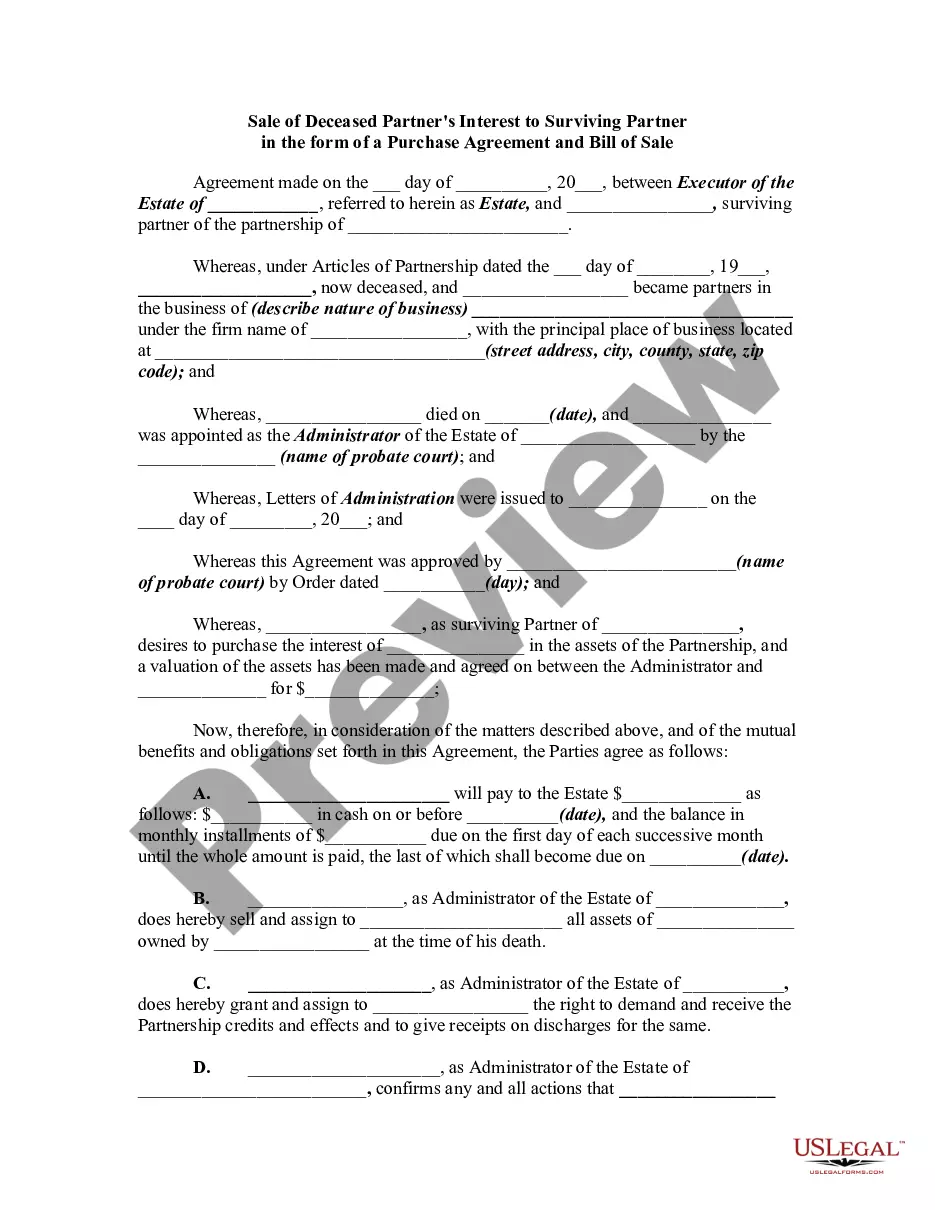

Title: Indiana Sale of Deceased Partner's Interest to Surviving Partner: Purchase Agreement and Bill of Sale Introduction: In the state of Indiana, when a partner passes away in a partnership, it becomes necessary for the surviving partner(s) to acquire the deceased partner's interest. This transaction is commonly facilitated through a Purchase Agreement and Bill of Sale, which outlines the terms and conditions of the transfer. This article will delve into the intricacies of the Indiana Sale of Deceased Partner's Interest to Surviving Partner and shed light on any variations that may exist within this process. Key Points: 1. Purchase Agreement: — A Purchase Agreement is a legally binding contract that outlines the terms of the sale between the surviving partner(s) and the estate of the deceased partner. It defines the purchase price, payment terms, closing date, and other pertinent details. — The agreement should include a clear identification of the parties involved, specifying the surviving partner(s) and the representative(s) of the estate. — It should state the specific interest being transferred, including the percentage or share of ownership the deceased partner held in the partnership. 2. Bill of Sale: — A Bill of Sale is a document that formalizes the transfer of ownership from the estate of the deceased partner to the surviving partner(s). — It should include a detailed description of the assets or property being transferred, such as the partnership interest and any accompanying rights or benefits. — The Bill of Sale must be signed, dated, and notarized by both parties to affirm its validity and to ensure a smooth transfer of the deceased partner's interest. 3. Key Terms in the Purchase Agreement: — Purchase Price: State the agreed-upon amount that the surviving partner(s) will pay the estate for the deceased partner's interest. — Payment Terms: Establish the payment method, whether it is a lump sum or installment payments, and specify any interest or late fees. — Closing Date: Determine the date on which the transaction will be finalized, and ensure both parties have fulfilled their obligations by that time. — Representations and Warranties: Include provisions wherein the estate warrants that they possess the full right to transfer the interest and that there are no undisclosed liabilities or claims. Types of Indiana Sale of Deceased Partner's Interest to Surviving Partner: 1. Voluntary Sale: In cases where both partners have previously agreed to a buyout arrangement, the surviving partner can negotiate the terms with the estate's representative or executor. 2. Forced Sale: In situations where there is no prior agreement, Indiana law permits the surviving partner(s) to make a fair market value offer to the estate for the deceased partner's interest. If the parties fail to reach a mutual agreement, a court-appointed appraiser may determine the sale price. Conclusion: The Indiana Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale is a crucial step in preserving and continuing the partnership. Understanding the process and incorporating these documents helps ensure a fair and legal transfer of the deceased partner's interest. Whether a voluntary or forced sale, the Purchase Agreement and Bill of Sale must be accurately executed to secure a smooth transition of ownership.

