Dissolution is the act of bringing to an end. It is the act of rendering a legal proceeding null, or changing its character. Under corporate law, it is the last stage of liquidation. Dissolution is the process by which a company is brought to an end.

Liquidation is the selling of the assets of a business, paying bills and dividing the remainder among shareholders, partners or other investors. A business need not be insolvent to liquidate. Upon liquidation of certain business, such as a bank, a bond may be required to be posted to assure the proper distribution of assets to creditors.

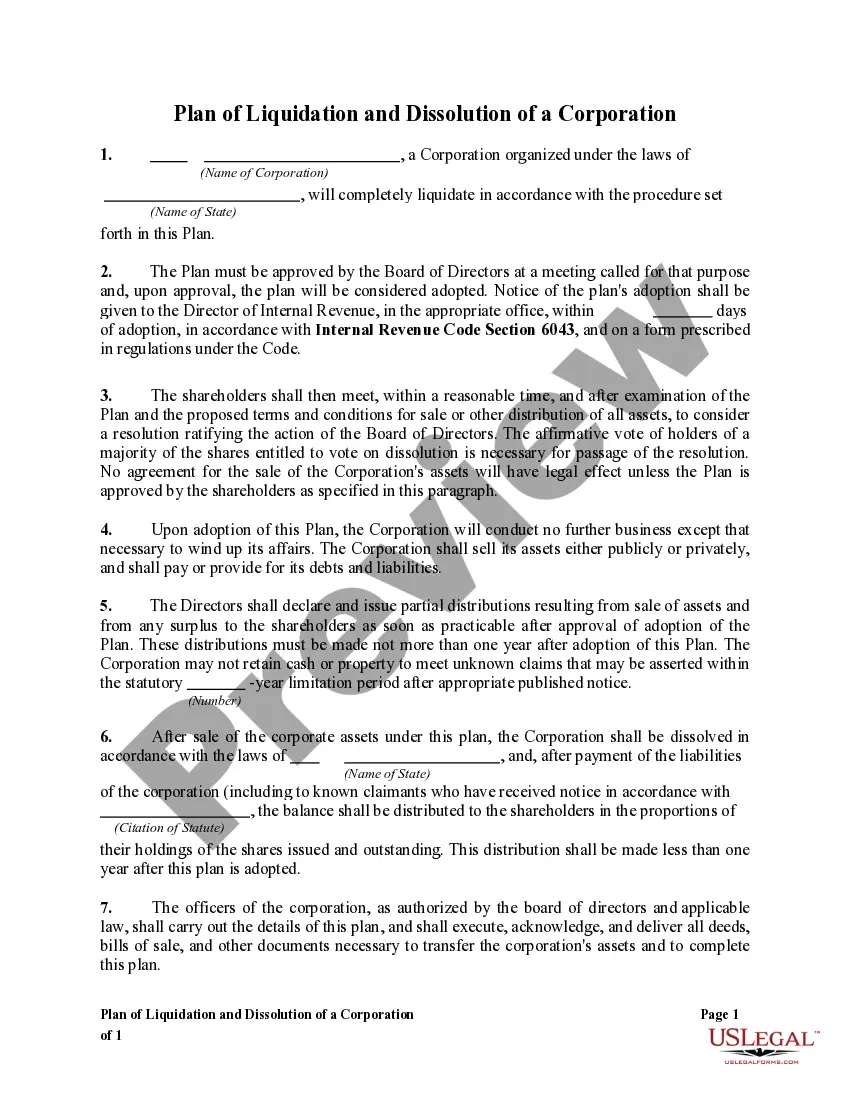

The Indiana Plan of Liquidation and Dissolution of a Corporation is a legal process through which a corporation based in Indiana can wind up its affairs and cease its ongoing operations. This plan outlines the steps that need to be taken to liquidate the corporation's assets, settle its debts, and distribute the remaining funds or assets among its shareholders. The Indiana Plan of Liquidation and Dissolution of a Corporation involves several key components. Firstly, the corporation's board of directors must adopt a resolution proposing the plan, specifying the reasons for dissolution, and directing the submission of the plan to the shareholders for their approval. After this, the plan must be approved by the shareholders, typically through a majority vote, unless the articles of incorporation require a higher threshold. Once the plan has been approved, the corporation initiates the liquidation process, which involves winding up its affairs in an orderly manner. This includes settling any outstanding debts, paying off creditors, and selling off the corporation's assets. The liquidation process may be overseen by a liquidating trustee appointed by the board of directors to ensure the proper execution of the plan. It is important to note that there are various types of Indiana Plans of Liquidation and Dissolution of a Corporation, each with its own specific timeframe and considerations. These may include: 1. Voluntary Dissolution: This occurs when the corporation decides to dissolve voluntarily, either due to its inability to sustain operations or as a result of the shareholders' decision to cease business activities. 2. Involuntary Dissolution: In cases where the corporation fails to comply with certain legal requirements, such as paying taxes or filing annual reports, the state may initiate involuntary dissolution proceedings, forcing the corporation to liquidate and dissolve. 3. Dissolution Pursuant to Court Order: If a court determines that it is in the best interest of the corporation or its shareholders, it may order the dissolution and appointment of a liquidating trustee to oversee the process. 