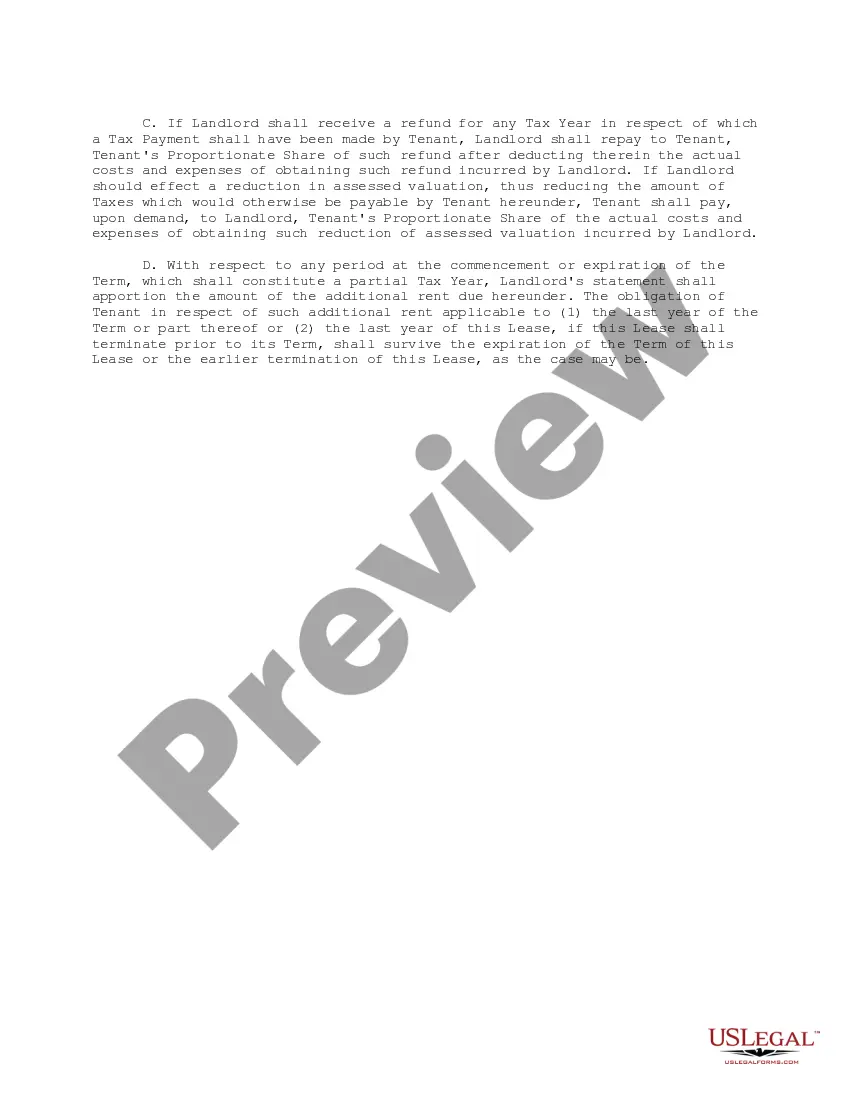

This form is a clause regarding additional rent element of an office lease providing for tax increases. The tax increases pertain to assessments and special assessments levied, assessed or imposed upon the building and/or the land under, including any land(s) dedicated to the use of, the building, by any governmental bodies or authorities.

