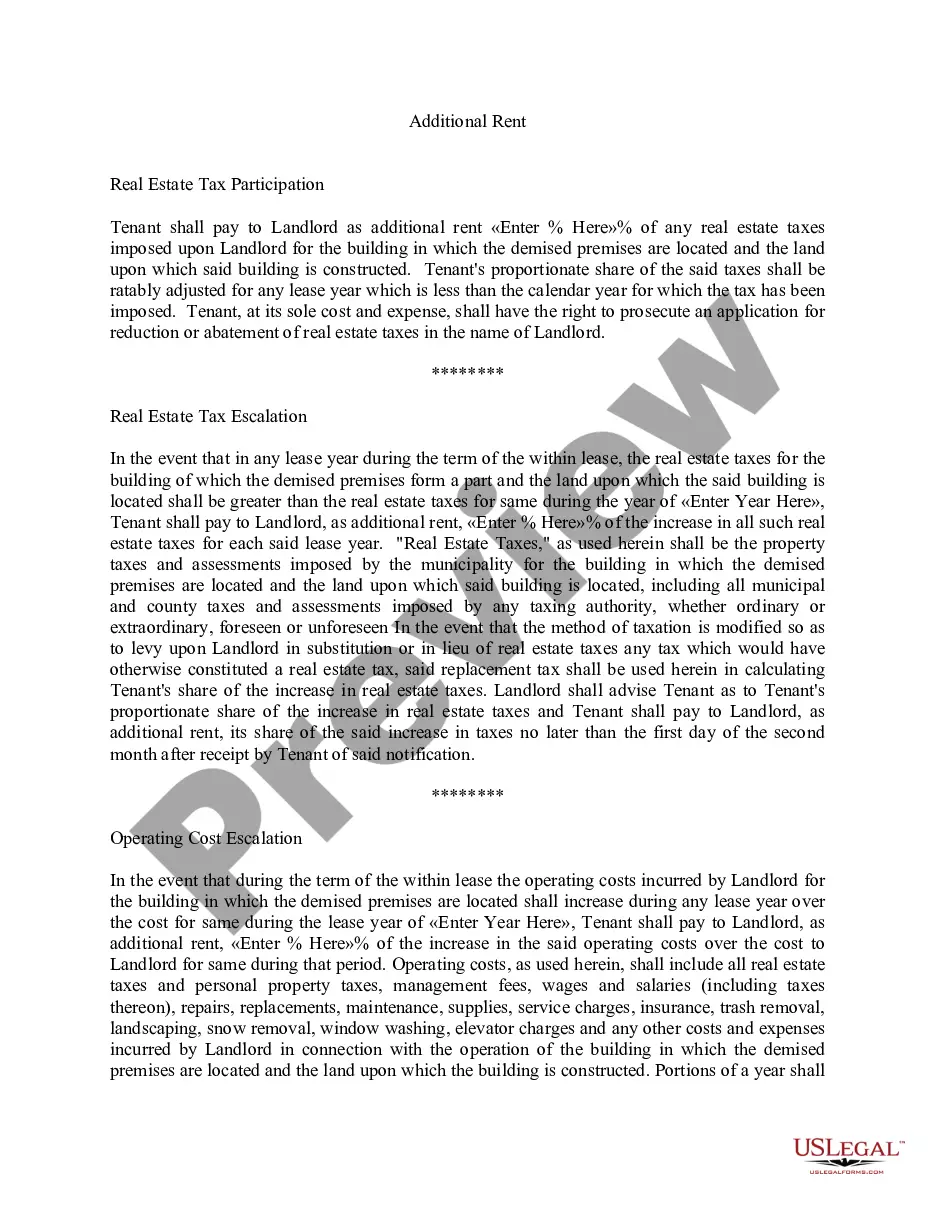

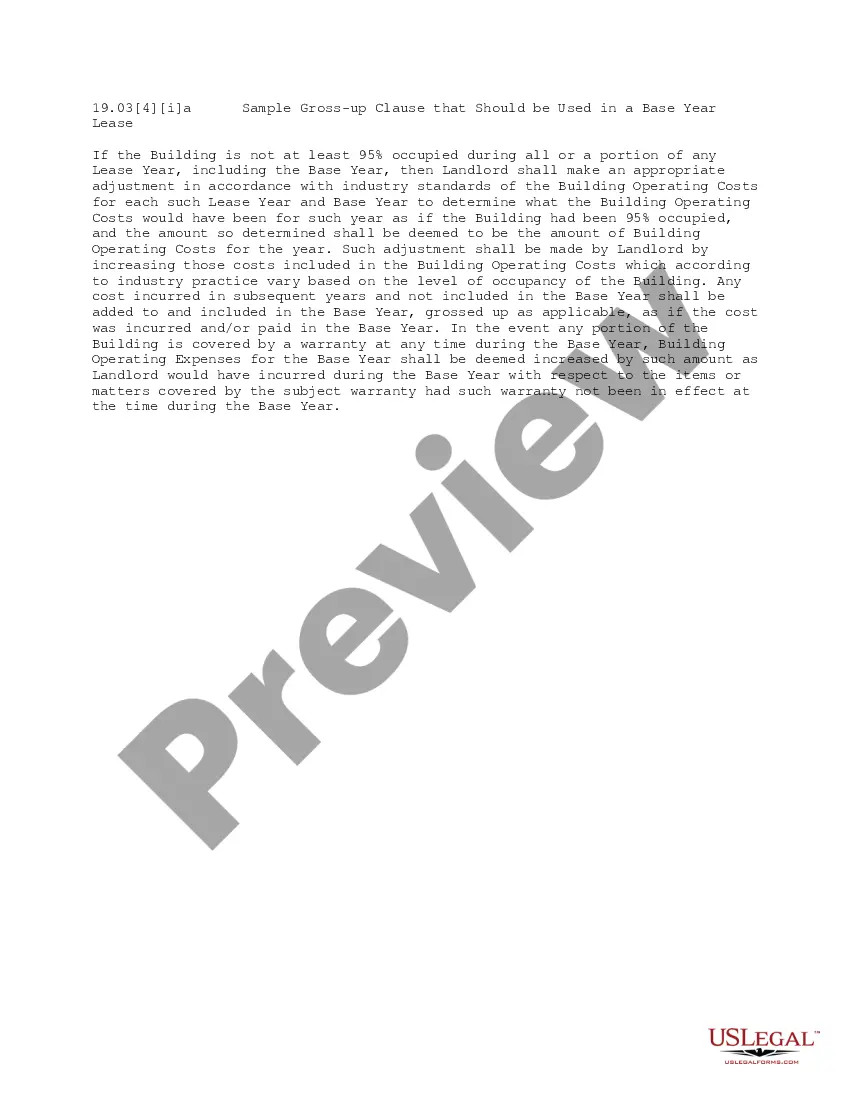

This form is a clause regarding additional rent element of an office lease providing for tax increases. The tax increases pertain to assessments and special assessments levied, assessed or imposed upon the building and/or the land under, including any land(s) dedicated to the use of, the building, by any governmental bodies or authorities.

Idaho Tax Increase Clause

Category:

State:

Multi-State

Control #:

US-OL19033GA

Format:

Word;

PDF

Instant download

Description

Free preview

How to fill out Tax Increase Clause?

If you have to total, acquire, or printing authorized record themes, use US Legal Forms, the biggest selection of authorized kinds, which can be found on-line. Utilize the site`s basic and convenient lookup to find the papers you require. A variety of themes for company and person functions are categorized by categories and states, or search phrases. Use US Legal Forms to find the Idaho Tax Increase Clause in just a couple of click throughs.

If you are currently a US Legal Forms buyer, log in to your accounts and then click the Download key to obtain the Idaho Tax Increase Clause. You can also access kinds you in the past delivered electronically inside the My Forms tab of your own accounts.

If you are using US Legal Forms the first time, follow the instructions under:

- Step 1. Be sure you have chosen the shape for your correct city/land.

- Step 2. Utilize the Preview solution to look over the form`s content material. Do not forget about to learn the description.

- Step 3. If you are unsatisfied using the kind, utilize the Search industry on top of the screen to locate other types from the authorized kind design.

- Step 4. When you have found the shape you require, click on the Get now key. Opt for the pricing plan you choose and add your accreditations to sign up on an accounts.

- Step 5. Process the purchase. You may use your Мisa or Ьastercard or PayPal accounts to complete the purchase.

- Step 6. Pick the structure from the authorized kind and acquire it on the product.

