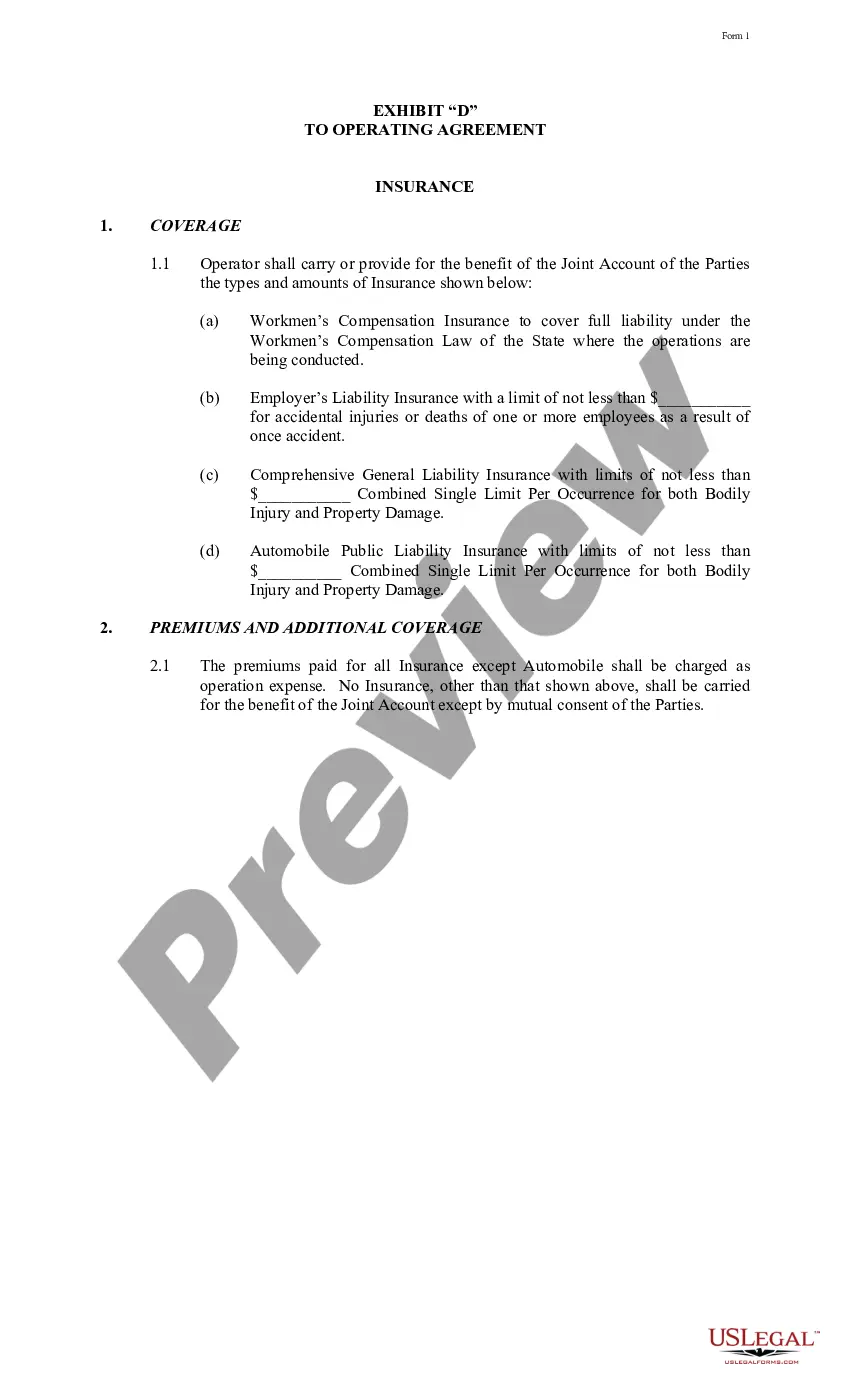

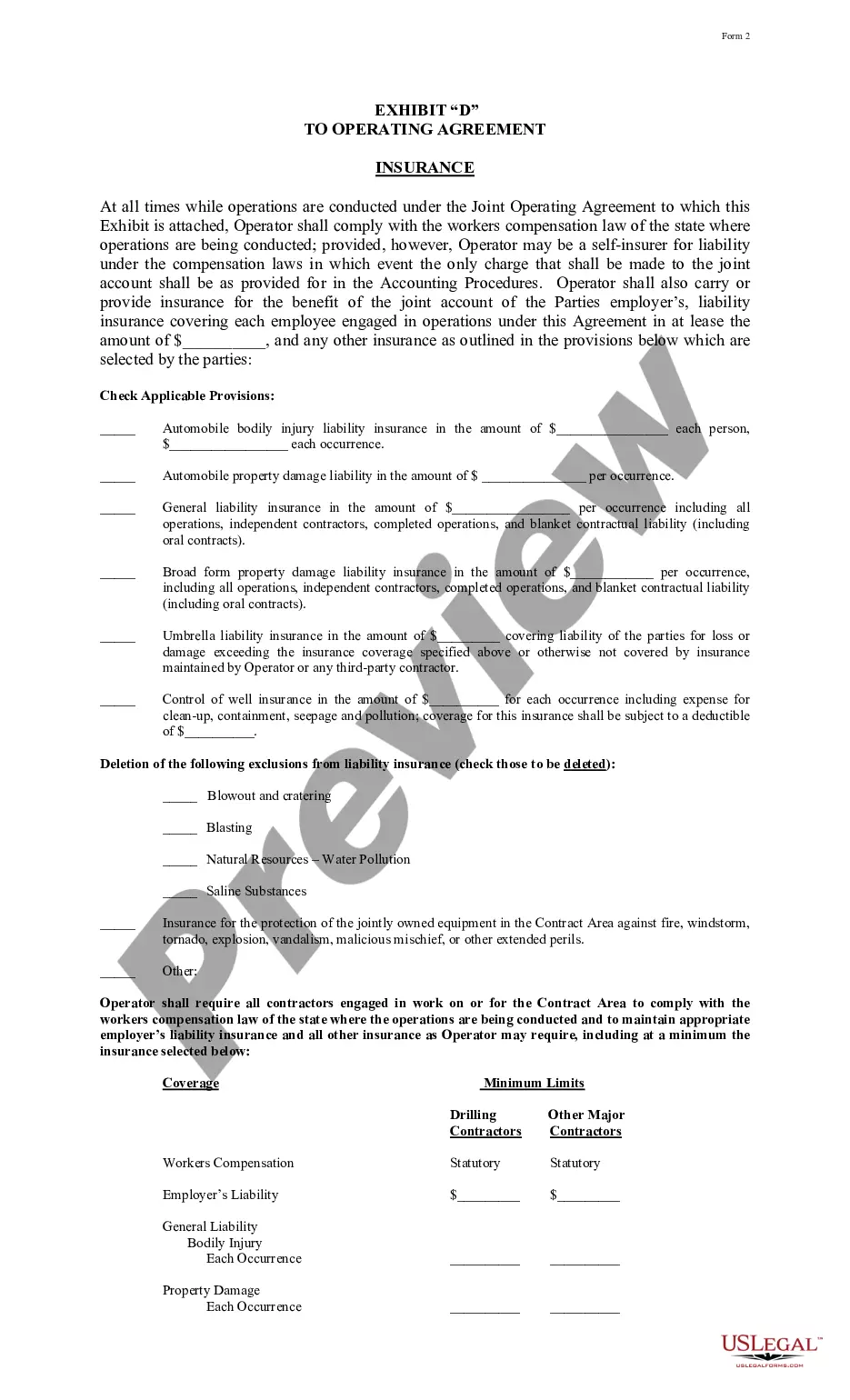

Illinois Exhibit C Accounting Procedure Joint Operations

Description

How to fill out Exhibit C Accounting Procedure Joint Operations?

Choosing the right legal document template could be a struggle. Naturally, there are plenty of themes accessible on the Internet, but how can you obtain the legal type you need? Utilize the US Legal Forms site. The assistance delivers 1000s of themes, including the Illinois Exhibit C Accounting Procedure Joint Operations, that you can use for company and private demands. Each of the varieties are inspected by professionals and fulfill state and federal specifications.

If you are presently listed, log in for your profile and click the Acquire button to obtain the Illinois Exhibit C Accounting Procedure Joint Operations. Make use of your profile to look through the legal varieties you possess bought earlier. Proceed to the My Forms tab of your respective profile and have an additional version from the document you need.

If you are a new user of US Legal Forms, listed here are easy instructions for you to comply with:

- Initially, make sure you have chosen the proper type for your area/county. You are able to look over the shape utilizing the Preview button and study the shape information to make certain this is the right one for you.

- In the event the type fails to fulfill your needs, take advantage of the Seach discipline to get the appropriate type.

- Once you are sure that the shape is suitable, select the Buy now button to obtain the type.

- Select the pricing plan you need and type in the required info. Design your profile and pay money for your order with your PayPal profile or Visa or Mastercard.

- Opt for the document file format and acquire the legal document template for your gadget.

- Full, edit and produce and indicator the acquired Illinois Exhibit C Accounting Procedure Joint Operations.

