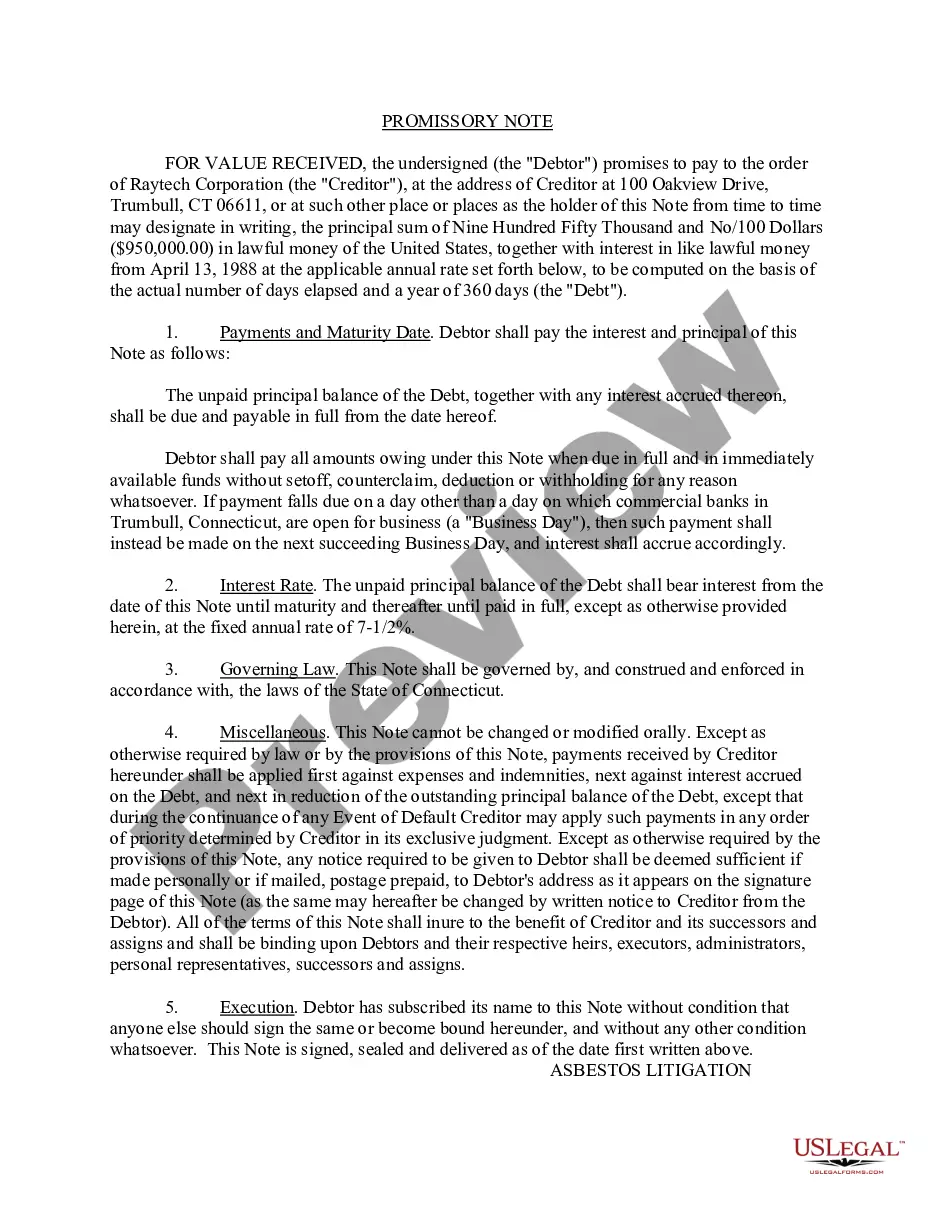

Illinois Promissory Note: A Comprehensive Guide to Types and Key Points A Promissory Note is a legally binding document that establishes a promise to repay a specific amount of money. In Illinois, a Promissory Note is commonly used in various financial transactions, including personal loans, student loans, business financing, and real estate transactions. This article aims to provide a detailed description of what an Illinois Promissory Note entails, including its key features, types, and important components. Key Features of an Illinois Promissory Note: 1. Promise to Repay: A Promissory Note clearly states the borrower's commitment to repay the lender a specific sum of money, along with interest (if applicable), over a predetermined period. 2. Interest Rate: It specifies the interest rate charged on the loan, the method of computation (simple or compound interest), and whether it is a fixed or variable rate. 3. Loan Amount and Tenure: The Note contains the principal loan amount disbursed to the borrower and the agreed-upon repayment schedule, including the installment amount and frequency. 4. Parties Involved: It identifies the lender (also known as the payee or note holder) and borrower (also known as the maker or mayor) with their legal names, addresses, and contact information. 5. Collateral and Security: If applicable, the Promissory Note may outline any collateral or security provided by the borrower to secure the loan. 6. Late Payment and Default: The Note may include provisions specifying the consequences of late payments, default, and the remedies available to the lender, such as late fees or acceleration of the debt. 7. Governing Law and Jurisdiction: It establishes that the Promissory Note follows the laws of the state of Illinois and identifies the appropriate jurisdiction in case of any legal disputes. Types of Illinois Promissory Notes: 1. Simple Promissory Note: This type of Promissory Note outlines the basic terms of the loan, including the loan amount, repayment terms, and interest rate. It does not involve any collateral. 2. Secured Promissory Note: This Note includes provisions for collateral or security provided by the borrower, ensuring that assets can be seized in the event of default. 3. Unsecured Promissory Note: Unlike a secured note, this type of Promissory Note does not involve any collateral, relying solely on the borrower's creditworthiness and trustworthiness. 4. Installment Promissory Note: It divides loan repayment into a series of payments (installments) over a specified period, with each payment comprising both principal and interest. 5. Balloon Promissory Note: This Note involves smaller periodic payments for the majority of the loan tenure, with a significantly larger payment (known as the balloon payment) due at the loan's end, often used in real estate financing. In conclusion, an Illinois Promissory Note serves as a crucial legal instrument for defining and formalizing loans between parties. It is essential to understand the different types of Promissory Notes available, their key features, and components to ensure compliance with relevant laws and regulations in Illinois. Seeking legal advice or assistance from a qualified professional is recommended when drafting or entering into a Promissory Note to protect the interests of all parties involved.

Illinois Promissory Note

Description

How to fill out Illinois Promissory Note?