Indiana Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale

Description

How to fill out Indiana Sale Of Deceased Partner's Interest To Surviving Partner In The Form Of A Purchase Agreement And Bill Of Sale?

US Legal Forms - one of many most significant libraries of authorized types in America - gives a wide array of authorized file web templates it is possible to obtain or produce. While using site, you can get a large number of types for enterprise and person functions, categorized by types, claims, or search phrases.You will discover the latest types of types such as the Indiana Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale within minutes.

If you have a subscription, log in and obtain Indiana Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale from the US Legal Forms library. The Down load button will show up on every single develop you view. You gain access to all previously delivered electronically types in the My Forms tab of your own account.

In order to use US Legal Forms the very first time, listed here are straightforward guidelines to obtain began:

- Make sure you have chosen the proper develop for your personal city/state. Click on the Review button to check the form`s information. See the develop description to ensure that you have chosen the right develop.

- In the event the develop doesn`t match your requirements, utilize the Research discipline towards the top of the monitor to find the one which does.

- When you are pleased with the shape, verify your option by clicking on the Purchase now button. Then, select the costs prepare you prefer and supply your qualifications to register for the account.

- Process the financial transaction. Make use of your charge card or PayPal account to perform the financial transaction.

- Find the formatting and obtain the shape on your own device.

- Make changes. Fill out, change and produce and indication the delivered electronically Indiana Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale.

Each template you included in your account does not have an expiration particular date which is yours for a long time. So, if you want to obtain or produce an additional version, just check out the My Forms area and click on around the develop you want.

Get access to the Indiana Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale with US Legal Forms, by far the most comprehensive library of authorized file web templates. Use a large number of professional and status-particular web templates that fulfill your organization or person requires and requirements.