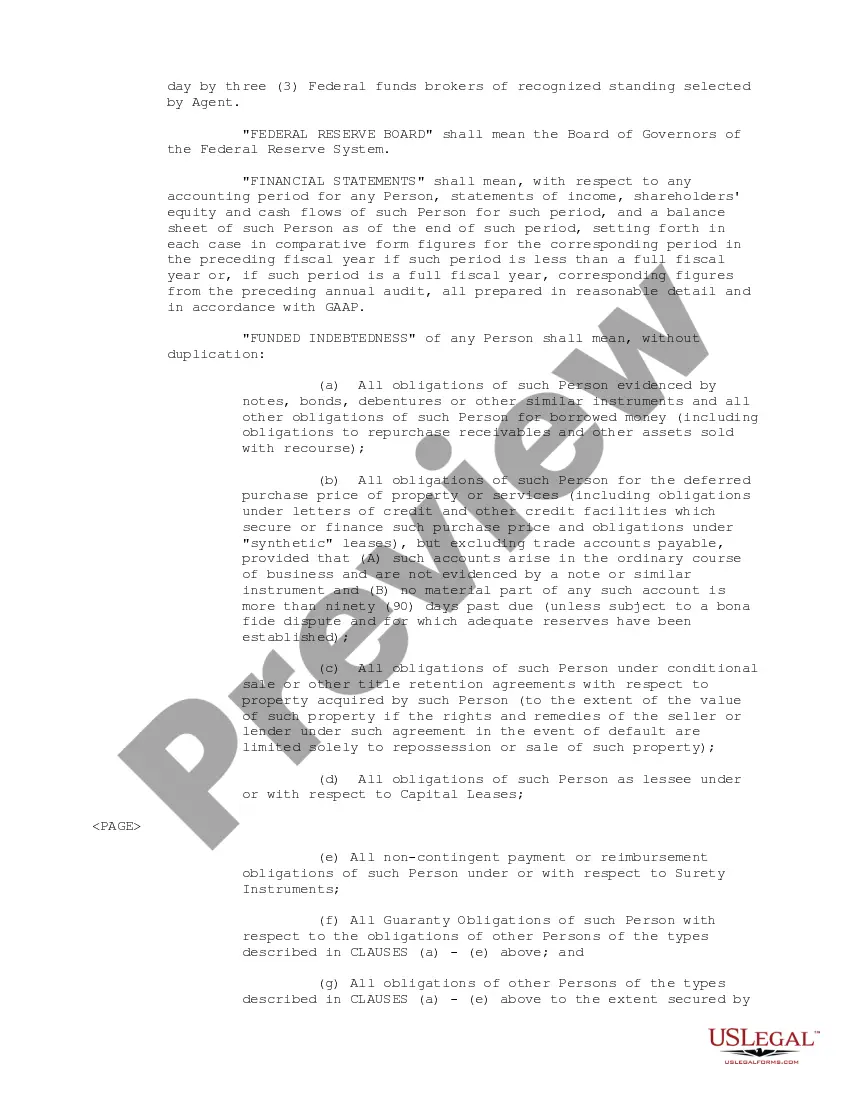

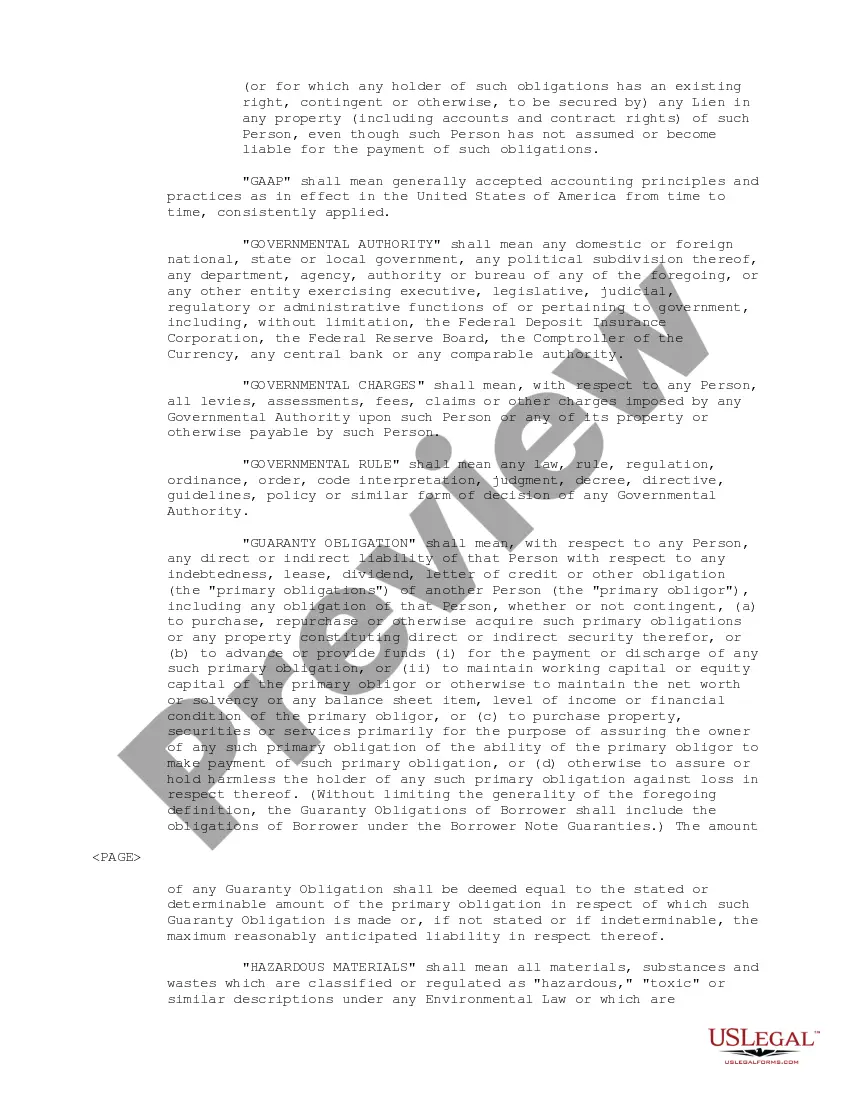

Title: Understanding the Illinois Amended and Restated Credit Agreement between ADAC Laboratories, various financial institutions, and ABN AFRO Bank Introduction: The Illinois Amended and Restated Credit Agreement is a legally binding document that establishes a financial arrangement between ADAC Laboratories, various financial institutions, and ABN AFRO Bank. This agreement outlines the terms and conditions for the provision of credit facilities and the management of financial transactions. Within the realm of Illinois Amended and Restated Credit Agreements, there can be various types available based on the specific terms and structure of the agreement. Let's delve into the details: 1. Types of Illinois Amended and Restated Credit Agreements: a) Revolving Credit Facility: This type of agreement provides ADAC Laboratories with flexible access to a predetermined credit limit. It allows multiple borrowings and repayments within the agreed-upon time frame. b) Term Loan Facility: In this arrangement, ADAC Laboratories receives a lump sum loan amount from ABN AFRO Bank or the participating financial institutions, which must be repaid in installments over a specified period. The interest rates, repayment schedule, and collateral requirements are defined within this type of agreement. c) Syndicated Credit Facility: Syndicated credit agreements involve the participation of multiple financial institutions to provide a considerable credit amount to ADAC Laboratories. ABN AFRO Bank serves as the administrative agent for coordinating this arrangement, which distributes the credit risk among the participating lenders. d) Secured Credit Agreement: A secured credit agreement requires ADAC Laboratories to pledge specific assets or collateral in favor of ABN AFRO Bank or the participating financial institutions. This provides added security to the lenders in case of default. e) Unsecured Credit Agreement: In contrast to secured credit agreements, unsecured credit agreements do not require ADAC Laboratories to provide collateral. Instead, they rely on the borrower's general creditworthiness and financial standing. Key Elements of the Illinois Amended and Restated Credit Agreement: a) Borrowing Limits: This section outlines the maximum amount of credit available to ADAC Laboratories, often referred to as the "commitment amount." b) Interest Rates: The agreement specifies the interest rates that ADAC Laboratories must pay on the borrowed funds. These rates may be fixed or variable, depending on the agreement's terms. c) Repayment Terms: The repayment schedule, including the frequency and amount of installments, is defined in detail. It may be monthly, quarterly, or annually, depending on the agreement. d) Conditions Precedent: These are the conditions that must be met before ADAC Laboratories can access the credit facility. It may include submitting financial statements, complying with certain financial ratios, or obtaining regulatory approvals. e) Representations and Warranties: This portion includes the borrower's declarations regarding the accuracy of the provided information, absence of any default, and compliance with laws and regulations. f) Covenants: These are the promises made by