US Legal Forms is definitely the most significant collection of legal varieties in which you can find various document themes. Utilize the service to acquire expertly-created documents that comply with state specifications.

Form popularity

FAQ

IFRS 11 requires an investor to account for its investments in joint ventures using the equity method (with some limited exceptions). IAS 28 prescribes how to apply the equity method when accounting for investments in associates and joint ventures.

Under the equity method, on initial recognition the investment in an associate or a joint venture is recognised at cost, and the carrying amount is increased or decreased to recognise the investor's share of the profit or loss of the investee after the date of acquisition.

Joint Ventures: Accounting Methodology Under this method, the investor includes the profits of the investee as a single line in its income statement, reflecting the investor's share of the investee's net income. The investor also shows dividends received from the investee as a single line in its cash flow statement.

A joint venture is a joint arrangement whereby the parties that have joint control of the arrangement have rights to the net assets of the arrangement. Those parties are called joint venturers. [IFRS ]

Joint venture accounting involves sharing of financial data relevant to enterprises that are engaged in a joint venture. Gain full visibility into capital and operating expenses using joint-venture software from SAP. Joint Venture Accounting (S/4) - SAP Industry Solution Portfolio net.sap ? industry ? OIL ? object net.sap ? industry ? OIL ? object

IFRS 11 requires an investor to account for its investments in joint ventures using the equity method (with some limited exceptions). IAS 28 prescribes how to apply the equity method when accounting for investments in associates and joint ventures. IAS 28 Investments in Associates and Joint Ventures - IFRS Foundation ifrs.org ? issued-standards ? list-of-standards ifrs.org ? issued-standards ? list-of-standards