4. Dissolution by Short-Form Procedure: A corporation that meets certain eligibility criteria, such as having no liabilities or obligations and the written consent of all shareholders, may dissolve using a simplified short-form procedure. In conclusion, the Indiana Plan of Liquidation and Dissolution of a Corporation is a legal framework that enables a corporation in Indiana to wind up its affairs, settle its debts, and distribute remaining assets to shareholders. Understanding the different types of dissolution processes available can help corporations navigate the complexities of liquidation and dissolution in accordance with Indiana state laws.The Indiana Plan of Liquidation and Dissolution of a Corporation is a legal process through which a corporation based in Indiana can wind up its affairs and cease its ongoing operations. This plan outlines the steps that need to be taken to liquidate the corporation's assets, settle its debts, and distribute the remaining funds or assets among its shareholders. The Indiana Plan of Liquidation and Dissolution of a Corporation involves several key components. Firstly, the corporation's board of directors must adopt a resolution proposing the plan, specifying the reasons for dissolution, and directing the submission of the plan to the shareholders for their approval. After this, the plan must be approved by the shareholders, typically through a majority vote, unless the articles of incorporation require a higher threshold. Once the plan has been approved, the corporation initiates the liquidation process, which involves winding up its affairs in an orderly manner. This includes settling any outstanding debts, paying off creditors, and selling off the corporation's assets. The liquidation process may be overseen by a liquidating trustee appointed by the board of directors to ensure the proper execution of the plan. It is important to note that there are various types of Indiana Plans of Liquidation and Dissolution of a Corporation, each with its own specific timeframe and considerations. These may include: 1. Voluntary Dissolution: This occurs when the corporation decides to dissolve voluntarily, either due to its inability to sustain operations or as a result of the shareholders' decision to cease business activities. 2. Involuntary Dissolution: In cases where the corporation fails to comply with certain legal requirements, such as paying taxes or filing annual reports, the state may initiate involuntary dissolution proceedings, forcing the corporation to liquidate and dissolve. 3. Dissolution Pursuant to Court Order: If a court determines that it is in the best interest of the corporation or its shareholders, it may order the dissolution and appointment of a liquidating trustee to oversee the process. 4. Dissolution by Short-Form Procedure: A corporation that meets certain eligibility criteria, such as having no liabilities or obligations and the written consent of all shareholders, may dissolve using a simplified short-form procedure. In conclusion, the Indiana Plan of Liquidation and Dissolution of a Corporation is a legal framework that enables a corporation in Indiana to wind up its affairs, settle its debts, and distribute remaining assets to shareholders. Understanding the different types of dissolution processes available can help corporations navigate the complexities of liquidation and dissolution in accordance with Indiana state laws.