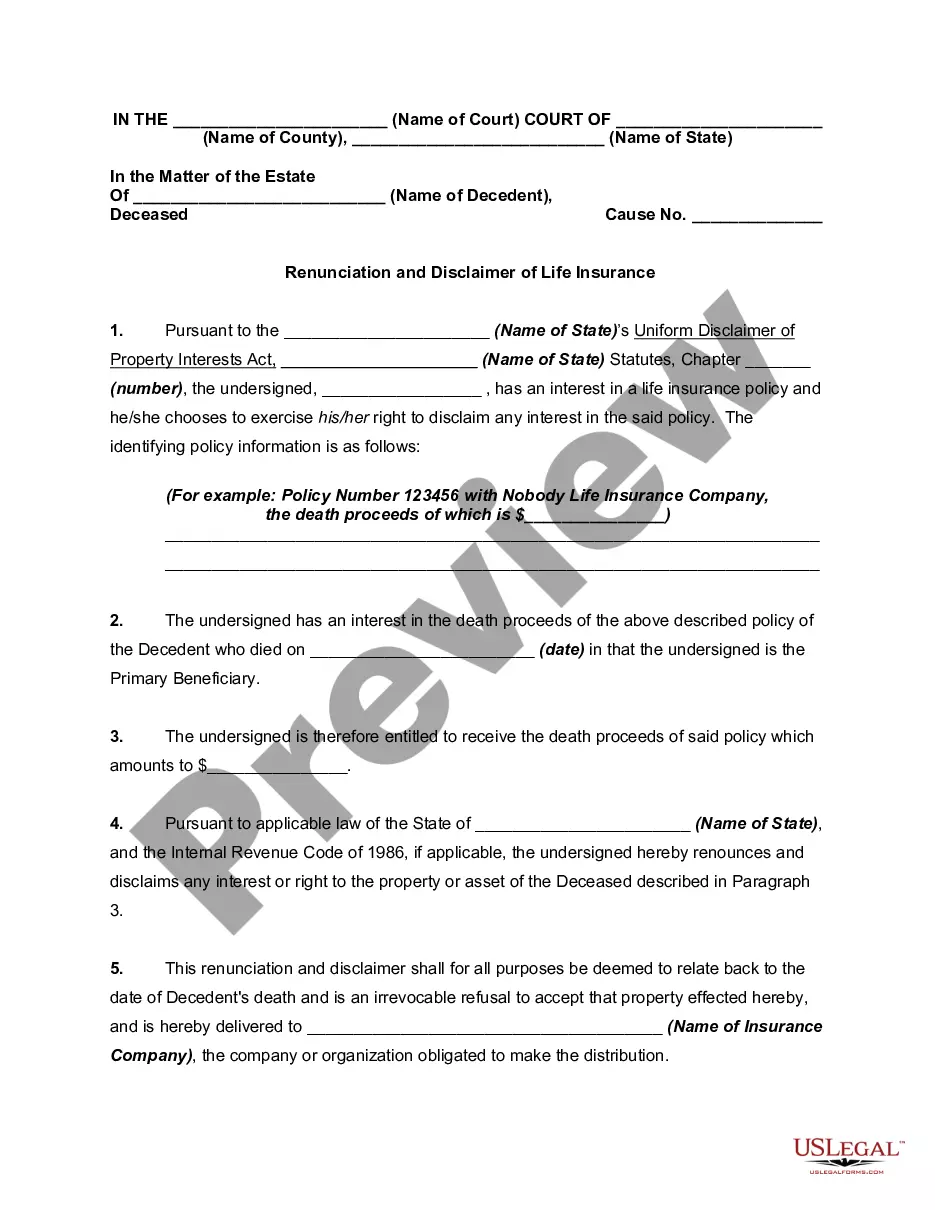

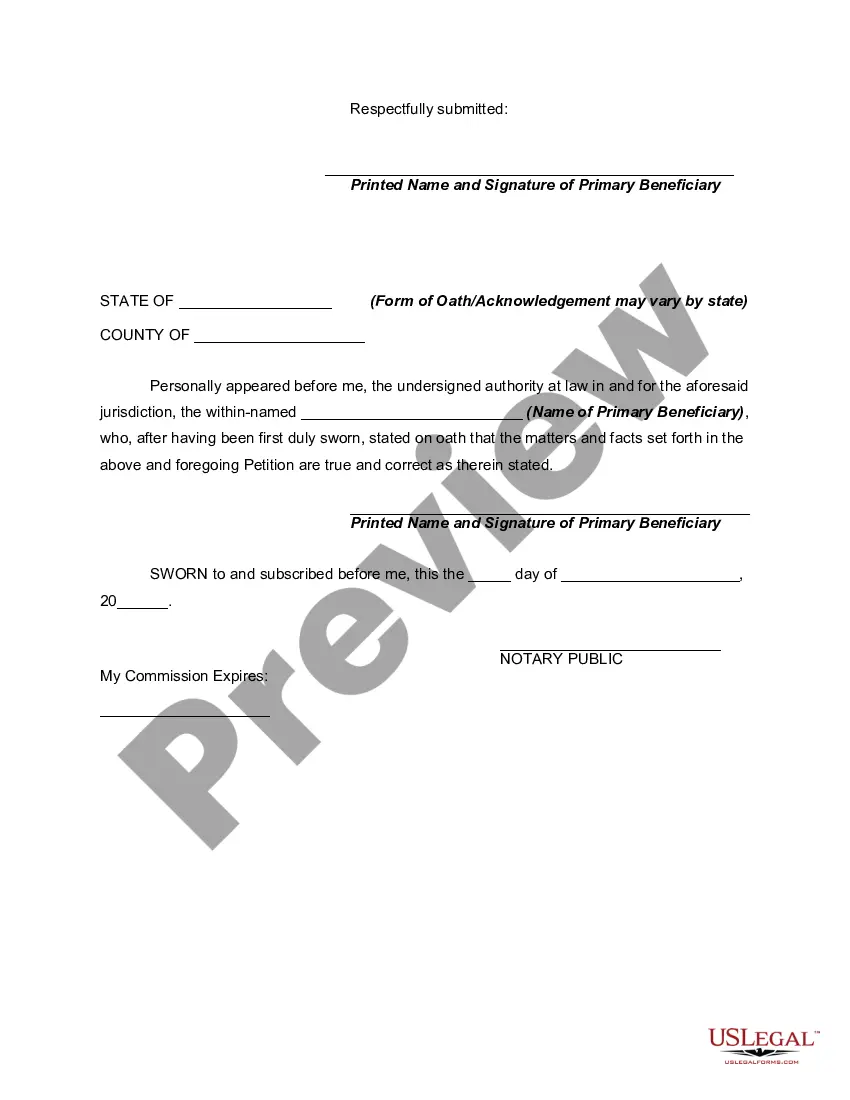

Disclaimers are used by those who receive property as heirs or legatees in an estate, or by beneficiaries of a non-testamentary transfer of property at death; for example, the beneficiaries of a life insurance policy. A disclaimer is simply a declaration by the person entitled to property that the interest in that property is disclaimed or renounced. A disclaimer allows the disclaiming heir or beneficiary to disclaim an interest in such a fashion that the right to the property that is disclaimed is treated as if it never existed.

The Uniform Disclaimers of Property Interests Act (which has been adopted by a number of states) provides the authority to make disclaimers, what interests may be disclaimed, the time when disclaimers are effective, and the effect on the distribution of the disclaimed property interests.

Illinois Renunciation and Disclaimer of Interest in Life Insurance Proceeds: A Detailed Explanation In the realm of life insurance, individuals occasionally find themselves in a situation where they may need to renounce or disclaim their interest in life insurance proceeds. Illinois recognizes this necessity, providing legal provisions for beneficiaries to relinquish their rights to these financial benefits, ensuring smooth administration and distribution of the policy proceeds. In this article, we delve into the details of Illinois Renunciation and Disclaimer of Interest in Life Insurance Proceeds, highlighting its purpose, significance, and various types. Purpose and Significance: The Illinois Renunciation and Disclaimer of Interest in Life Insurance Proceeds enable beneficiaries to legally refuse their claim to the insurance benefits associated with a life insurance policy. While it may seem counterintuitive to decline such a financial advantage, there are situations where renunciation or disclaimer becomes necessary. These actions may be required to accommodate complex estate planning, minimize tax implications, address creditor concerns, or facilitate the equitable distribution of assets. By offering beneficiaries the option to renounce their entitlement, Illinois ensures flexibility and transparency in the transfer of life insurance proceeds. Types of Renunciation and Disclaimer in Illinois: 1. Absolute Renunciation: Under Illinois law, beneficiaries can exercise an absolute renunciation of their interest in life insurance proceeds. By renouncing their claim, beneficiaries entirely surrender any rights they possess to the policy's benefits. This allows for an uninterrupted succession of the insurance proceeds to other designated beneficiaries or successors. 