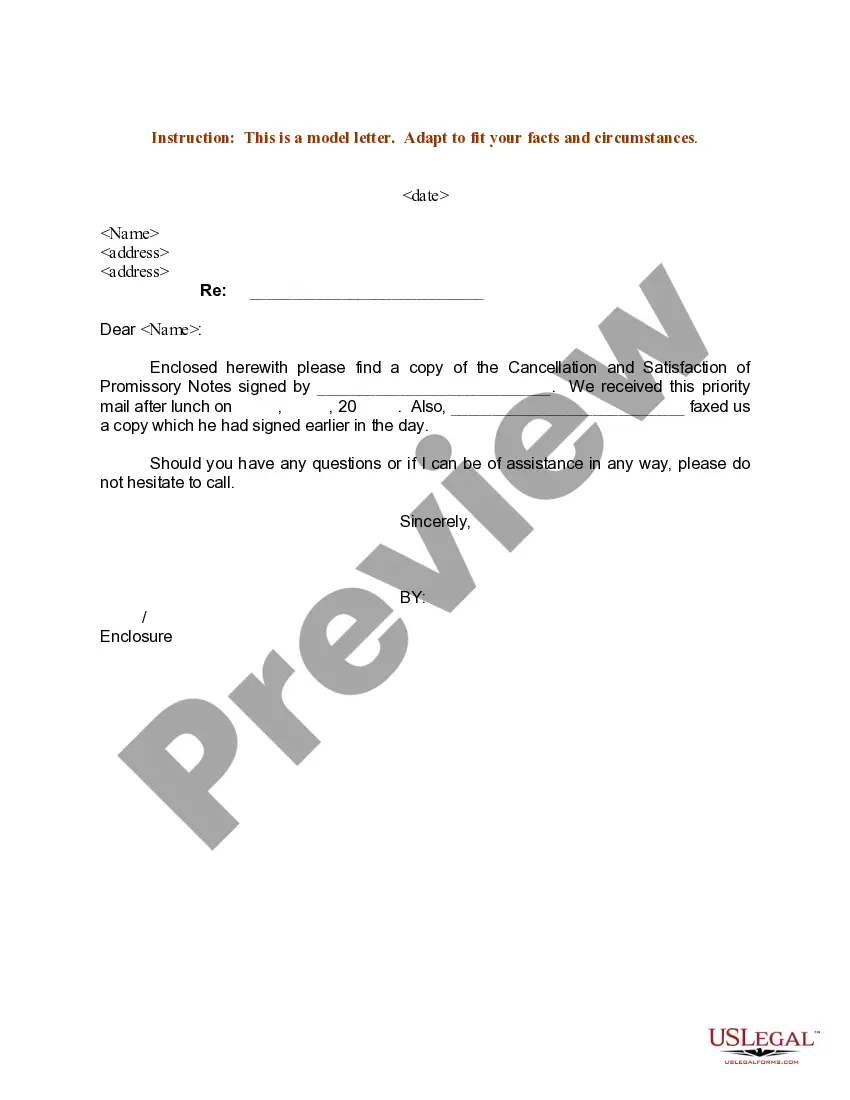

This form is a Promissory Note. The form provides notification that the lender has issued a satisfaction and release to the borrower. All claims against the borrower and his/her heirs have been permanently discharged.

Indiana Promissory Note - Satisfaction and Release

Category:

State:

Multi-State

Control #:

US-00600

Format:

Word;

Rich Text

Instant download

Description

How to fill out Promissory Note - Satisfaction And Release?

US Legal Forms - one of the largest collections of legal templates in the United States - offers a selection of legal document formats that you can download or print.

By utilizing the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the most recent versions of documents such as the Indiana Promissory Note - Satisfaction and Release in mere seconds.

If you already have a monthly subscription, Log In and download the Indiana Promissory Note - Satisfaction and Release from the US Legal Forms library. The Download button will appear on every form you view. You have access to all previously downloaded forms within the My documents section of your account.

