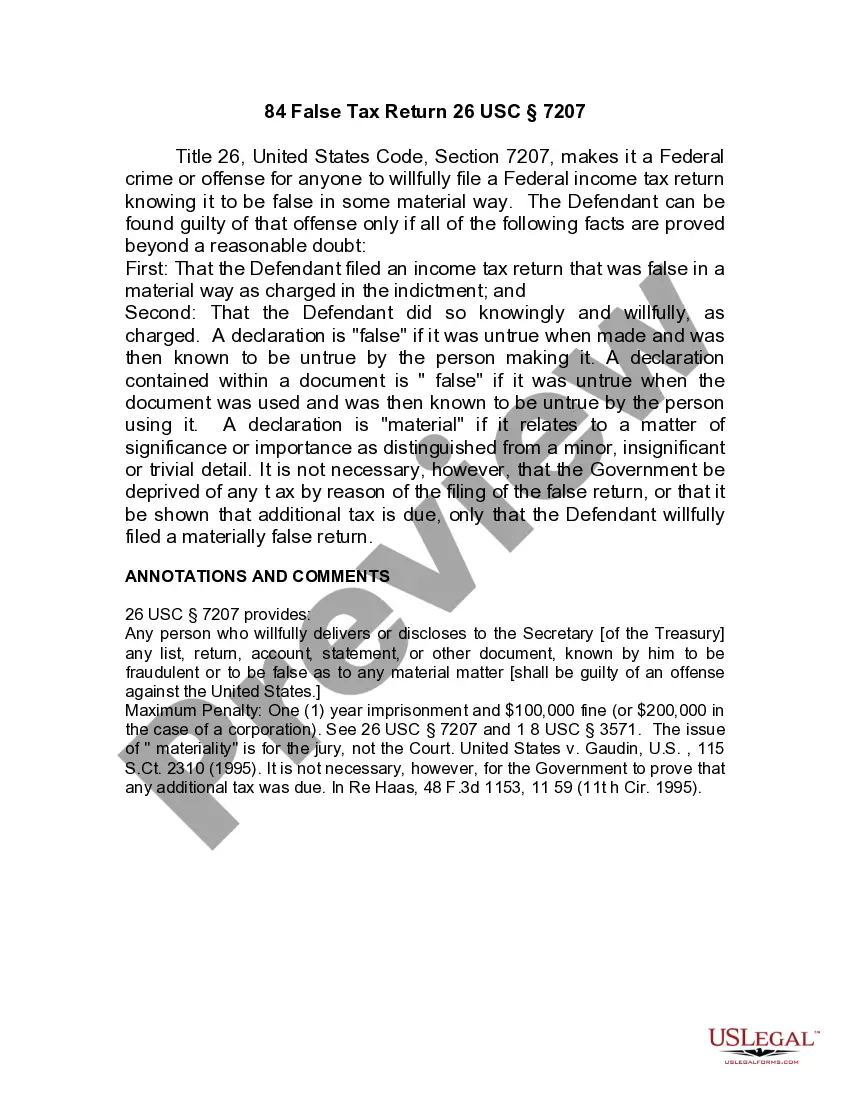

Illinois Jury Instruction - 10.10.6 Section 6672 Penalty

Description

How to fill out Jury Instruction - 10.10.6 Section 6672 Penalty?

Finding the right lawful file format can be a have a problem. Obviously, there are a variety of web templates available on the Internet, but how do you get the lawful form you need? Use the US Legal Forms web site. The services delivers a huge number of web templates, including the Illinois Jury Instruction - 10.10.6 Section 6672 Penalty, that you can use for company and private needs. All the forms are checked by professionals and meet state and federal needs.

In case you are already listed, log in to your account and click on the Down load button to get the Illinois Jury Instruction - 10.10.6 Section 6672 Penalty. Make use of your account to check through the lawful forms you possess bought earlier. Check out the My Forms tab of your own account and obtain an additional duplicate from the file you need.

In case you are a new customer of US Legal Forms, here are basic recommendations so that you can adhere to:

- Initially, ensure you have selected the proper form to your metropolis/county. You may look over the shape while using Preview button and read the shape information to make certain it will be the best for you.

- In case the form fails to meet your requirements, use the Seach discipline to get the proper form.

- Once you are positive that the shape is proper, click the Buy now button to get the form.

- Pick the pricing program you would like and type in the necessary information and facts. Create your account and pay for the order utilizing your PayPal account or charge card.

- Pick the submit format and acquire the lawful file format to your system.

- Total, modify and print and signal the attained Illinois Jury Instruction - 10.10.6 Section 6672 Penalty.

US Legal Forms is definitely the largest catalogue of lawful forms that you can find numerous file web templates. Use the service to acquire expertly-made paperwork that adhere to condition needs.

Form popularity

FAQ

Nature, Extent, and Duration of Injury Rather, any award for one of the various elements of damages (such as disability, pain and suffering, lost wages, etc.) must involve, and be based upon, an assessment of the nature, extent, and duration of the claimant's injuries. Powers v. Illinois C. G. R.

Illinois Pattern Jury Instruction (I.P.I.) 30.04. 02 defines loss of a normal life, as ?When I use the expression ?loss of a normal life,? I mean the temporary or permanent diminished ability to enjoy life. This includes a person's inability to pursue the pleasurable aspects of life.?

This term specifically relates to personal injury cases, when a defendant's negligence or reckless behavior causes the victim's family to lose a connection with the victim. Loss of consortium cases happen when a partner or family lose the joys of companionship, affection, love, comfort, or sexual intimacy.

Undue Influence Influence is ?undue? when it ?prevents the testator from exercising his own will in the disposition of his estate? such that the testator's will is rendered more the will of another. Id., 69 Ill. Dec. at 963.

30.04.02 Loss of a Normal Life--Definition This includes a person's inability to pursue the pleasurable aspects of life.