for the county/city of your choosing. Browse the develop information to make sure you have selected the right develop. If available, take advantage of the Preview button to search through the papers template also.

- If you wish to discover yet another model of the develop, take advantage of the Research discipline to discover the template that meets your requirements and demands.

- After you have identified the template you would like, simply click Get now to carry on.

- Choose the costs program you would like, enter your credentials, and register for an account on US Legal Forms.

- Full the transaction. You may use your charge card or PayPal account to fund the authorized develop.

- Choose the format of the papers and acquire it in your product.

- Make modifications in your papers if possible. You are able to total, modify and signal and produce Idaho Split-Dollar Life Insurance.

Acquire and produce thousands of papers web templates using the US Legal Forms web site, which provides the greatest variety of authorized kinds. Use skilled and status-particular web templates to take on your company or person requirements.

Form popularity

FAQ

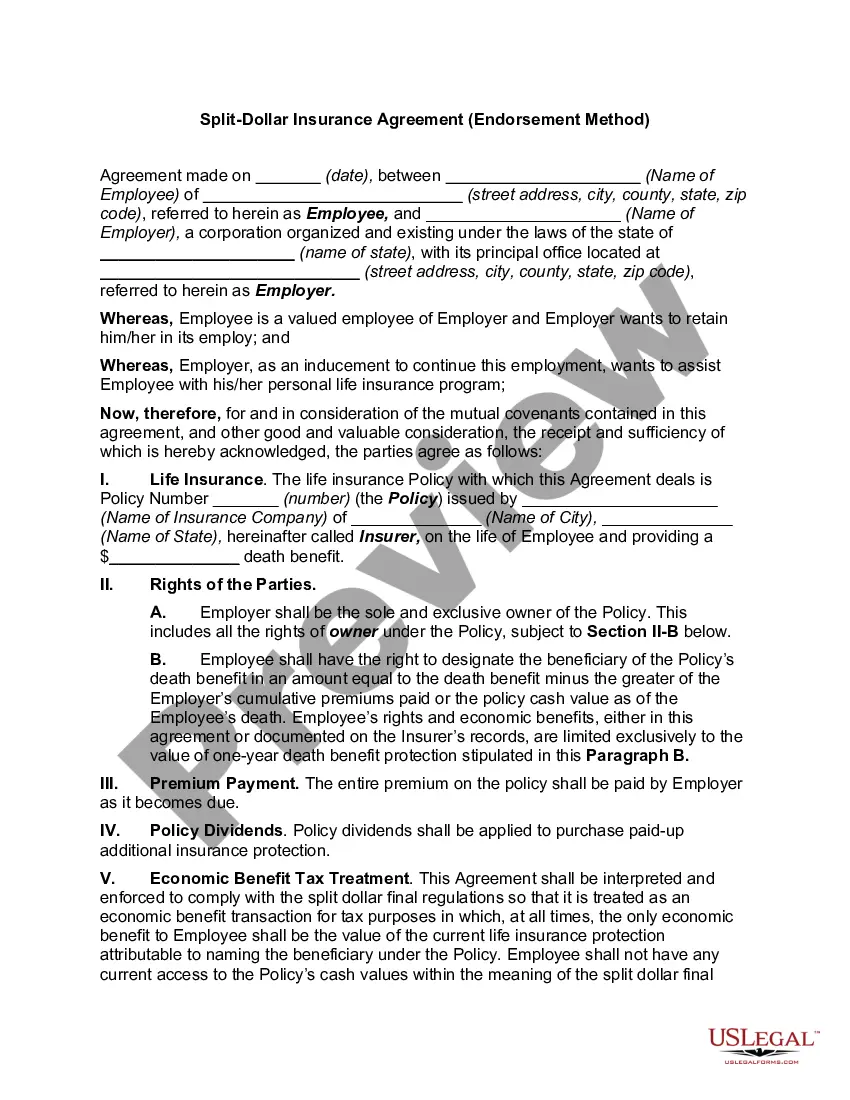

Split-dollar life insurance is an agreement?rather than a policy?between an individual and employer (or trust) using permanent life insurance. The employer pays all or most of the premiums while retaining an interest in the policy's cash value and/or death benefit.

Split Dollar Loan Regime Agreement & Contract Generally, at the employee's death, the employer receives a portion of the death benefit (usually equal to the total premiums plus interest from the loan) and the employee's beneficiary receives the balance.

With a classic split-dollar plan, the employer pays some of the premium (the part that is equal to cash value), while the employee pays the rest. If the employees dies, or the plan is terminated, the surrender cash value is paid to the company, and the death benefits are paid out to beneficiaries.

Split-dollar payment arrangements generally take one of two forms: The employer pays the premiums and owns the contract. The employer receives reimbursement of the premiums upon the employee's death, and the employee's beneficiary then receives the balance of the insurance proceeds.

The best way is to contact the policy's issuer (the life insurance company). Their records are key: even if you see your name listed on an old policy document, the deceased may have changed their beneficiaries (or the allocation of benefits among those beneficiaries) after that document was printed.

Employers are responsible for making split-dollar life insurance premiums, regardless of the plan's type. However, it is important to note that under loan arrangements, employees must repay the premiums via collateral assignments made to their employer.

While split-dollar life insurance arrangements offer numerous advantages, they also come with potential drawbacks, such as complexity, tax considerations, and limited availability. Both employers and employees must carefully weigh the benefits and disadvantages of this type of arrangement before deciding to pursue it.