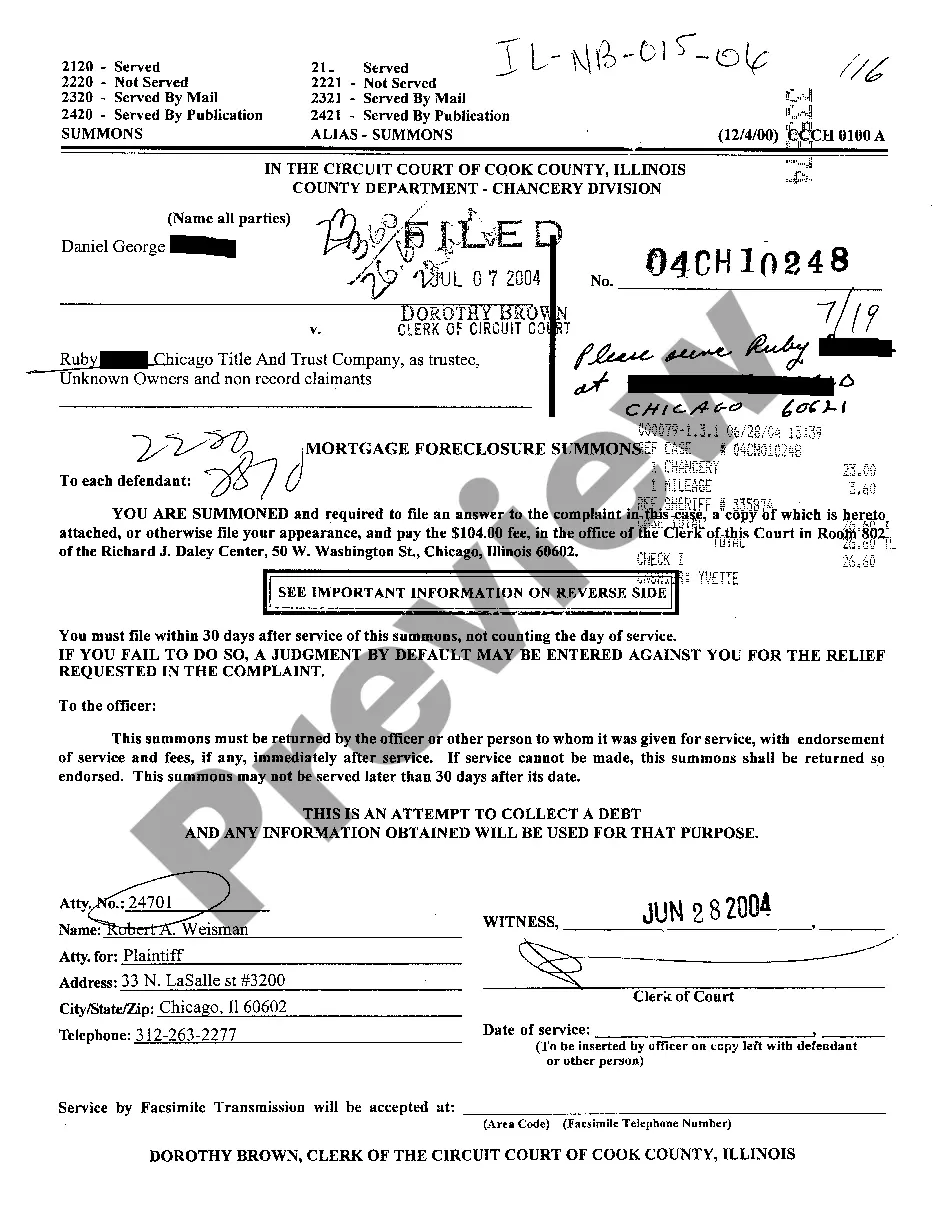

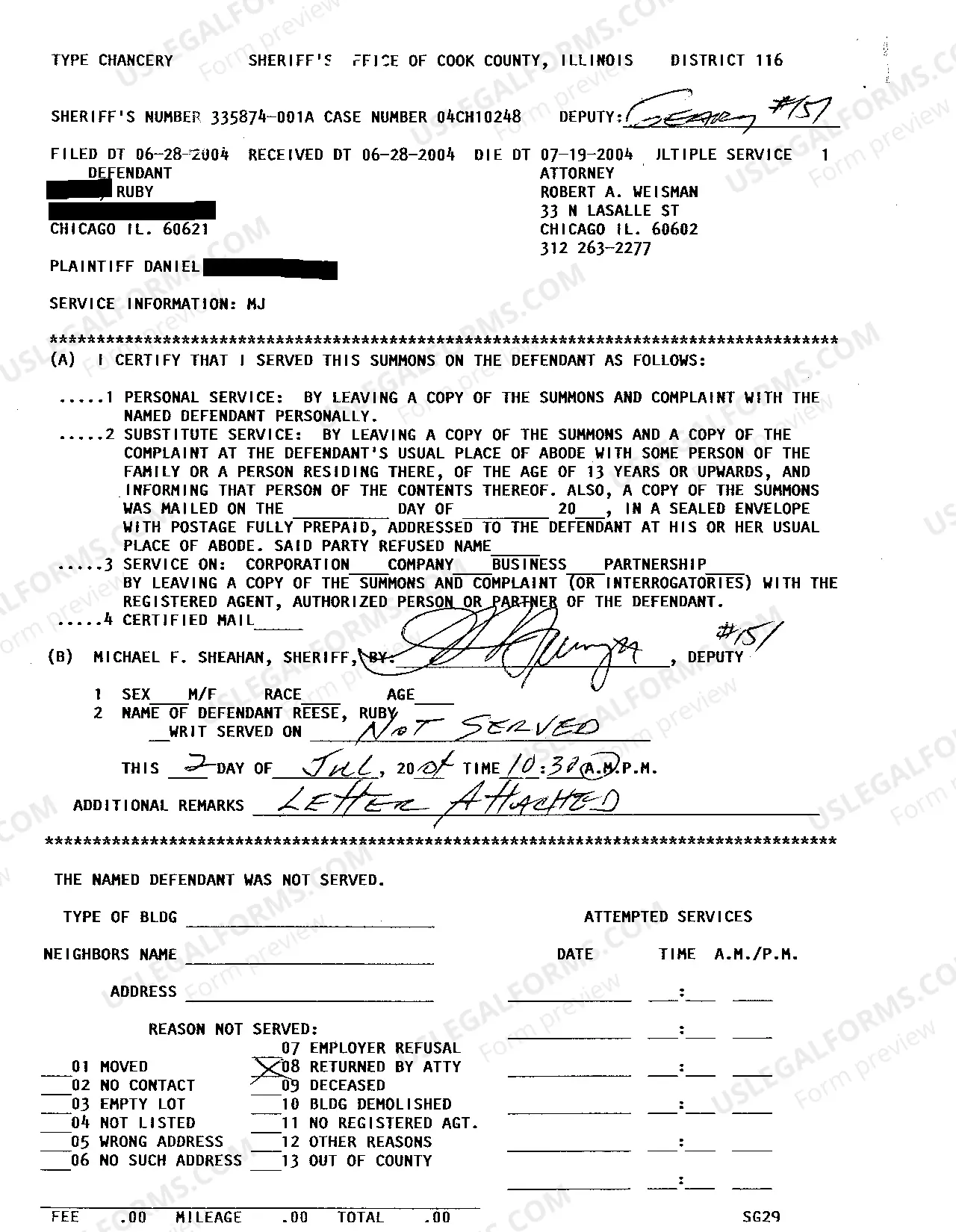

Illinois Mortgage Foreclosure Summons

Description

How to fill out Illinois Mortgage Foreclosure Summons?

Looking for Illinois Mortgage Foreclosure Summons sample and filling out them could be a problem. To save lots of time, costs and effort, use US Legal Forms and find the correct example specially for your state in just a couple of clicks. Our attorneys draw up every document, so you just have to fill them out. It truly is that easy.

Log in to your account and come back to the form's web page and save the document. Your downloaded templates are stored in My Forms and they are accessible always for further use later. If you haven’t subscribed yet, you have to sign up.

Have a look at our detailed recommendations on how to get the Illinois Mortgage Foreclosure Summons sample in a couple of minutes:

- To get an eligible sample, check out its applicability for your state.

- Take a look at the form using the Preview option (if it’s available).

- If there's a description, go through it to know the important points.

- Click on Buy Now button if you identified what you're seeking.

- Pick your plan on the pricing page and create your account.

- Choose you wish to pay out by way of a credit card or by PayPal.

- Download the sample in the preferred format.

Now you can print the Illinois Mortgage Foreclosure Summons form or fill it out using any online editor. No need to worry about making typos because your sample can be used and sent, and published as many times as you wish. Try out US Legal Forms and access to more than 85,000 state-specific legal and tax files.

Form popularity

FAQ

In Illinois, it can take approximately 12-15 months for a foreclosure to be completed. Call your lender or a HUD-certified counseling agency as soon as you can.