The Illinois Tax Increase Clause is a constitutional provision that plays a crucial role in the state's financial management. This clause is often referred to as the "Taxpayer Protection Amendment" and was enacted in 1970 as a means to ensure fiscal responsibility and stability in Illinois. The primary objective of the Tax Increase Clause is to protect taxpayers from excessive tax burdens imposed by the government. It stipulates that any tax rate increase must be approved by a three-fifths majority vote in both the Illinois House of Representatives and the Senate, or through a statewide referendum, before it can be implemented. This requirement acts as a safeguard against hasty and unwarranted tax hikes, forcing lawmakers to carefully consider the necessity and impact of any proposed tax increase. This constitutional provision is instrumental in maintaining a balanced budget in Illinois, preventing over-reliance on taxing citizens and businesses. It encourages elected officials to explore alternative revenue sources or implement spending cuts before resorting to increasing taxes. By requiring a super majority support, the Tax Increase Clause ensures that tax policies are thoroughly debated and encourages bipartisan cooperation in Illinois' legislative process. In addition to the overarching Tax Increase Clause, there are several subcategories or considerations within Illinois' tax framework. These include: 1. Income tax increase: Pertains to any proposed changes to the state's income tax rate, necessitating a three-fifths majority vote in the Illinois General Assembly or through a statewide referendum. 2. Sales tax increase: Applies to any proposed alterations to the sales tax rate, requiring three-fifths majority approval in the Illinois House and Senate or via a referendum. 3. Property tax increase: Refers to changes in property tax rates, which must be approved by a three-fifths majority vote in the General Assembly or through a local voter referendum. 4. Fuel tax increase: Deals with proposed adjustments to fuel tax rates, necessitating a three-fifths majority approval in the Illinois Legislature or through a popular vote. 5. Estate tax increase: Relates to any proposed modifications to the state's estate tax, which must be endorsed by a three-fifths majority vote in the General Assembly or via a referendum. Overall, the Illinois Tax Increase Clause serves as a critical tool to ensure responsible fiscal policy and protect taxpayers' interests. It promotes transparency, accountability, and encourages thoughtful decision-making when implementing tax adjustments, fostering a more stable and balanced financial environment for the state.The Illinois Tax Increase Clause is a constitutional provision that plays a crucial role in the state's financial management. This clause is often referred to as the "Taxpayer Protection Amendment" and was enacted in 1970 as a means to ensure fiscal responsibility and stability in Illinois. The primary objective of the Tax Increase Clause is to protect taxpayers from excessive tax burdens imposed by the government. It stipulates that any tax rate increase must be approved by a three-fifths majority vote in both the Illinois House of Representatives and the Senate, or through a statewide referendum, before it can be implemented. This requirement acts as a safeguard against hasty and unwarranted tax hikes, forcing lawmakers to carefully consider the necessity and impact of any proposed tax increase. This constitutional provision is instrumental in maintaining a balanced budget in Illinois, preventing over-reliance on taxing citizens and businesses. It encourages elected officials to explore alternative revenue sources or implement spending cuts before resorting to increasing taxes. By requiring a super majority support, the Tax Increase Clause ensures that tax policies are thoroughly debated and encourages bipartisan cooperation in Illinois' legislative process. In addition to the overarching Tax Increase Clause, there are several subcategories or considerations within Illinois' tax framework. These include: 1. Income tax increase: Pertains to any proposed changes to the state's income tax rate, necessitating a three-fifths majority vote in the Illinois General Assembly or through a statewide referendum. 2. Sales tax increase: Applies to any proposed alterations to the sales tax rate, requiring three-fifths majority approval in the Illinois House and Senate or via a referendum. 3. Property tax increase: Refers to changes in property tax rates, which must be approved by a three-fifths majority vote in the General Assembly or through a local voter referendum. 4. Fuel tax increase: Deals with proposed adjustments to fuel tax rates, necessitating a three-fifths majority approval in the Illinois Legislature or through a popular vote. 5. Estate tax increase: Relates to any proposed modifications to the state's estate tax, which must be endorsed by a three-fifths majority vote in the General Assembly or via a referendum. Overall, the Illinois Tax Increase Clause serves as a critical tool to ensure responsible fiscal policy and protect taxpayers' interests. It promotes transparency, accountability, and encourages thoughtful decision-making when implementing tax adjustments, fostering a more stable and balanced financial environment for the state.