Complete the transaction. Use your Visa or Mastercard or PayPal account to finalize the transaction.

Select the format and download the form to your device. Make edits. Fill out, modify, print, and sign the downloaded Indiana Promissory Note - Satisfaction and Release. Every form you added to your account does not expire and is yours permanently. Therefore, if you wish to download or print another copy, simply go to the My documents section and click on the form you need. Gain access to the Indiana Promissory Note - Satisfaction and Release with US Legal Forms, one of the most extensive collections of legal document formats. Utilize thousands of professional and state-specific templates that fulfill your business or personal needs and requirements.

- Ensure you have chosen the correct form for your city/region.

- Click on the Review button to review the content of the form.

- Read the form description to confirm that you have selected the appropriate form.

- If the form does not suit your requirements, utilize the Search area located at the top of the screen to find the one that fits.

- Once satisfied with the form, validate your selection by clicking the Get now button.

- Then, choose the payment plan you prefer and provide your credentials to register for an account.

Form popularity

FAQ

Releasing an Indiana promissory note involves creating a formal satisfaction and release document once you have received full payment. This document should state that all obligations have been met and confirm the lender's acceptance of payment. Both parties should sign this release to retain a record of the closure. Utilizing platforms like uslegalforms can streamline this process, making it easy to generate the necessary documents.

Yes, an Indiana promissory note is a legally binding document, provided it meets specific requirements. When signed by both parties, it serves as proof of the debt and outlines repayment terms. If either party fails to uphold their responsibilities, the other party may seek legal enforcement. Understanding this importance can help you navigate your financial agreements more effectively.

Filling out an Indiana promissory demand note involves clearly stating the borrower's information, the amount borrowed, and the repayment terms. Ensure that the note specifies that it is payable on demand, meaning the lender can request payment at any time. Both parties should sign and date the document, which solidifies the agreement. For assistance, using platforms like uslegalforms can simplify the process and offer templates to guide you.

To terminate an Indiana promissory note, both parties should agree to the termination and document this decision in writing. Typically, you would create a satisfaction and release document that acknowledges the completion of repayment. This document should be signed by both the lender and borrower, ensuring both parties have a copy. By properly documenting this, you confirm that the obligation under the Indiana promissory note has been fulfilled.

Satisfaction and general release of a promissory note refer to the formal closure of the debt obligation. When a borrower fulfills their payment duties, a satisfaction document can be created to indicate that the debt is settled. This declaration protects both parties by clearly stating that the borrower has met their obligations related to the Indiana Promissory Note. It's essential to maintain this documentation for future reference.

To obtain your Indiana Promissory Note, start by visiting a reliable resource like US Legal Forms. They offer a variety of templates and guides tailored to your needs. Simply select the appropriate form, fill it out, and follow the instructions to ensure you comply with state requirements. This process ensures you receive a valid and enforceable document.

In Indiana, the statute of limitations for enforcing a promissory note is generally six years. This period begins from the date the note becomes due. Understanding this timeline is important for both lenders and borrowers when considering the Indiana Promissory Note - Satisfaction and Release.

The release and satisfaction of a promissory note confirm that the borrower has repaid the debt in full. Once satisfied, the lender issues a document that clears the borrower from any future obligations. This step is essential in the context of the Indiana Promissory Note - Satisfaction and Release.

To release a promissory note, the lender must provide written confirmation that the debt has been satisfied. This usually involves issuing a release or satisfaction document after payment has been made. By following this process, you can ensure compliance with the Indiana Promissory Note - Satisfaction and Release requirements.

Cancellation and release indicate that a promissory note has been deemed void and no longer holds value. This occurs when the debt is fully satisfied or if an agreement is made to cancel the note. A formal Indiana Promissory Note - Satisfaction and Release ensures that both parties acknowledge the completion of the agreement.