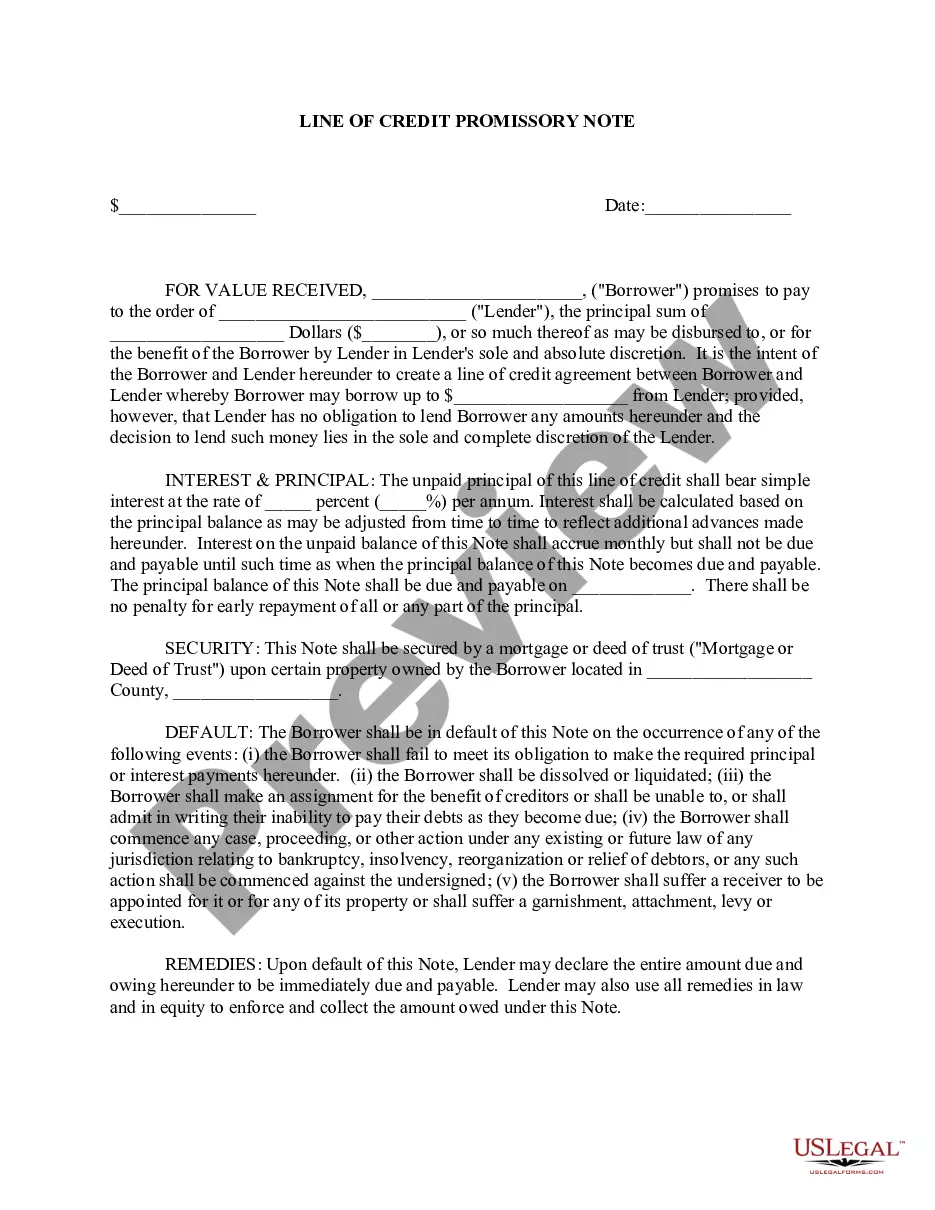

An Illinois Line of Credit Promissory Note is a legally binding document that outlines the terms and conditions regarding a line of credit taken by a borrower in the state of Illinois. This promissory note serves as a written agreement between the borrower and the lender, clearly defining the rights and obligations of both parties. A line of credit is a flexible arrangement where the borrower can access funds up to a predetermined limit, and interest is only charged on the amount borrowed. This type of financing is often used by individuals or businesses to manage their cash flow, cover unexpected expenses, or take advantage of investment opportunities. The Illinois Line of Credit Promissory Note contains various essential elements, such as: 1. Parties Involved: The names and contact information of both the borrower and the lender are stated at the beginning of the note. 2. Loan Details: The principal amount of the line of credit, the interest rate charged, and any additional fees or charges are clearly specified. 3. Repayment Terms: The repayment terms include the time frame within which the borrower can draw funds from the line of credit, the minimum and maximum borrowing limits, and the repayment schedule. This may involve regular installments or interest-only payments, depending on the agreement. 4. Interest and Fees: The interest rate and any applicable fees, such as an annual fee or transaction fees, are explicitly mentioned. 5. Default and Remedies: This section outlines the consequences if the borrower fails to repay the line of credit as agreed. It may include penalties, increased interest rates, or the lender's right to demand immediate repayment. 6. Governing Law: As the note is specific to Illinois, it references the applicable laws of the state regarding the validity, interpretation, and enforcement of the terms. Different types of Illinois Line of Credit Promissory Notes can vary based on factors such as the purpose of the line of credit, whether it is for personal or commercial use, and the specific terms negotiated between the borrower and lender. Some common variations may include: 1. Personal Line of Credit Promissory Note: Used by individuals for personal expenses or emergencies. 2. Business Line of Credit Promissory Note: Designed for businesses to cover operating costs, inventory purchases, or cash flow management. 3. Secured Line of Credit Promissory Note: Involves securing the line of credit with collateral, which provides added security for the lender. 4. Unsecured Line of Credit Promissory Note: Does not require any collateral, but often involves higher interest rates to compensate for the increased risk. In summary, an Illinois Line of Credit Promissory Note is a crucial legal document that safeguards the rights and obligations of both the borrower and lender in a line of credit agreement. Understanding the specifics of this document helps ensure a transparent and mutually beneficial financial relationship.

Illinois Line of Credit Promissory Note

Description

How to fill out Illinois Line Of Credit Promissory Note?

Are you presently in the place in which you require documents for possibly enterprise or person uses almost every day time? There are plenty of authorized record web templates available online, but getting ones you can rely on is not effortless. US Legal Forms gives a large number of kind web templates, like the Illinois Line of Credit Promissory Note, which are published in order to meet state and federal specifications.

If you are already knowledgeable about US Legal Forms website and also have your account, merely log in. Following that, it is possible to obtain the Illinois Line of Credit Promissory Note template.

If you do not offer an profile and would like to begin to use US Legal Forms, abide by these steps:

- Obtain the kind you want and make sure it is to the proper metropolis/county.

- Take advantage of the Preview switch to check the form.

- Browse the explanation to actually have selected the proper kind.

- If the kind is not what you are seeking, use the Search field to get the kind that suits you and specifications.

- When you discover the proper kind, simply click Purchase now.

- Pick the prices prepare you would like, submit the specified information to create your account, and purchase the transaction making use of your PayPal or Visa or Mastercard.

- Select a practical data file file format and obtain your duplicate.

Locate all of the record web templates you have bought in the My Forms menus. You can get a additional duplicate of Illinois Line of Credit Promissory Note anytime, if possible. Just click the necessary kind to obtain or print out the record template.

Use US Legal Forms, probably the most comprehensive assortment of authorized types, to conserve time and steer clear of blunders. The support gives appropriately made authorized record web templates that you can use for a variety of uses. Create your account on US Legal Forms and start generating your way of life easier.