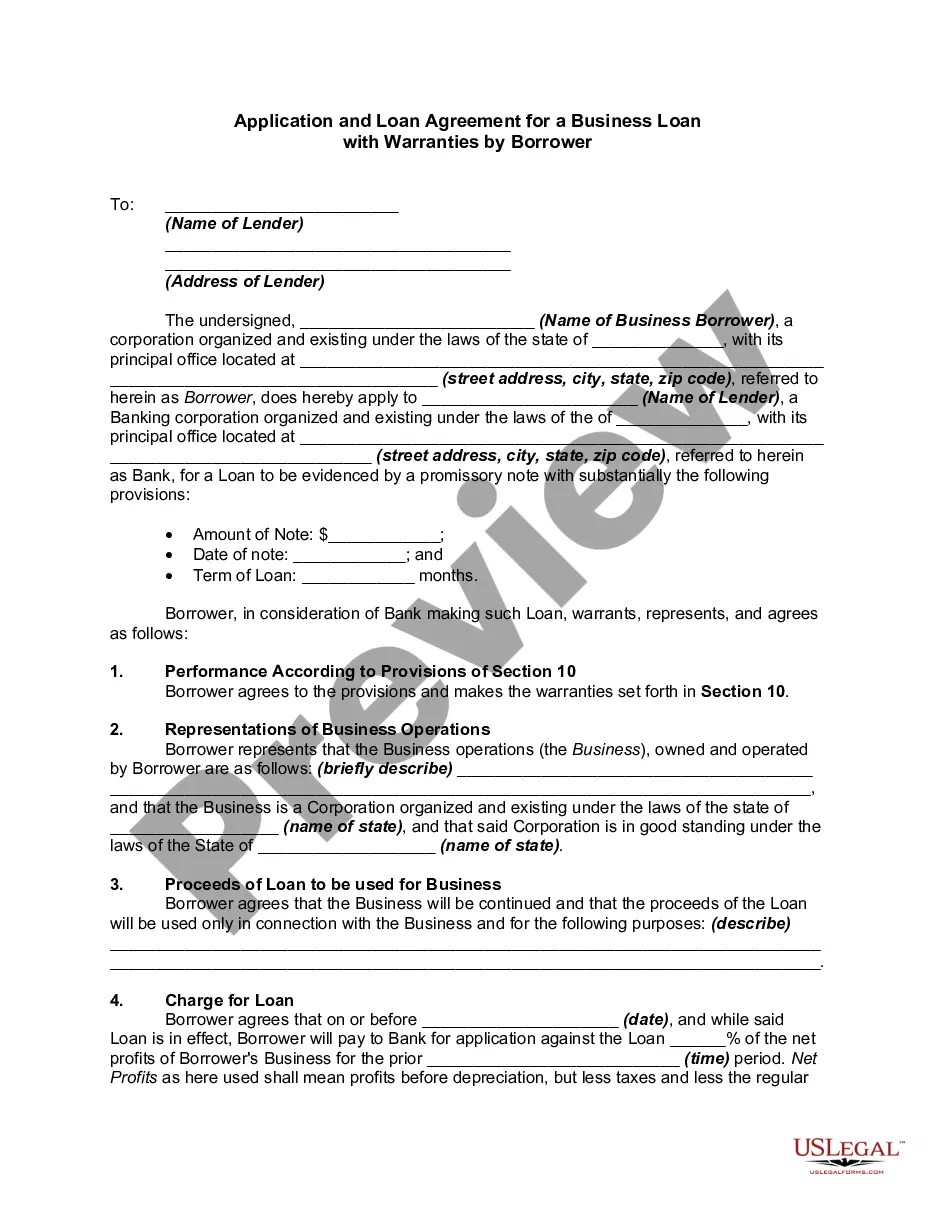

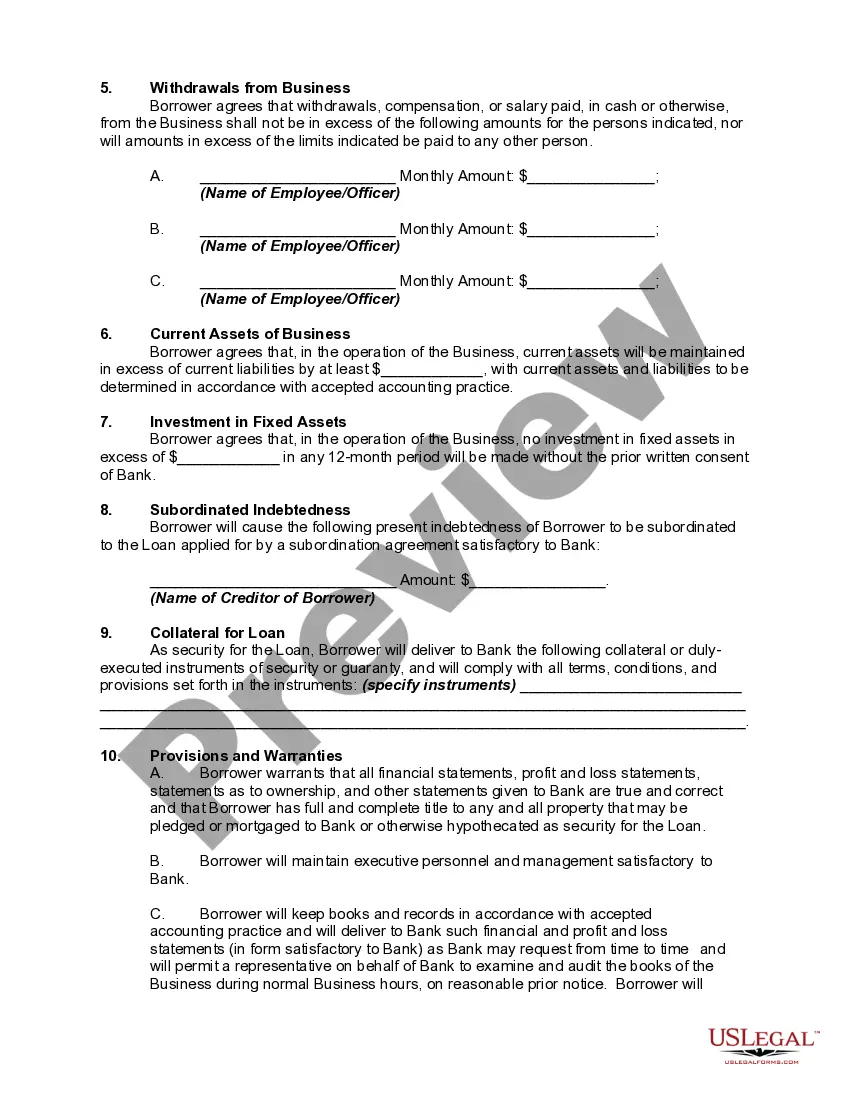

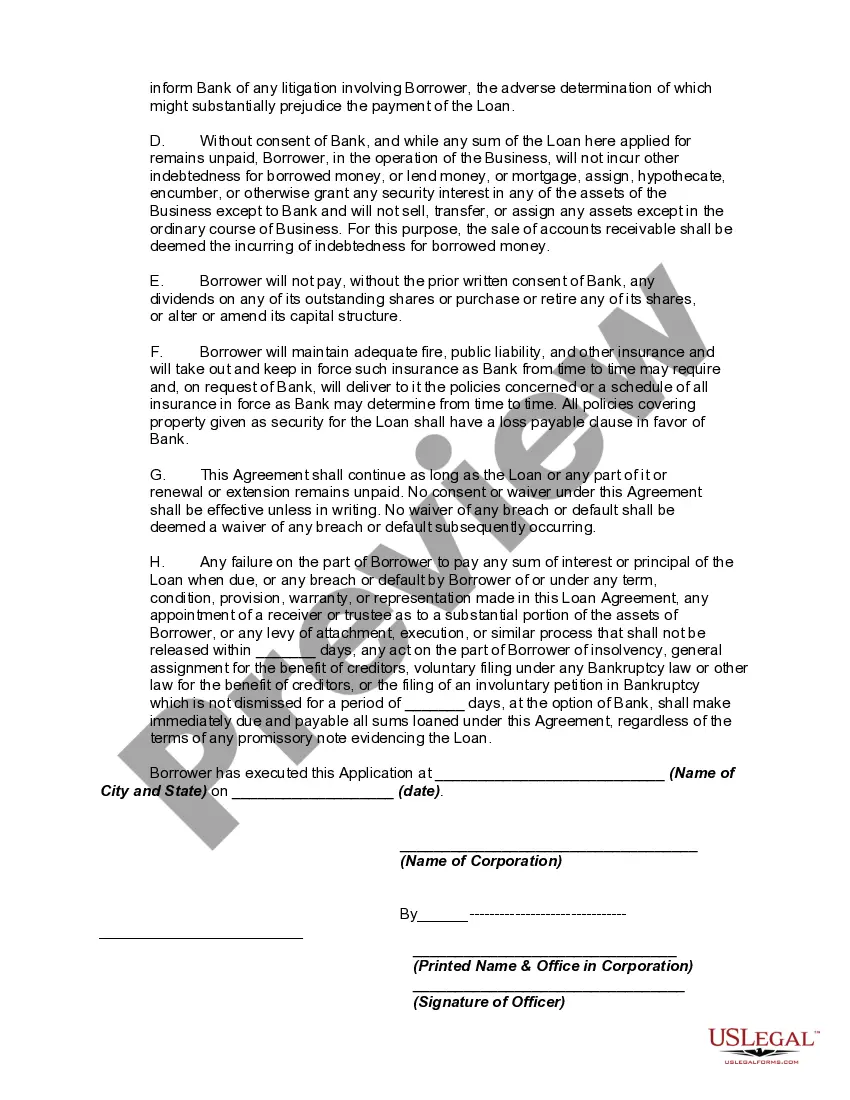

As a general matter, a loan by a bank is the borrowing of money by a person or entity who promises to return it on or before a specific date, with interest, or who pledges collateral as security for the loan and promises to redeem it at a specific later date. Loans are usually made on the basis of applications, together with financial statements submitted by the applicants.

The Federal Truth in Lending Act and the regulations promulgated under the Act apply to certain credit transactions, primarily those involving loans made to a natural person and intended for personal, family, or household purposes and for which a finance charge is made, or loans that are payable in more than four installments. However, said Act and regulations do not apply to a business loan of this type.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The Illinois Application and Loan Agreement for a Business Loan with Warranties by Borrower is a legally binding document used in the