Illinois Cooperative Loan Recognition Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Cooperative Loan Recognition Agreement?

It is possible to invest hrs on the Internet attempting to find the legal record format that meets the state and federal demands you want. US Legal Forms offers thousands of legal forms that are examined by professionals. You can actually obtain or print the Illinois Cooperative Loan Recognition Agreement from your services.

If you have a US Legal Forms accounts, you may log in and click on the Obtain switch. Afterward, you may comprehensive, change, print, or indication the Illinois Cooperative Loan Recognition Agreement. Every single legal record format you purchase is your own forever. To get one more backup associated with a purchased type, go to the My Forms tab and click on the related switch.

If you are using the US Legal Forms internet site the first time, stick to the simple directions below:

- Initial, make certain you have selected the right record format for your area/area of your choice. Look at the type information to make sure you have picked out the correct type. If available, use the Review switch to check with the record format as well.

- If you would like locate one more variation of the type, use the Look for field to discover the format that fits your needs and demands.

- Once you have identified the format you desire, just click Buy now to proceed.

- Choose the costs plan you desire, enter your credentials, and register for an account on US Legal Forms.

- Total the financial transaction. You can use your charge card or PayPal accounts to fund the legal type.

- Choose the format of the record and obtain it to your device.

- Make changes to your record if required. It is possible to comprehensive, change and indication and print Illinois Cooperative Loan Recognition Agreement.

Obtain and print thousands of record layouts using the US Legal Forms site, which provides the most important collection of legal forms. Use skilled and express-specific layouts to deal with your business or person needs.

Form popularity

FAQ

There are numerous benefits to having a recognition agreement in place. Benefits include: Being able to negotiate on terms and conditions (including pay, hours worked and holidays). Improved policies and company procedures on flexible working and employee health. Recognition agreements - Community Trade Union community-tu.org ? mymembership ? advice-centre community-tu.org ? mymembership ? advice-centre

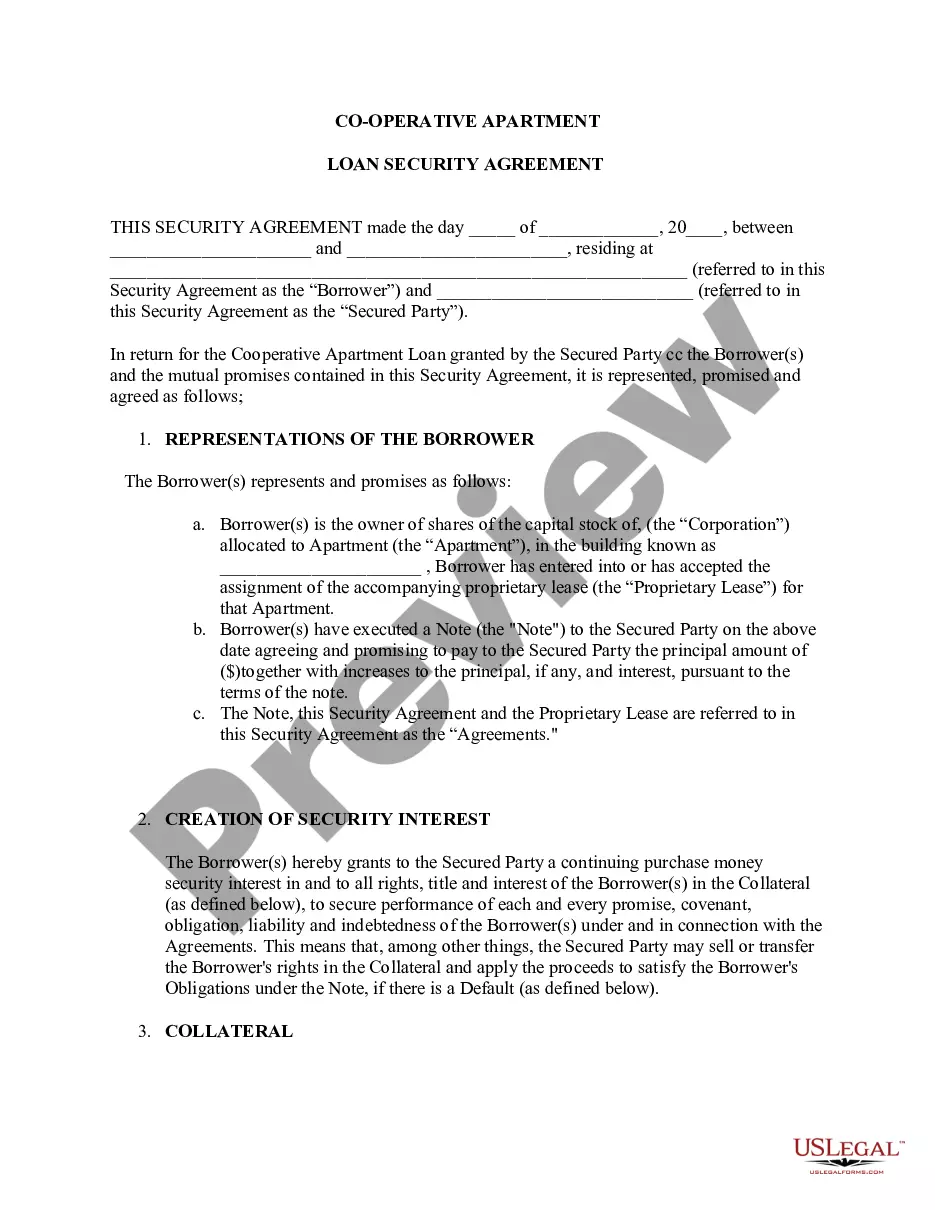

Assignment of Recognition Agreement . With respect to a Cooperative Loan, an assignment of the Recognition Agreement sufficient under the laws of the jurisdiction wherein the related Cooperative Unit is located to reflect the assignment of such Recognition Agreement.

A recognition agreement names the union or unions who have rights to represent and negotiate on behalf of employees in that workplace. A NEGOTIATOR'S GUIDE TO RECOGNITION AGREEMENTS International Labour Organization ? inwork ? cb-policy-guide International Labour Organization ? inwork ? cb-policy-guide PDF

The stock, shares, membership certificates, or other contractual agreement evidencing ownership. The original Recognition Agreement, and, if applicable, the original assignment of the Recognition Agreement to the lender.

In a nutshell therefore Collective agreements deal with procedural and substantive issues that are of common interest to management and workers whereas the purpose of a recognition agreement is to allow the employer to strictly control the activities of the union and business leaders. differences between recognition agreement and collective ... academia.edu ? DIFFERENCES_BETWEEN... academia.edu ? DIFFERENCES_BETWEEN...

Recognition Agreement means, with respect to a Cooperative Mortgage Loan, an agreement executed by a Cooperative Corporation which, among other things, acknowledges the lien of the Mortgage on the Mortgaged Property in question.

A recognition agreement is a legal document that allows parties to recognize each other's interests in an agreement. This document could be used in co-op unit financing, a union negotiation, between borrowers and lenders for a loan, and for other purposes.

Lender Recognition Agreement means an agreement in form and substance satisfactory to the Landlord between the Landlord, Tenant and a Leasehold Mortgagee pursuant to which the Landlord undertakes in favor of the Leasehold Mortgagee that in the event of a default by Tenant the Landlord will recognize the Leasehold ... Lender Recognition Agreement Definition - Law Insider Law Insider ? dictionary ? lender-reco... Law Insider ? dictionary ? lender-reco...