Idaho A Summary of Your Rights Under the Fair Credit Reporting Act

Description

How to fill out A Summary Of Your Rights Under The Fair Credit Reporting Act?

Are you presently within a place the place you need papers for either company or individual purposes nearly every day time? There are a lot of lawful record layouts available online, but locating types you can rely on is not effortless. US Legal Forms offers thousands of develop layouts, just like the Idaho A Summary of Your Rights Under the Fair Credit Reporting Act, which can be published to satisfy state and federal requirements.

If you are already informed about US Legal Forms internet site and have your account, just log in. Following that, you can down load the Idaho A Summary of Your Rights Under the Fair Credit Reporting Act design.

Should you not come with an account and wish to begin using US Legal Forms, adopt these measures:

- Get the develop you will need and ensure it is for that proper city/state.

- Utilize the Review option to analyze the form.

- Read the description to actually have chosen the proper develop.

- If the develop is not what you are seeking, take advantage of the Look for discipline to discover the develop that suits you and requirements.

- Once you find the proper develop, simply click Buy now.

- Choose the pricing prepare you would like, fill in the required information to produce your money, and purchase an order making use of your PayPal or bank card.

- Pick a practical file formatting and down load your duplicate.

Get each of the record layouts you possess bought in the My Forms menu. You can obtain a additional duplicate of Idaho A Summary of Your Rights Under the Fair Credit Reporting Act anytime, if necessary. Just click the necessary develop to down load or printing the record design.

Use US Legal Forms, the most substantial collection of lawful types, to save lots of efforts and steer clear of errors. The assistance offers skillfully made lawful record layouts that you can use for a selection of purposes. Produce your account on US Legal Forms and initiate creating your daily life a little easier.

Form popularity

FAQ

If you have an otherwise blemish-free credit history, go ahead and ask the collection agency for a goodwill deletion. Removal after payment might be against their rules?but goodwill deletions might not be, and it never hurts to ask. You can find goodwill letter templates online to help you communicate with your lender.

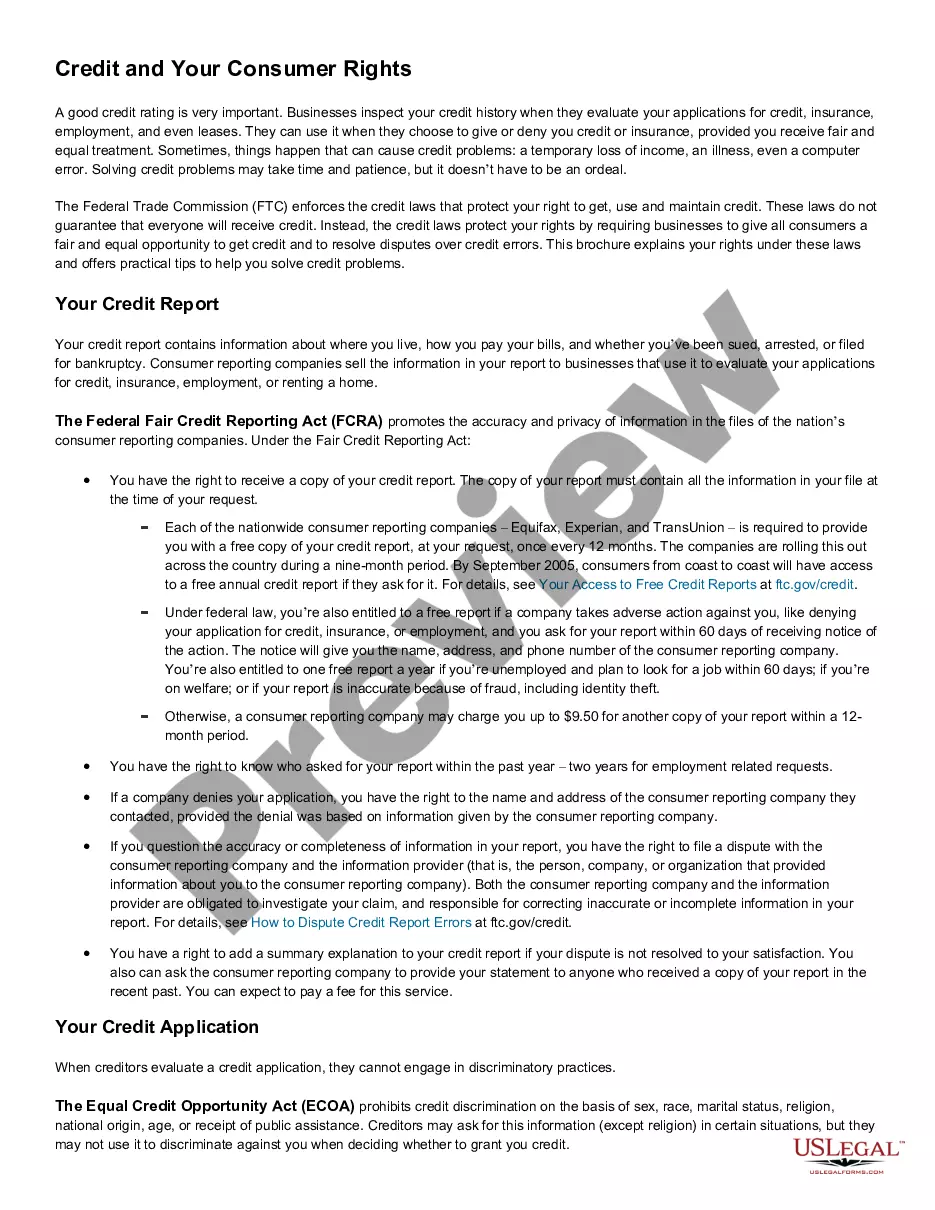

The Summary of Consumer Rights explains certain major consumer rights under the FCRA, including the right to obtain a copy of a consumer report, the frequency and circumstances under which a consumer is entitled to receive a free consumer report, the right to dispute information in a consumer's file, and the right to ...

The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.

In August 2022, it was announced that medical debt in collections would no longer be used in calculating Vantage scores, one of the country's most used credit scoring models. In addition, after April 2023, medical collections under $500 would no longer appear on consumer credit reports.

How can you remove collections from a credit report? Step 1: Ask for proof. Step 2: Look for and report inaccuracies. Step 3: Ask for a pay-for-delete agreement. Step 4: Write a goodwill letter to your creditor.

Federal Legislative Activity in 2023 Amend Section 604(c) of the FCRA to address the treatment of pre-screening report requests. Section 604(c) governs the furnishing of reports in connection with credit or insurance transactions that are not initiated by the consumer.

The myth comes from the fact that most negative information will leave your credit report within seven years of an incident. In reality, a missed payment on your debt will only take six years to disappear from your credit report, but this has no effect on whether you still need to pay.

The Bureau is amending Appendix O to Regulation V, which implements the FCRA, to establish the maximum allowable charge for disclosures by a consumer reporting agency to a consumer for 2023. The maximum allowable charge will be $14.50 for 2023.

Reporting of Medical Debt: The three major credit bureaus (Equifax, Transunion, and Experian) will institute a new policy by March 30, 2023, to no longer include medical debt under a dollar threshold (the threshold will be at least $500) on credit reports.