state of Illinois to formalize a business loan between a lender and borrower. This agreement outlines the terms and conditions of the loan, including the loan amount, interest rate, repayment terms, and the warranties provided by the borrower. Keywords: Illinois, Application and Loan Agreement, Business Loan, Warranties, Borrower. Different types of Illinois Application and Loan Agreement for a Business Loan with Warranties by Borrower may include: 1. Secured Loan Agreement: This type of agreement is used when the borrower provides collateral to secure the loan. The collateral can be in the form of assets, real estate, or personal guarantees. 2. Unsecured Loan Agreement: In this type of agreement, the loan is not backed by any collateral. The borrower relies solely on their creditworthiness and financial stability to obtain the loan. 3. Term Loan Agreement: A term loan agreement defines a specific period within which the loan must be repaid. It includes details such as repayment schedule, interest rates, and any penalties for early repayment or late payments. 4. Revolving Loan Agreement: This agreement establishes a line of credit that can be utilized by the borrower as needed. The borrower can withdraw funds up to a certain limit and repay them to replenish the available credit. 5. Small Business Administration (SBA) Loan Agreement: If the loan is obtained through the Small Business Administration, additional provisions may be included in the agreement to comply with the SBA's regulations and requirements. 6. Construction Loan Agreement: This type of agreement is used when the loan is specifically for construction purposes. It includes provisions related to disbursement of funds in stages, inspection requirements, and necessary documentation. 7. Working Capital Loan Agreement: When a business needs funds for day-to-day operations, a working capital loan agreement is used. It addresses how the funds can be used, repayment terms, and any restrictions or conditions related to the loan. These various types of loan agreements serve different purposes and may have specific clauses or warranties that cater to the unique circumstances of the borrower and lender.