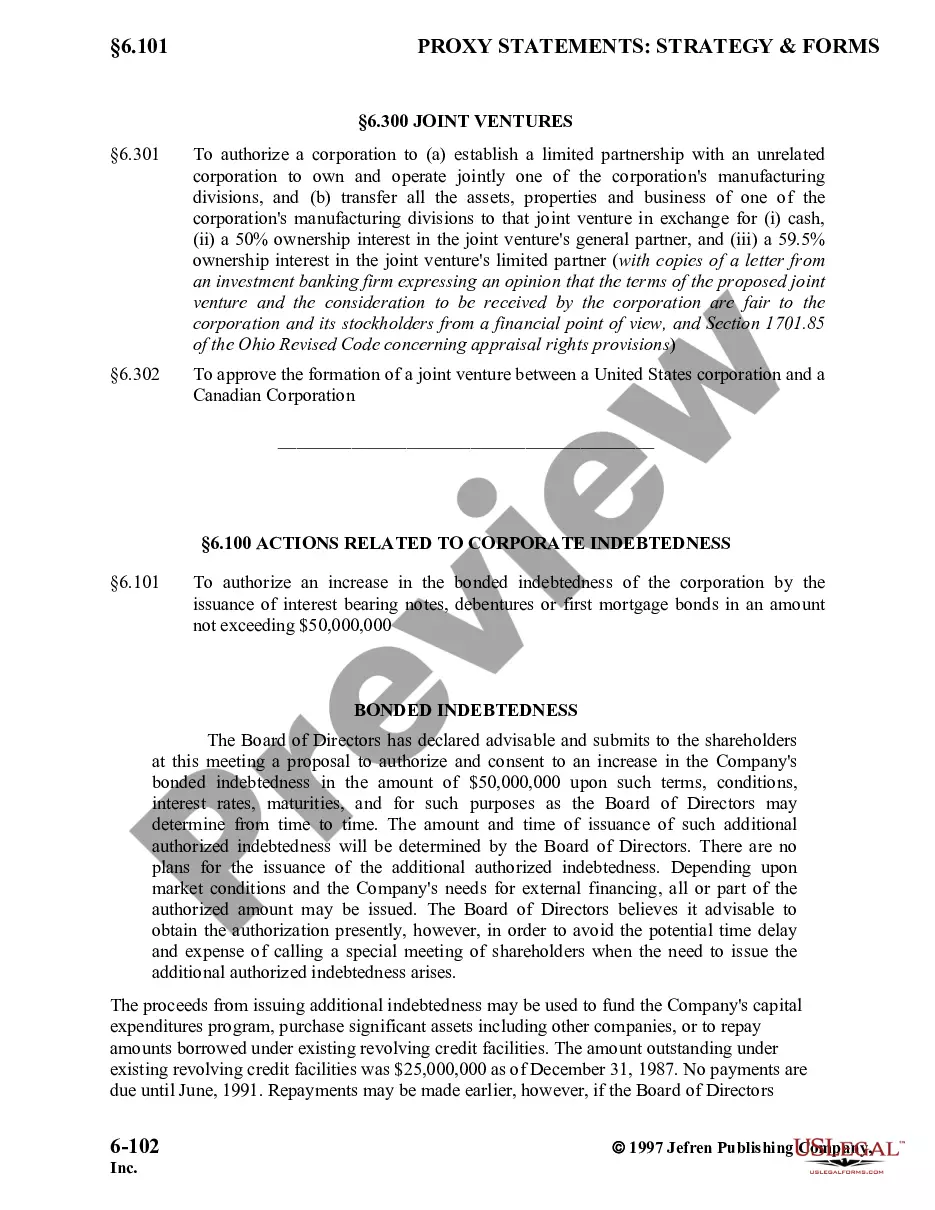

Illinois Authorization to Increase Bonded Indebtedness is a legal process that allows the state of Illinois to raise the limit on the amount of bonded indebtedness it can incur. This authorization is necessary when the state needs additional funds for various reasons, such as funding infrastructure projects, improving public facilities, or addressing budget deficits. By obtaining authorization to increase bonded indebtedness, Illinois can effectively borrow money from investors by issuing bonds. These bonds function as a loan from investors to the state, with the promise of repayment over a predetermined period of time, usually with interest. The process of obtaining authorization involves a formal approval from the Illinois General Assembly, which is the state's legislative body. The General Assembly must pass a bill that specifies the details of the authorization, including the maximum amount of bonded indebtedness that the state can incur. There are different types of Illinois Authorization to Increase Bonded Indebtedness: 1. General Obligation Bonds: These are bonds issued by the state, backed by the full faith and credit of the state's taxing authority. This means that the state pledges to use its taxing power to repay bondholders if other revenue sources are insufficient. 2. Revenue Bonds: Unlike general obligation bonds, revenue bonds are backed by specific revenue sources, such as tolls, fees, or dedicated taxes. The repayment of these bonds comes directly from the revenue generated by the project or entity for which the bonds were issued. 3. Capital Appreciation Bonds: Capital appreciation bonds differ from traditional bonds as they do not require periodic interest payments. Instead, the interest is compounded, and the bondholder receives the full amount, including interest, upon maturity. It is essential for the state to carefully consider the implications of increasing bonded indebtedness, as it directly impacts the state's financial obligations and ability to repay its debts. The authorization process provides a way for the state to maintain fiscal responsibility while still meeting its funding needs. In conclusion, Illinois Authorization to Increase Bonded Indebtedness is a crucial mechanism that allows the state to secure additional funds through the issuance of bonds. Different types of bonds, such as general obligation bonds, revenue bonds, and capital appreciation bonds, offer varying repayment structures and sources of revenue. However, it is imperative that the state carefully manages its bonded indebtedness to ensure long-term fiscal stability.

Illinois Authorization to increase bonded indebtedness

Description

How to fill out Illinois Authorization To Increase Bonded Indebtedness?

You are able to invest time on the Internet looking for the legal document template which fits the state and federal demands you need. US Legal Forms provides thousands of legal varieties that happen to be reviewed by pros. It is simple to obtain or printing the Illinois Authorization to increase bonded indebtedness from our service.

If you have a US Legal Forms accounts, you can log in and click the Download key. Afterward, you can comprehensive, modify, printing, or indicator the Illinois Authorization to increase bonded indebtedness. Every single legal document template you get is your own property for a long time. To obtain one more backup for any purchased kind, visit the My Forms tab and click the related key.

If you work with the US Legal Forms internet site for the first time, follow the basic recommendations beneath:

- Initial, ensure that you have selected the correct document template for that state/town that you pick. Browse the kind outline to make sure you have selected the right kind. If readily available, take advantage of the Preview key to appear with the document template as well.

- If you want to locate one more model in the kind, take advantage of the Lookup field to discover the template that meets your needs and demands.

- After you have found the template you need, click on Get now to carry on.

- Choose the pricing strategy you need, key in your qualifications, and register for a free account on US Legal Forms.

- Total the financial transaction. You can use your bank card or PayPal accounts to fund the legal kind.

- Choose the formatting in the document and obtain it to the system.

- Make adjustments to the document if necessary. You are able to comprehensive, modify and indicator and printing Illinois Authorization to increase bonded indebtedness.

Download and printing thousands of document themes using the US Legal Forms site, which offers the biggest collection of legal varieties. Use professional and state-distinct themes to take on your business or individual requires.