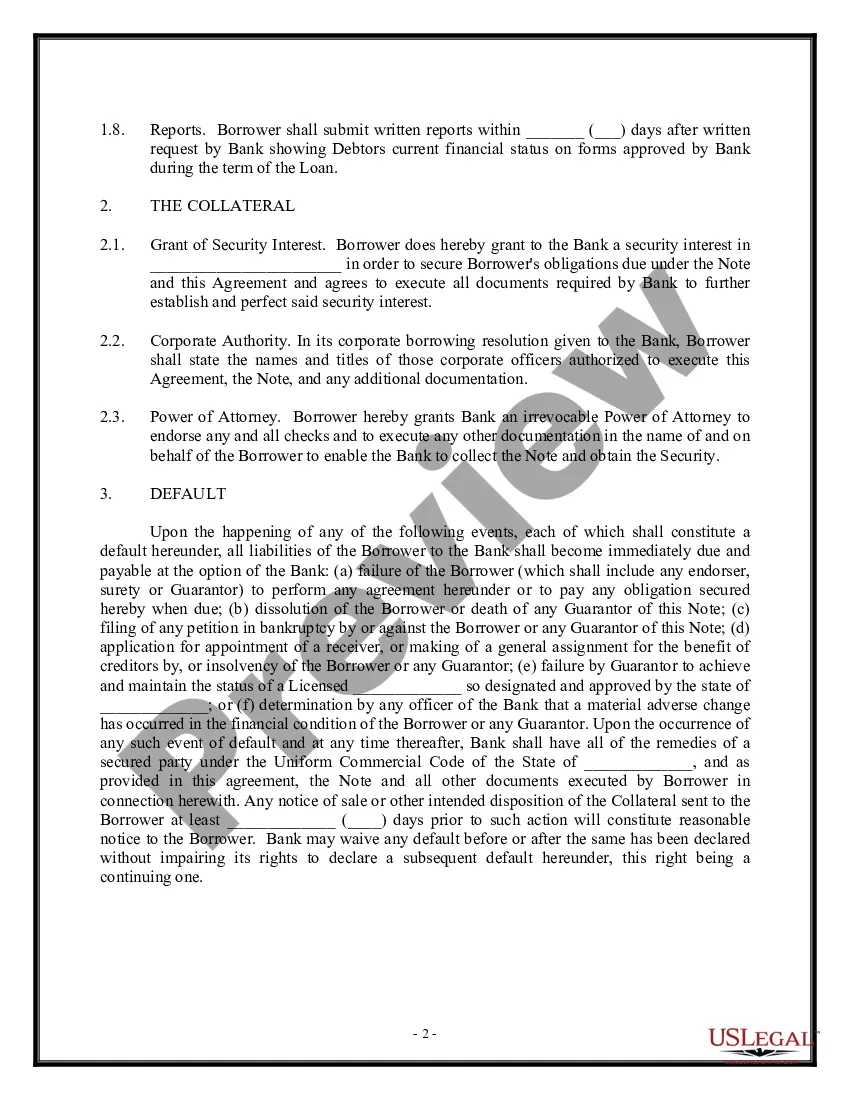

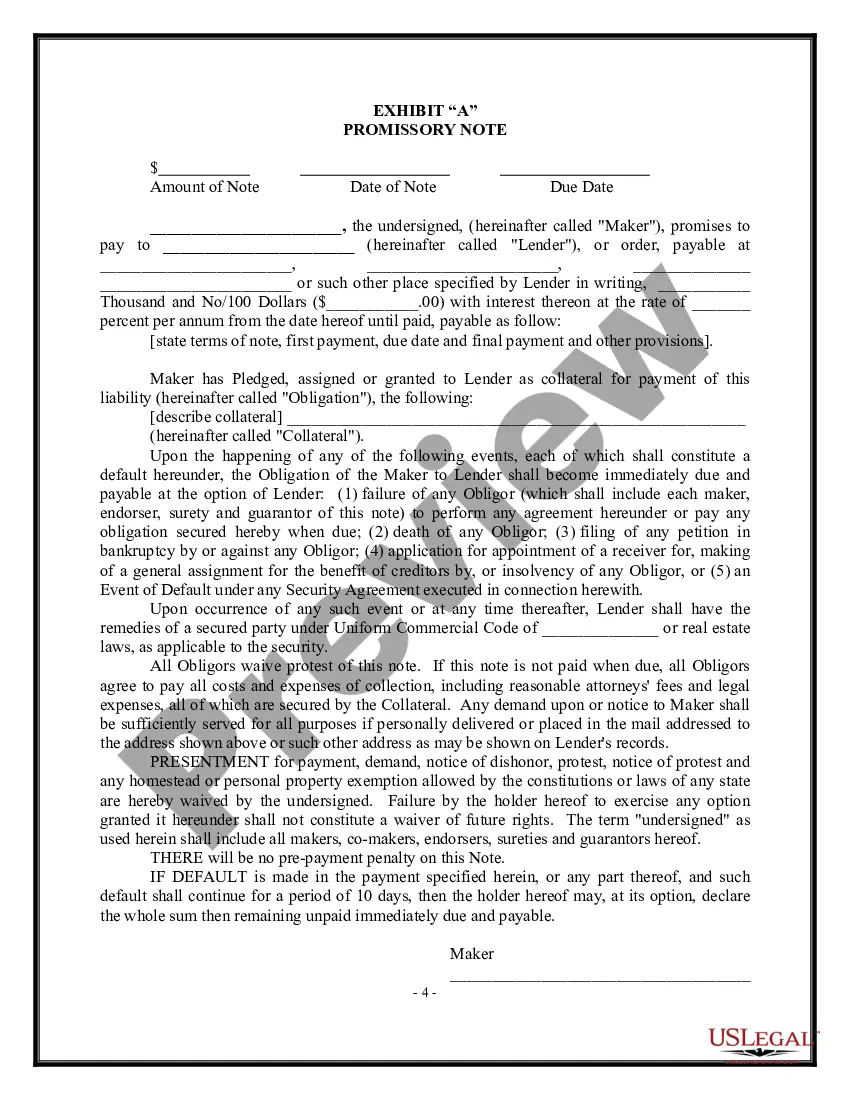

The Illinois Loan Agreement — Short Form is a legally binding document that outlines the terms and conditions for a loan transaction between a lender and borrower in the state of Illinois. This agreement is designed to provide a concise and straightforward framework for individuals or businesses engaging in small-scale lending activities, ensuring that both parties are protected and aware of their rights and obligations. The Illinois Loan Agreement — Short Form typically covers essential aspects of the loan, such as the loan amount, interest rate, repayment terms, and any additional fees or charges. The agreement also includes provisions related to default, late payments, and the remedies available to both the lender and borrower in case of non-compliance. In Illinois, there are several types of Loan Agreement — Short Form that cater to specific lending situations or industries. Some common variations include: 1. Personal Loan Agreement: This type of agreement is used when an individual lends money to another individual, typically for personal reasons such as debt consolidation, home repairs, or education expenses. 2. Business Loan Agreement: This agreement is tailored for lending transactions between businesses, such as a small business owner borrowing funds to finance their operations, purchase inventory, or expand their enterprise. 3. Payday Loan Agreement: Payday loans are short-term, high-interest loans that are typically repaid within a few weeks. This type of agreement is often used by individuals in urgent need of cash between paychecks, with the borrower agreeing to repay the loan with their next paycheck. 4. Promissory Note Agreement: While not strictly a loan agreement, a promissory note is a legal instrument used to document a loan's terms and serves as evidence of the borrower's promise to repay the loan. It can be used in conjunction with a loan agreement or as a stand-alone document. It's important to note that these variations of the Illinois Loan Agreement — Short Form may have specific legal requirements or considerations. Consulting with a qualified attorney or legal professional is recommended to ensure compliance with relevant laws and regulations. In conclusion, the Illinois Loan Agreement — Short Form is a versatile document that facilitates loan transactions between lenders and borrowers in the state. Whether it's for personal or business purposes, having a well-drafted loan agreement helps protect the interests of all parties involved, ensuring clear communication, and mitigating potential disputes.

