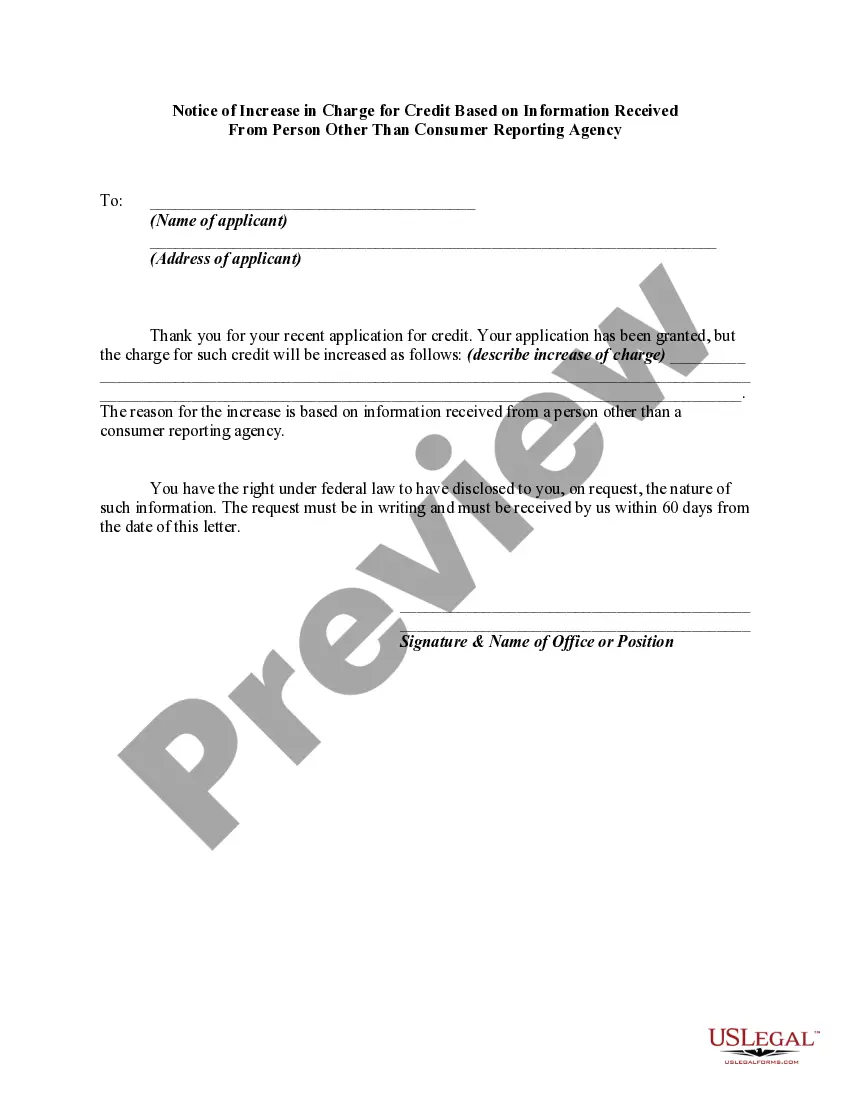

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

Title: Understanding Indiana Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency Introduction: The Indiana Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is an important legal document that outlines the reasons and implications behind a potential increase in charges for credit. This notice serves to inform consumers about changes to their credit terms and conditions based on information obtained from a source other than a consumer reporting agency. Let's delve into the different types and key aspects of this notice. Types of Indiana Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency: 1. General Overview: The notice provides consumers with an overview of the change in credit charges based on the information received from a person other than a consumer reporting agency. It explains the reasons for the increase, how it will affect the consumer's credit account, and any associated fees or penalties. 2. Disclosure of Information Sources: This type of notice clearly discloses the specific source from which the information leading to the credit charge increase was obtained. Examples can include creditors, financial institutions, or other relevant entities. 3. Explanation of Factors Leading to Increase: This notice explains the factors and reasons that contributed to the increase in charges. It may mention negative changes in the consumer's credit history, outstanding debts, or concerns regarding their creditworthiness, among other relevant factors. 4. Disclosure of Alternative Options: In some cases, the notice might outline alternative options for consumers to avoid or minimize the increased charges. These options could include paying off outstanding balances, seeking credit counseling services, or disputing incorrect information provided to the creditor. 5. Notification of Consumer's Right to Obtain Credit Reports: The notice emphasizes the consumer's right to obtain a free copy of their credit report from consumer reporting agencies, to review the accuracy of the information provided by the person other than a consumer reporting agency. It may also provide instructions on how to request the report. Key Components and Relevant Keywords: a. Consumer Reporting Agency: A consumer reporting agency is an entity that collects and provides information about individuals' credit history, such as Equifax, Experian, and TransUnion. b. Credit Charges: This refers to the fees, interest rates, or penalties imposed on a consumer's credit account. c. Credit Terms and Conditions: The specific rules, regulations, and conditions that apply to a consumer's credit account, including interest rates, payment terms, and fees. d. Creditworthiness: A measure of an individual's ability to repay borrowed funds based on their credit history, income, and financial stability. e. Negative Changes in Credit History: Adverse events, such as late payments, defaults, or other negative marks on a consumer's credit record, which may impact their creditworthiness. f. Outstanding Debts: Unsettled balances or amounts owed on a consumer's credit accounts. g. Penalties and Fees: Additional charges imposed on a consumer when certain conditions or terms of their credit agreement are not met. Conclusion: Understanding the Indiana Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is crucial for consumers to make informed financial decisions. It ensures transparency and compliance with consumer protection laws. By familiarizing themselves with this notice, consumers can take appropriate actions to maintain their creditworthiness