An Illinois Loan Agreement refers to a legally binding contract between a lender and a borrower in the state of Illinois. This agreement outlines the terms and conditions under which a loan is provided, including the amount borrowed, interest rates, repayment schedule, and any applicable fees or penalties. The purpose of an Illinois Loan Agreement is to establish the rights and responsibilities of both parties involved, ensuring that each party understands their obligations and liabilities. This agreement serves as an important legal document that protects both the lender and the borrower in case of any disputes or defaults. There are various types of loan agreements in Illinois, catering to different lending situations and purposes. Some common types include: 1. Personal Loan Agreement: This agreement is used when an individual borrower obtains a loan for personal use, such as medical expenses, education fees, or financing a vacation. It typically outlines the repayment terms, interest rates, and any collateral provided by the borrower. 2. Business Loan Agreement: This type of agreement is specifically designed for commercial purposes, enabling businesses to borrow money for various needs, including expansion, equipment purchase, or working capital. The agreement may include details such as loan purpose, repayment terms, interest rates, and any business assets used as collateral. 3. Mortgage Loan Agreement: A mortgage loan agreement is used when the borrower intends to purchase a property and pledges the property as collateral for the loan. This agreement includes important details like loan amount, interest rates, repayment schedules, and specifics related to the property, such as its address, legal description, and any restrictions or covenants. 4. Auto Loan Agreement: When an individual borrows funds to finance the purchase of a vehicle, an auto loan agreement is utilized. This agreement outlines the terms of the loan, including repayment schedules, interest rates, and specifications regarding the vehicle being financed. 5. Payday Loan Agreement: Payday loans are short-term loans typically taken to cover unexpected expenses or bridge financial gaps until the borrower's next payday. Payday loan agreements in Illinois specify the loan amount, repayment terms, fees, and any restrictions or regulations imposed by the state on payday lending. Regardless of the type of loan agreement, it is essential for both parties to thoroughly read, understand, and negotiate the terms and conditions before signing the contract. Seeking legal advice or consulting with a financial professional is highly recommended ensuring compliance with Illinois laws and to protect the rights and interests of all parties involved in the loan transaction.

Illinois Loan Agreement

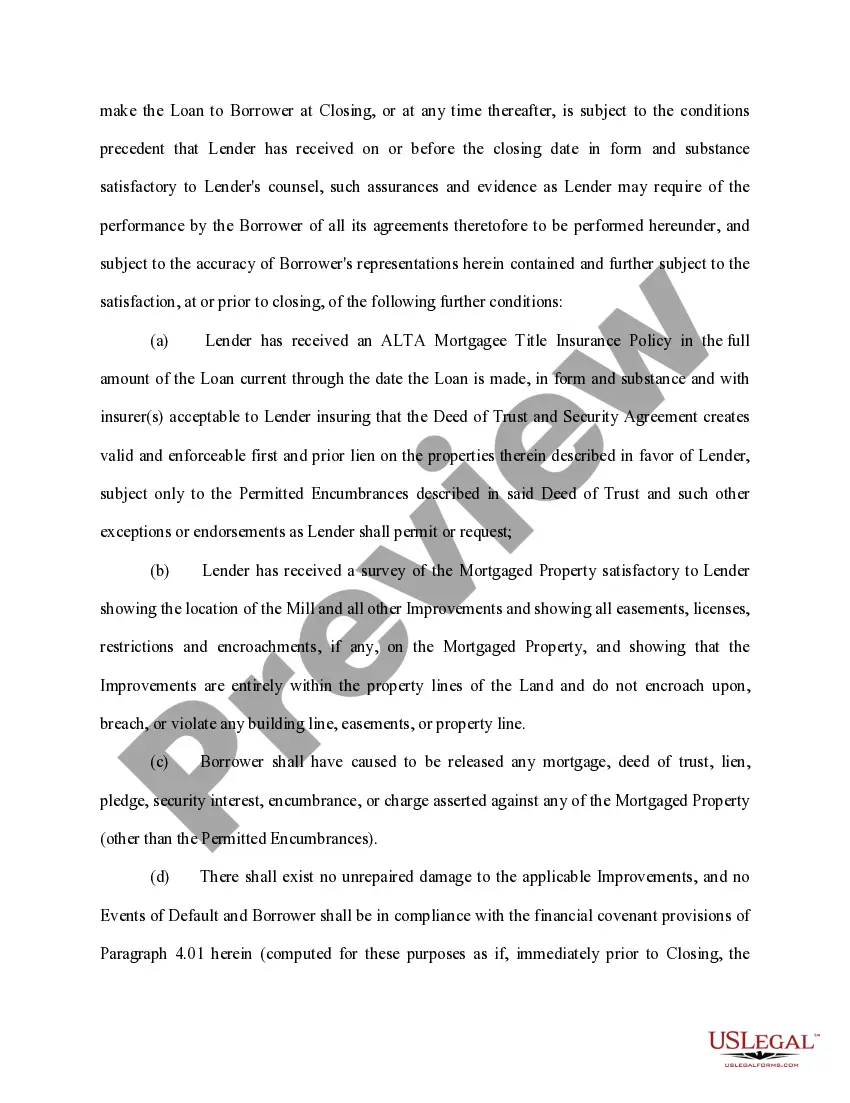

Description

How to fill out Illinois Loan Agreement?

You may commit several hours on-line attempting to find the legal papers format that suits the federal and state requirements you need. US Legal Forms gives a large number of legal varieties that happen to be evaluated by experts. It is simple to download or print out the Illinois Loan Agreement from our service.

If you currently have a US Legal Forms profile, you are able to log in and then click the Acquire option. After that, you are able to comprehensive, edit, print out, or indicator the Illinois Loan Agreement. Every legal papers format you acquire is your own forever. To get an additional version of the bought kind, go to the My Forms tab and then click the related option.

If you use the US Legal Forms website initially, stick to the straightforward instructions listed below:

- Initial, make sure that you have chosen the best papers format to the area/area of your liking. Browse the kind outline to make sure you have chosen the appropriate kind. If available, make use of the Preview option to look from the papers format at the same time.

- If you want to discover an additional edition from the kind, make use of the Lookup industry to get the format that meets your requirements and requirements.

- When you have discovered the format you want, just click Buy now to move forward.

- Pick the pricing strategy you want, type your accreditations, and register for a merchant account on US Legal Forms.

- Total the purchase. You may use your Visa or Mastercard or PayPal profile to cover the legal kind.

- Pick the formatting from the papers and download it in your gadget.

- Make changes in your papers if needed. You may comprehensive, edit and indicator and print out Illinois Loan Agreement.

Acquire and print out a large number of papers web templates utilizing the US Legal Forms site, that provides the greatest assortment of legal varieties. Use skilled and state-specific web templates to take on your organization or person requirements.