Finding the right lawful file template could be a struggle. Of course, there are tons of templates available on the Internet, but how would you discover the lawful type you require? Make use of the US Legal Forms website. The service offers 1000s of templates, including the Illinois Promissory Note, which can be used for enterprise and personal demands. Each of the kinds are checked by experts and meet state and federal specifications.

Should you be previously authorized, log in to the account and click on the Download option to have the Illinois Promissory Note. Make use of your account to look from the lawful kinds you might have bought previously. Check out the My Forms tab of the account and get one more backup of the file you require.

Should you be a whole new customer of US Legal Forms, here are basic directions that you should comply with:

- Initial, ensure you have chosen the proper type for your area/area. It is possible to look over the form making use of the Preview option and browse the form information to make certain it will be the right one for you.

- When the type does not meet your requirements, use the Seach field to discover the proper type.

- Once you are certain the form is proper, click on the Acquire now option to have the type.

- Opt for the costs prepare you would like and type in the required info. Create your account and buy your order making use of your PayPal account or bank card.

- Pick the document formatting and acquire the lawful file template to the gadget.

- Total, change and produce and indication the acquired Illinois Promissory Note.

US Legal Forms will be the most significant collection of lawful kinds where you can see numerous file templates. Make use of the company to acquire skillfully-made files that comply with condition specifications.

Form popularity

FAQ

In Illinois, a promissory note does not need a notary or witness. The good thing with a promissory note today is that you don't have to contact an attorney to get the template.

Promissory notes are legally binding contracts that can hold up in court if the terms of borrowing and repayment are signed and follow applicable laws.

The state of Illinois, like every other state in the U.S., has its statute of limitations for various types of debts. All unwritten and open-ended agreements, for example, have a five-year expiration. Written contracts and promissory notes, on the other hand, have a 10-year expiration.

Promissory notes don't have to be notarized in most cases. You can typically sign a legally binding promissory note that contains unconditional pledges to pay a certain sum of money. However, you can strengthen the legality of a valid promissory note by having it notarized.

A promissory note could become invalid if: It isn't signed by both parties. The note violates laws. One party tries to change the terms of the agreement without notifying the other party.

Promissory notes may also be referred to as an IOU, a loan agreement, or just a note. It's a legal lending document that says the borrower promises to repay to the lender a certain amount of money in a certain time frame. This kind of document is legally enforceable and creates a legal obligation to repay the loan.

Promissory note is supported by a consideration as recited in the negotiable instrument and the evidence adduced in support therefor, the burden is on the defendant to disprove that the promissory note is ... summarised as follows:??Negotiable Instruments Act, S.

To be legally enforceable, a promissory note must meet multiple legal conditions. Moreover, it must contain both an offer of agreement and an acceptance of agreement. All contracts state the type of services or goods rendered and indicate how much they cost.