2. Conditional Renunciation: In certain cases, beneficiaries may choose to conditionally renounce their interest in life insurance proceeds. Such renunciations are typically subject to certain conditions, which may include specific events, timeframes, or additional requirements. Conditional renunciations provide beneficiaries with flexibility while addressing unique circumstances or concerns that may arise. 3. Partial Renunciation: In situations where beneficiaries do not wish to relinquish their entire interest in the life insurance proceeds, they have the option to pursue a partial renunciation. This allows beneficiaries to renounce only a specific portion or percentage of their share. This flexibility ensures that they can still benefit partially, while potentially addressing estate tax issues, creditor claims, or other concerns. 4. Disclaimer of Interest: In addition to renunciation, Illinois recognizes the concept of disclaimer regarding life insurance proceeds. Beneficiaries can disclaim their interest in the policy benefits, effectively refusing their inheritance. Similar to renunciation, disclaimers facilitate the smooth transfer of insurance proceeds to alternative beneficiaries or successors. Conclusion: Illinois Renunciation and Disclaimer of Interest in Life Insurance Proceeds play a crucial role in estate planning, allowing beneficiaries to relinquish their rights to life insurance benefits. Whether through an absolute renunciation, conditional renunciation, partial renunciation, or disclaimer of interest, individuals can navigate complex situations more effectively. By utilizing these legal options, beneficiaries can ensure a streamlined transition of life insurance proceeds, address tax concerns, protect assets, and uphold the intentions of the insured.Illinois Renunciation and Disclaimer of Interest in Life Insurance Proceeds: A Detailed Explanation In the realm of life insurance, individuals occasionally find themselves in a situation where they may need to renounce or disclaim their interest in life insurance proceeds. Illinois recognizes this necessity, providing legal provisions for beneficiaries to relinquish their rights to these financial benefits, ensuring smooth administration and distribution of the policy proceeds. In this article, we delve into the details of Illinois Renunciation and Disclaimer of Interest in Life Insurance Proceeds, highlighting its purpose, significance, and various types. Purpose and Significance: The Illinois Renunciation and Disclaimer of Interest in Life Insurance Proceeds enable beneficiaries to legally refuse their claim to the insurance benefits associated with a life insurance policy. While