ADAC Laboratories to the lenders, ensuring specific actions or prohibiting certain activities during the duration of the agreement. Covenants may relate to financial reporting, financial ratios, debt occurrence, or asset disposal. g) Events of Default: This section specifies the circumstances under which the lender can declare a default and take appropriate actions, such as accelerating the loan repayment or suing for recovery. Conclusion: The Illinois Amended and Restated Credit Agreement defines the terms and conditions for credit facilities provided by ABN AFRO Bank and various financial institutions to ADAC Laboratories. By understanding the various types of agreements available, along with their key elements, ADAC Laboratories can effectively manage their financial transactions and fulfill their obligations within the framework of this credit agreement.

Illinois Amended and Restated Credit Agreement between ADAC Laboratories, various financial institution and ABN AMRO Bank

Description

How to fill out Illinois Amended And Restated Credit Agreement Between ADAC Laboratories, Various Financial Institution And ABN AMRO Bank?

Have you been inside a situation that you need files for possibly enterprise or personal uses just about every day time? There are a variety of lawful file layouts available online, but discovering types you can depend on is not effortless. US Legal Forms delivers thousands of develop layouts, such as the Illinois Amended and Restated Credit Agreement between ADAC Laboratories, various financial institution and ABN AMRO Bank, which can be created to satisfy federal and state needs.

Should you be already informed about US Legal Forms internet site and possess a merchant account, just log in. After that, you can down load the Illinois Amended and Restated Credit Agreement between ADAC Laboratories, various financial institution and ABN AMRO Bank format.

Unless you offer an bank account and would like to start using US Legal Forms, follow these steps:

- Discover the develop you require and ensure it is to the proper town/region.

- Take advantage of the Review key to examine the shape.

- Browse the information to ensure that you have chosen the appropriate develop.

- When the develop is not what you are searching for, make use of the Research field to get the develop that fits your needs and needs.

- Once you find the proper develop, just click Buy now.

- Select the rates plan you desire, fill in the required information to make your account, and purchase an order making use of your PayPal or Visa or Mastercard.

- Pick a hassle-free paper formatting and down load your backup.

Discover all of the file layouts you might have purchased in the My Forms menus. You can obtain a additional backup of Illinois Amended and Restated Credit Agreement between ADAC Laboratories, various financial institution and ABN AMRO Bank any time, if necessary. Just go through the needed develop to down load or printing the file format.

Use US Legal Forms, by far the most substantial variety of lawful kinds, in order to save efforts and stay away from mistakes. The service delivers professionally produced lawful file layouts which can be used for a range of uses. Generate a merchant account on US Legal Forms and start creating your lifestyle easier.