Generally, homeowners have to be more than 120 days delinquent before a foreclosure can begin. If you're behind in mortgage payments, you might be wondering how soon a foreclosure will start. Generally, a homeowner has to be at least 120 days delinquent before a mortgage servicer starts a foreclosure.

When You Have to Leave After an Illinois Foreclosure Sale The foreclosed homeowner can remain in the home for 30 days after the court confirms the sale.

In Illinois, it can take approximately 12-15 months for a foreclosure to be completed. Call your lender or a HUD-certified counseling agency as soon as you can.

In most states, lenders are required to provide a homeowner with sufficient notice of default. The lender must also provide notice of the property owner's right to cure the default before the lender can initiate a foreclosure proceeding. Written proof of money owed under the mortgage.

Foreclosure proceedings begin with a complaint filed by the lender. The borrower is served a copy of the complaint and a summons, along with a notice of his or her rights during foreclosure. In most cases, the borrower has 30 days to file a response. Failure to respond will result in a default judgment for the lender.

If the court grants summary judgment in favor of the bank, typically after a hearing, the bank wins the case, and your home will be sold at a foreclosure sale.order the foreclosure sale, or. dismiss the case, usually without prejudice. (Without prejudice means the bank can refile the foreclosure.)

The Notice of Default starts the official foreclosure process. This notice is issued 30 days after the fourth missed monthly payment. From this point onwards, the borrower will have 2 to 3 months, depending on state law, to reinstate the loan and stop the foreclosure process.