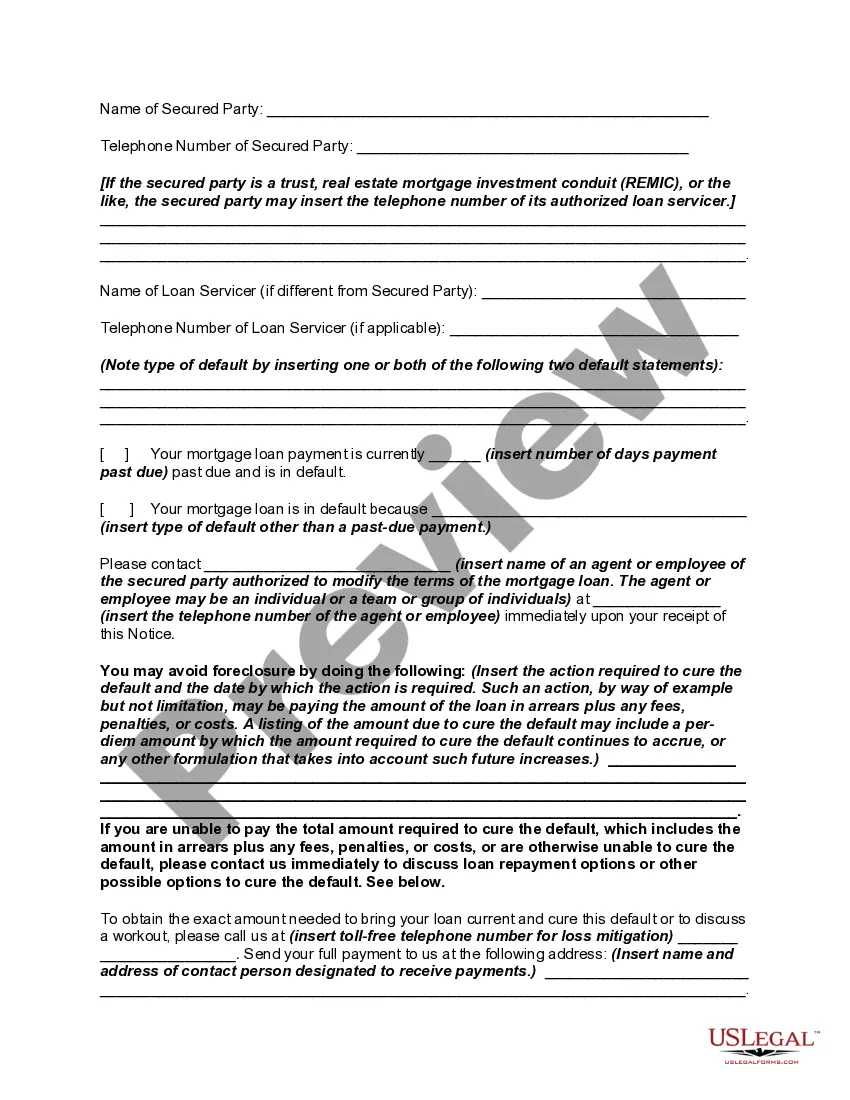

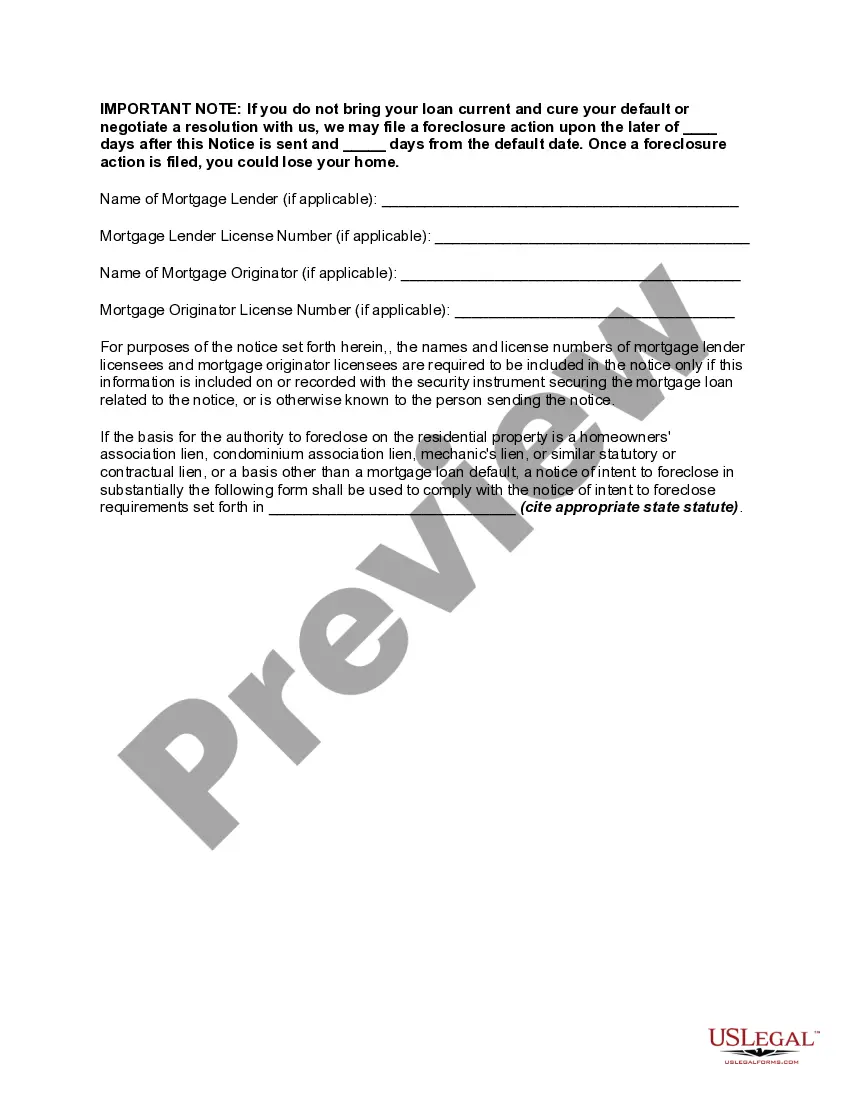

A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

The Illinois Notice of Intent to Foreclose — Mortgage Loan Default is a legal document that serves as a warning to borrowers in Illinois who have defaulted on their mortgage loans. This notice informs the borrower that the lender intends to initiate foreclosure proceedings if the outstanding payment issues are not resolved. The purpose of this notice is to provide a formal communication, as required by Illinois law, to the borrower regarding their default and the lender's intention to proceed with foreclosure. It serves as a prompt for the borrower to take immediate action to rectify the default and avoid the potentially severe consequences of foreclosure. Keywords: Illinois, Notice of Intent to Foreclose, Mortgage Loan Default Types of Illinois Notice of Intent to Foreclose — Mortgage Loan Default: 1. Standard Notice of Intent to Foreclose: This is the most common type of notice, sent by the lender to the borrower who has defaulted on their mortgage loan. It outlines the outstanding payment issues, the consequences of continued default, and the timeframe within which the borrower must respond or take corrective action. 2. Cure or Quit Notice: This specific type of notice is sent to the borrower when they have failed to cure their default within the previously specified timeframe. It informs the borrower that they must either bring the loan current or vacate the property within a specified timeframe, typically within 30 days. 3. Right to Cure Notice: This notice is sent to the borrower before the initiation of the foreclosure process, providing them with an opportunity to cure the default by paying all outstanding amounts owed within a specific timeframe. This notice is required by Illinois law to offer borrowers a chance to avoid foreclosure. 4. Acceleration Notice: In cases where the borrower has defaulted on their mortgage payments for an extended period, the lender may initiate an acceleration notice. This document notifies the borrower that the full loan amount, including all outstanding payments and interest, has become due immediately. If the borrower fails to comply, foreclosure proceedings will be initiated. 5. Judicial Sale Notice: This type of notice informs the borrower that the lender has received a judgment of foreclosure and that the property will be sold at a public auction to recover the outstanding debt. It includes details about the foreclosure sale, including the date, time, and location. It is important to note that the specific content and terminology used within each type of Notice of Intent to Foreclose may vary, as it should comply with Illinois state foreclosure laws and regulations. Borrowers should carefully review these notices and seek legal advice if necessary to fully understand their rights and responsibilities.