Illinois Loan Agreement - Short Form

Description

How to fill out Illinois Loan Agreement - Short Form?

You may devote hrs on the Internet trying to find the lawful papers design that suits the state and federal needs you need. US Legal Forms offers 1000s of lawful kinds that are examined by specialists. You can easily down load or print the Illinois Loan Agreement - Short Form from your support.

If you currently have a US Legal Forms bank account, you can log in and click on the Download button. Afterward, you can complete, edit, print, or signal the Illinois Loan Agreement - Short Form. Every lawful papers design you purchase is your own for a long time. To obtain yet another copy of any purchased form, go to the My Forms tab and click on the corresponding button.

Should you use the US Legal Forms website the very first time, follow the straightforward recommendations beneath:

- Very first, make sure that you have chosen the right papers design to the county/town of your choice. Read the form outline to make sure you have selected the correct form. If offered, take advantage of the Review button to check throughout the papers design also.

- If you want to locate yet another version of the form, take advantage of the Lookup field to get the design that meets your requirements and needs.

- Upon having discovered the design you would like, click Buy now to move forward.

- Find the costs plan you would like, type your credentials, and register for a free account on US Legal Forms.

- Comprehensive the purchase. You can utilize your bank card or PayPal bank account to cover the lawful form.

- Find the structure of the papers and down load it to your gadget.

- Make alterations to your papers if possible. You may complete, edit and signal and print Illinois Loan Agreement - Short Form.

Download and print 1000s of papers themes utilizing the US Legal Forms site, which offers the greatest variety of lawful kinds. Use expert and status-particular themes to tackle your business or person requirements.