Illinois Assignment of Life Insurance as Collateral

Description

How to fill out Assignment Of Life Insurance As Collateral?

If you wish to complete, down load, or printing legitimate document web templates, use US Legal Forms, the largest variety of legitimate forms, which can be found online. Use the site`s easy and convenient search to obtain the documents you will need. Various web templates for organization and individual reasons are sorted by groups and says, or keywords. Use US Legal Forms to obtain the Illinois Assignment of Life Insurance as Collateral in a number of clicks.

Should you be already a US Legal Forms buyer, log in to the account and click the Acquire button to obtain the Illinois Assignment of Life Insurance as Collateral. You can also accessibility forms you earlier delivered electronically from the My Forms tab of your respective account.

If you use US Legal Forms for the first time, follow the instructions below:

- Step 1. Be sure you have selected the shape for your correct area/land.

- Step 2. Use the Review method to check out the form`s information. Don`t forget to read through the description.

- Step 3. Should you be not happy together with the kind, use the Research discipline towards the top of the monitor to find other variations of the legitimate kind template.

- Step 4. Upon having discovered the shape you will need, click the Acquire now button. Select the prices prepare you favor and add your credentials to sign up for an account.

- Step 5. Procedure the financial transaction. You can utilize your credit card or PayPal account to finish the financial transaction.

- Step 6. Pick the format of the legitimate kind and down load it in your system.

- Step 7. Total, change and printing or indication the Illinois Assignment of Life Insurance as Collateral.

Every legitimate document template you get is your own for a long time. You possess acces to each and every kind you delivered electronically inside your acccount. Click the My Forms segment and choose a kind to printing or down load again.

Compete and down load, and printing the Illinois Assignment of Life Insurance as Collateral with US Legal Forms. There are millions of skilled and status-specific forms you may use for the organization or individual needs.

Form popularity

FAQ

The good news is that in Illinois, generally, the creditors of the deceased person have no rights against the money paid out by a life insurance policy to the beneficiaries.

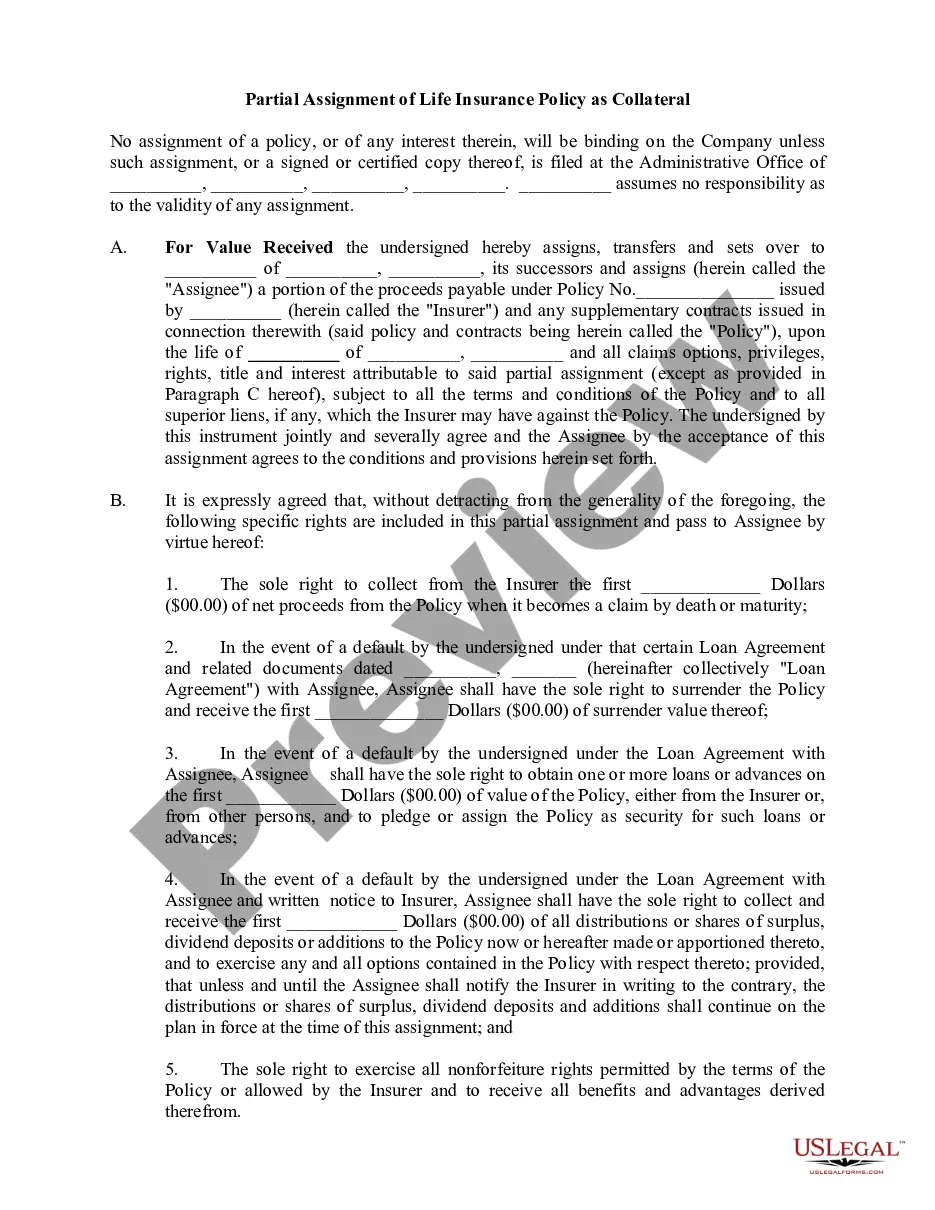

A life insurance policy can be assigned when rights of one person are transferred to another. The rights to your insurance policy can be transferred to someone else for various reasons. The process is known as assignment. An ?assignor? (policyholder) is the person who assigns the insurance policy.

The owner of a Life policy may pledge the policy as collateral for a loan from a bank, who would then have a temporary lien against the policy. If the insured dies during the term of the loan, the insurer will pay off the bank. Any remaining proceeds are payable to the designated beneficiary.

If you have a life insurance policy, you're in luck, because most businesses typically accept life insurance as collateral as they can guarantee funds if the borrower dies or defaults.

Any type of life insurance policy is acceptable for collateral assignment, provided the insurance company allows assignment for the policy. Some banks may require an escrow account for the life insurance premiums, others may require proof of premiums paid or prepaid.

You can use either term or whole life insurance policy as collateral, but the death benefit must meet the lender's terms. Alternately, the policy owner's access to the cash value is restricted to protect the collateral.