- Step 7. Full, revise and printing or indication the Idaho Tax Increase Clause.

Each and every authorized record design you buy is the one you have forever. You may have acces to every single kind you delivered electronically in your acccount. Click on the My Forms segment and select a kind to printing or acquire again.

Contend and acquire, and printing the Idaho Tax Increase Clause with US Legal Forms. There are millions of specialist and express-certain kinds you may use to your company or person requirements.

Form popularity

FAQ

The tax rate is 1% of the total home value and the rate can only increase a max of 2% per year.

The exemption is capped at $125,000. For example, if you own and live in a home with a market value of $150,000, your assessed value is $150,000. Your homeowners exemption would be $75,000 (half the value of the home), which means your tax rate will be applied to a total value of $75,000.

Idaho's first sales tax went into effect in 1965. The tax started at three percent and climbed to six percent by 2006, which is the current rate. The Idaho Tax Commission says retail sales and rentals of tangible personal property, admission fees and fees for recreation or hotel rooms are all subject to the sales tax.

Taxes are determined ing to a property's current market value minus any exemptions. For example, homeowners of owner-occupied property may qualify for a partial exemption. Also, qualified low income homeowners can receive a property tax reduction.

You may qualify for a property tax reduction if you meet the following requirements. You are in one or more of the following categories as of January 1st: Age 65 or older. Widow(er) of any age.

Changes to Idaho's tax rate Idaho's tax rate is now 5.8% for all taxpayers. For individuals, the rate applies to taxable income over: $4,489 if you're filing single. $8,978 if you're filing jointly.

Idaho property tax. Idaho limits how much local governments can increase property tax budgets to 3%. This may help keep property tax bills from skyrocketing too quickly, but the 3% limit can be overridden.