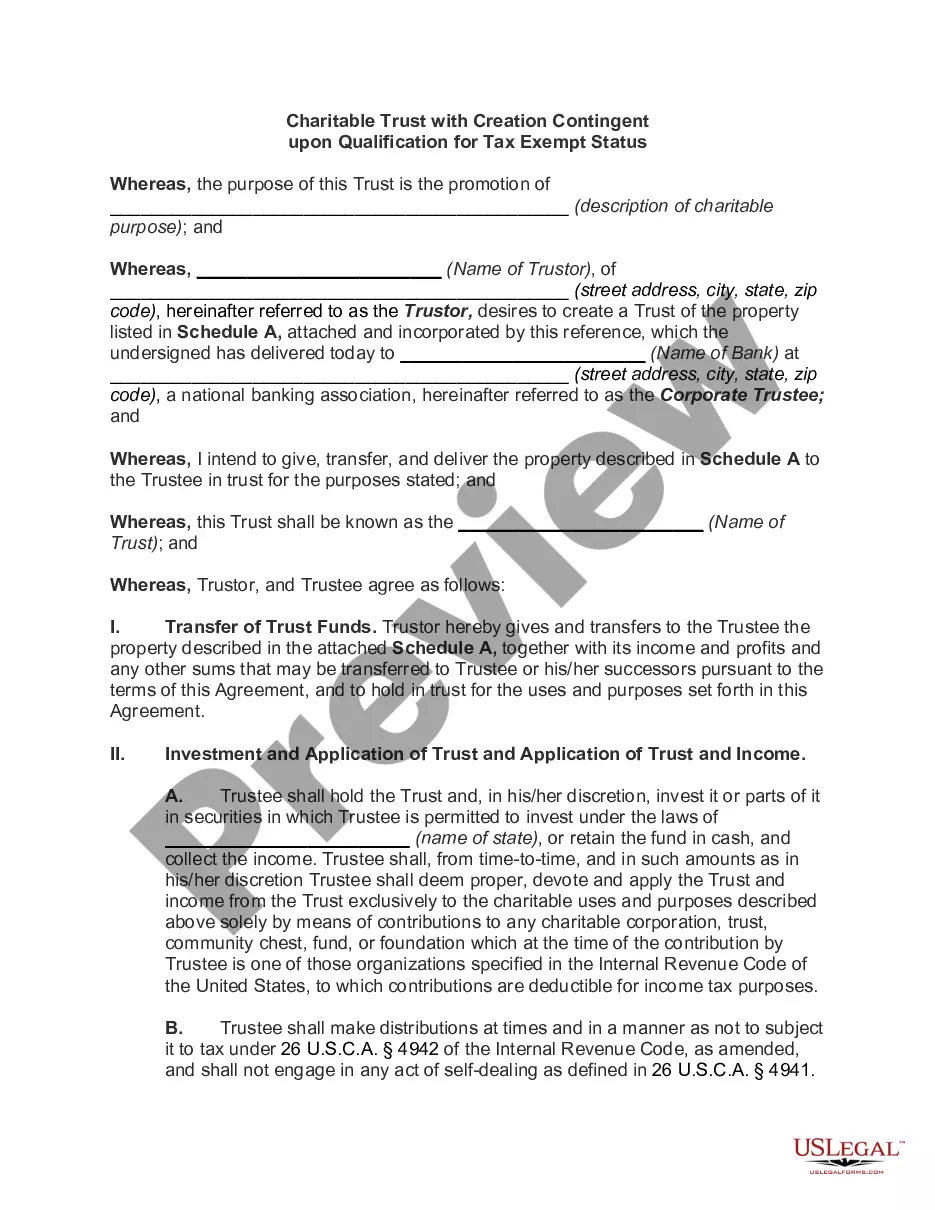

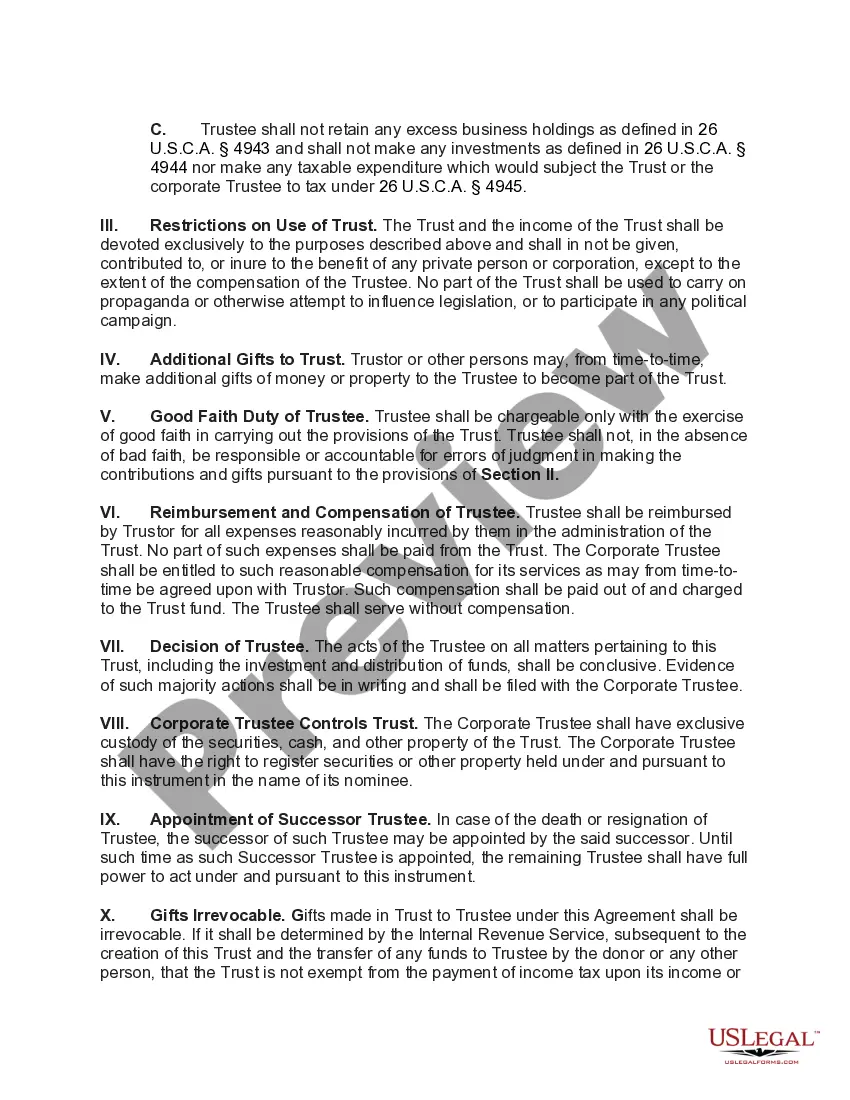

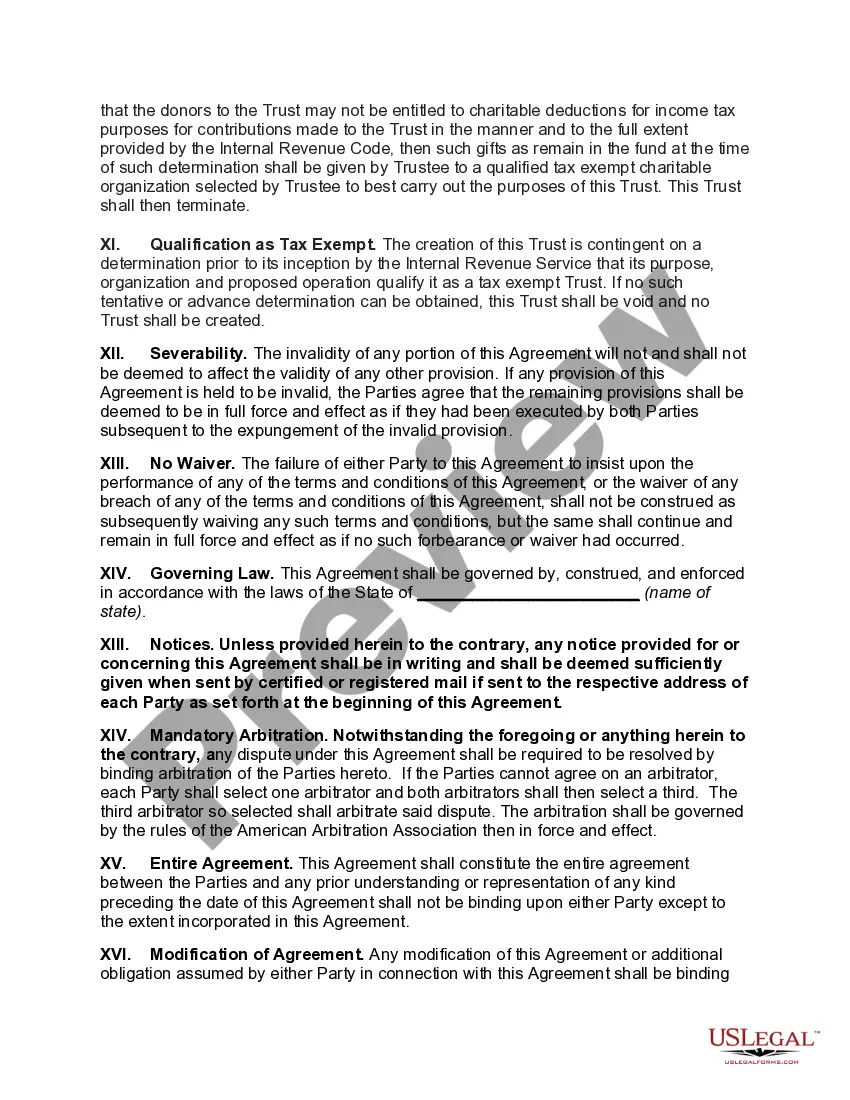

Title: Exploring Illinois Charitable Trusts with Creation Contingent upon Qualification for Tax Exempt Status Introduction: In Illinois, Charitable Trusts with Creation Contingent upon Qualification for Tax Exempt Status play a vital role in supporting philanthropic endeavors while providing potential tax benefits for donors. This detailed description dives into the nature and types of these trusts available in Illinois, emphasizing their significance in contributing to the betterment of society. Keywords: Illinois, charitable trust, creation, contingent, qualification, tax-exempt status. 1. Understanding Illinois Charitable Trusts: Illinois Charitable Trust refers to a legal entity created to benefit one or more charitable causes or organizations. These trusts are subject to specific regulations and guidelines outlined by the Illinois Charitable Trust Act. 2. Creation Contingent upon Qualification: For a Charitable Trust to be established in Illinois, the creation of the trust is contingent upon the qualification of the trust as tax-exempt under Section 501(c)(3) of the Internal Revenue Code (IRC). This means that the trust must obtain tax-exempt status from the IRS to carry out its charitable purpose. 3. Tax Exempt Status Benefits: By qualifying for tax-exempt status, a Charitable Trust gains numerous advantages, including: — Tax Deductions: Donors who contribute to tax-exempt charitable trusts may be eligible for tax deductions on their federal income tax returns. This incentive encourages philanthropy and can potentially reduce donors' tax liabilities. — Exemption from Income Taxes: Once a Charitable Trust secures tax-exempt status, it becomes exempt from federal income taxes, allowing a greater portion of the trust's funds to be utilized for charitable purposes. 