and manage their credit accounts effectively.Title: Understanding Indiana Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency Introduction: The Indiana Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is an important legal document that outlines the reasons and implications behind a potential increase in charges for credit. This notice serves to inform consumers about changes to their credit terms and conditions based on information obtained from a source other than a consumer reporting agency. Let's delve into the different types and key aspects of this notice. Types of Indiana Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency: 1. General Overview: The notice provides consumers with an overview of the change in credit charges based on the information received from a person other than a consumer reporting agency. It explains the reasons for the increase, how it will affect the consumer's credit account, and any associated fees or penalties. 2. Disclosure of Information Sources: This type of notice clearly discloses the specific source from which the information leading to the credit charge increase was obtained. Examples can include creditors, financial institutions, or other relevant entities. 3. Explanation of Factors Leading to Increase: This notice explains the factors and reasons that contributed to the increase in charges. It may mention negative changes in the consumer's credit history, outstanding debts, or concerns regarding their creditworthiness, among other relevant factors. 4. Disclosure of Alternative Options: In some cases, the notice might outline alternative options for consumers to avoid or minimize the increased charges. These options could include paying off outstanding balances, seeking credit counseling services, or disputing incorrect information provided to the creditor. 5. Notification of Consumer's Right to Obtain Credit Reports: The notice emphasizes the consumer's right to obtain a free copy of their credit report from consumer reporting agencies, to review the accuracy of the information provided by the person other than a consumer reporting agency. It may also provide instructions on how to request the report. Key Components and Relevant Keywords: a. Consumer Reporting Agency: A consumer reporting agency is an entity that collects and provides information about individuals' credit history, such as Equifax, Experian, and TransUnion. b. Credit Charges: This refers to the fees, interest rates, or penalties imposed on a consumer's credit account. c. Credit Terms and Conditions: The specific rules, regulations, and conditions that apply to a consumer's credit account, including interest rates, payment terms, and fees. d. Creditworthiness: A measure of an individual's ability to repay borrowed funds based on their credit history, income, and financial stability. e. Negative Changes in Credit History: Adverse events, such as late payments, defaults, or other negative marks on a consumer's credit record, which may impact their creditworthiness. f. Outstanding Debts: Unsettled balances or amounts owed on a consumer's credit accounts. g. Penalties and Fees: Additional charges imposed on a consumer when certain conditions or terms of their credit agreement are not met. Conclusion: Understanding the Indiana Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is crucial for consumers to make informed financial decisions. It ensures transparency and compliance with consumer protection laws. By familiarizing themselves with this notice, consumers can take appropriate actions to maintain their creditworthiness and manage their credit accounts effectively.