it may seem counterintuitive to decline such a financial advantage, there are situations where renunciation or disclaimer becomes necessary. These actions may be required to accommodate complex estate planning, minimize tax implications, address creditor concerns, or facilitate the equitable distribution of assets. By offering beneficiaries the option to renounce their entitlement, Illinois ensures flexibility and transparency in the transfer of life insurance proceeds. Types of Renunciation and Disclaimer in Illinois: 1. Absolute Renunciation: Under Illinois law, beneficiaries can exercise an absolute renunciation of their interest in life insurance proceeds. By renouncing their claim, beneficiaries entirely surrender any rights they possess to the policy's benefits. This allows for an uninterrupted succession of the insurance proceeds to other designated beneficiaries or successors. 2. Conditional Renunciation: In certain cases, beneficiaries may choose to conditionally renounce their interest in life insurance proceeds. Such renunciations are typically subject to certain conditions, which may include specific events, timeframes, or additional requirements. Conditional renunciations provide beneficiaries with flexibility while addressing unique circumstances or concerns that may arise. 3. Partial Renunciation: In situations where beneficiaries do not wish to relinquish their entire interest in the life insurance proceeds, they have the option to pursue a partial renunciation. This allows beneficiaries to renounce only a specific portion or percentage of their share. This flexibility ensures that they can still benefit partially, while potentially addressing estate tax issues, creditor claims, or other concerns. 4. Disclaimer of Interest: In addition to renunciation, Illinois recognizes the concept of disclaimer regarding life insurance proceeds. Beneficiaries can disclaim their interest in the policy benefits, effectively refusing their inheritance. Similar to renunciation, disclaimers facilitate the smooth transfer of insurance proceeds to alternative beneficiaries or successors. Conclusion: Illinois Renunciation and Disclaimer of Interest in Life Insurance Proceeds play a crucial role in estate planning, allowing beneficiaries to relinquish their rights to life insurance benefits. Whether through an absolute renunciation, conditional renunciation, partial renunciation, or disclaimer of interest, individuals can navigate complex situations more effectively. By utilizing these legal options, beneficiaries can ensure a streamlined transition of life insurance proceeds, address tax concerns, protect assets, and uphold the intentions of the insured.