4. Types of Illinois Charitable Trusts: There are several types of Charitable Trusts available in Illinois, each tailored to suit specific charitable objectives. Some common examples include: — Charitable Remainder Trust (CRT): A CRT allows donors to contribute assets to the trust, receive income from the trust for a specified period, and, upon termination, distribute the remaining assets to the designated charitable organization. — Charitable Lead Trust (CLT): In a CLT, the trust pays a fixed amount or percentage of its assets to one or more charitable organizations for a specific period. After this period, the remaining assets are distributed to non-charitable beneficiaries, such as family members. — Pooled Income Fund (PIF): A PIF combines donations from multiple donors into a single trust. Donors receive income based on their contribution's share, with the remaining assets benefiting the designated charitable cause. — Testamentary Charitable Remainder Trust (CRT): Created through a will, this trust comes into effect upon the donor's death. It allows the donor's designated beneficiary to receive income for life or a set period. Afterward, the remaining assets pass to the charitable organization. Conclusion: Illinois Charitable Trusts with Creation Contingent upon Qualification for Tax Exempt Status offer a structured approach to support charitable causes while providing potential tax benefits for donors. Understanding the nuances and types of these trusts empowers individuals and organizations to make informed decisions that align with their philanthropic goals and contribute positively to society.

Illinois Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status

Description

How to fill out Illinois Charitable Trust With Creation Contingent Upon Qualification For Tax Exempt Status?

US Legal Forms - one of the greatest libraries of authorized varieties in the United States - delivers an array of authorized record web templates you can download or print out. Utilizing the web site, you can get thousands of varieties for company and personal uses, categorized by categories, states, or search phrases.You can find the most recent versions of varieties much like the Illinois Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status within minutes.

If you already have a monthly subscription, log in and download Illinois Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status through the US Legal Forms collection. The Obtain option can look on each and every develop you see. You get access to all earlier downloaded varieties within the My Forms tab of the accounts.

If you wish to use US Legal Forms the first time, allow me to share simple instructions to help you get started:

- Be sure you have picked the right develop to your town/county. Select the Review option to check the form`s content. Browse the develop explanation to ensure that you have selected the correct develop.

- In the event the develop does not fit your demands, take advantage of the Research discipline at the top of the display screen to obtain the one that does.

- If you are happy with the form, confirm your decision by simply clicking the Acquire now option. Then, select the rates prepare you prefer and supply your accreditations to sign up for the accounts.

- Method the transaction. Use your Visa or Mastercard or PayPal accounts to perform the transaction.

- Find the format and download the form on your own device.

- Make modifications. Fill out, change and print out and indication the downloaded Illinois Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status.

Each template you included with your account does not have an expiry day which is the one you have forever. So, if you want to download or print out yet another copy, just proceed to the My Forms portion and click in the develop you will need.

Gain access to the Illinois Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status with US Legal Forms, probably the most considerable collection of authorized record web templates. Use thousands of expert and express-specific web templates that meet up with your small business or personal needs and demands.