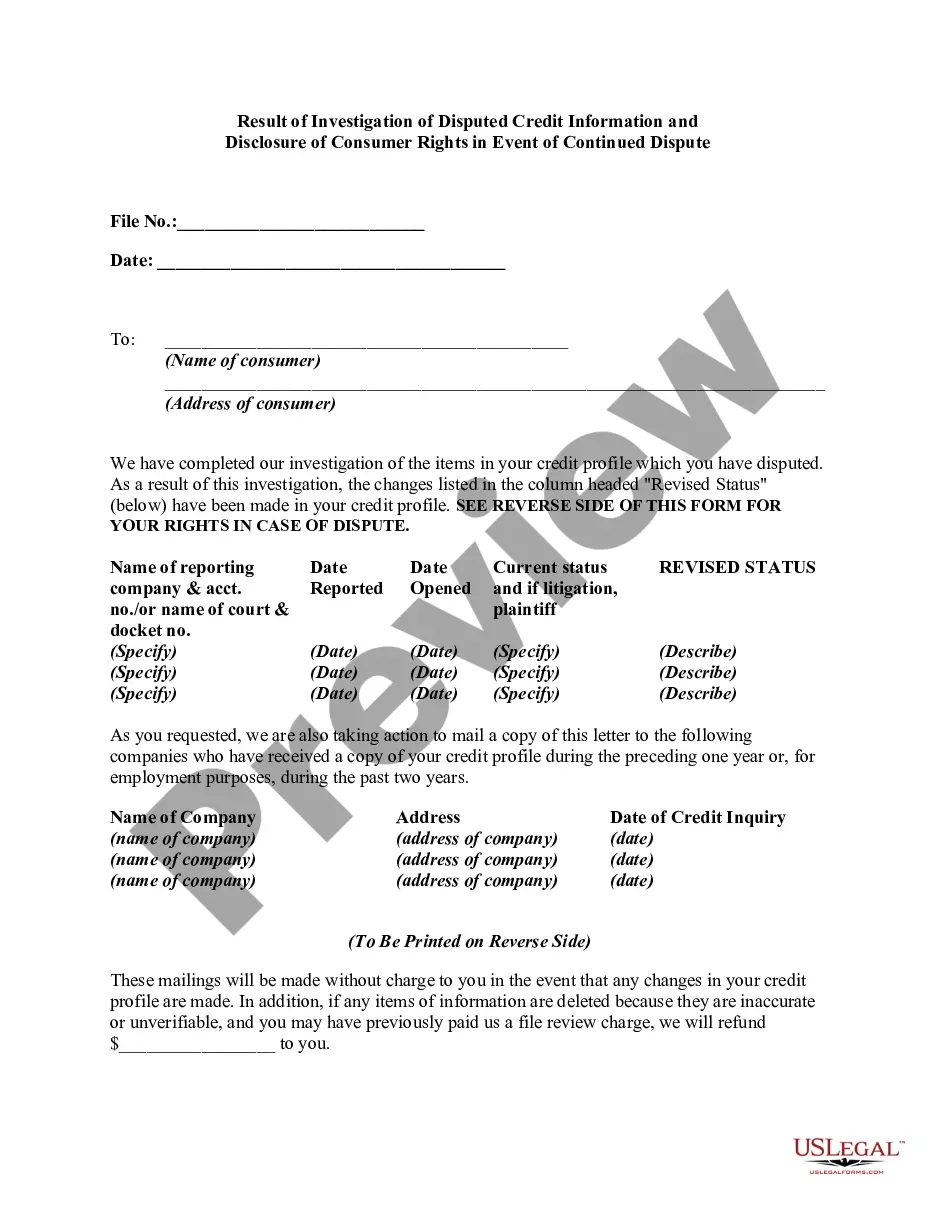

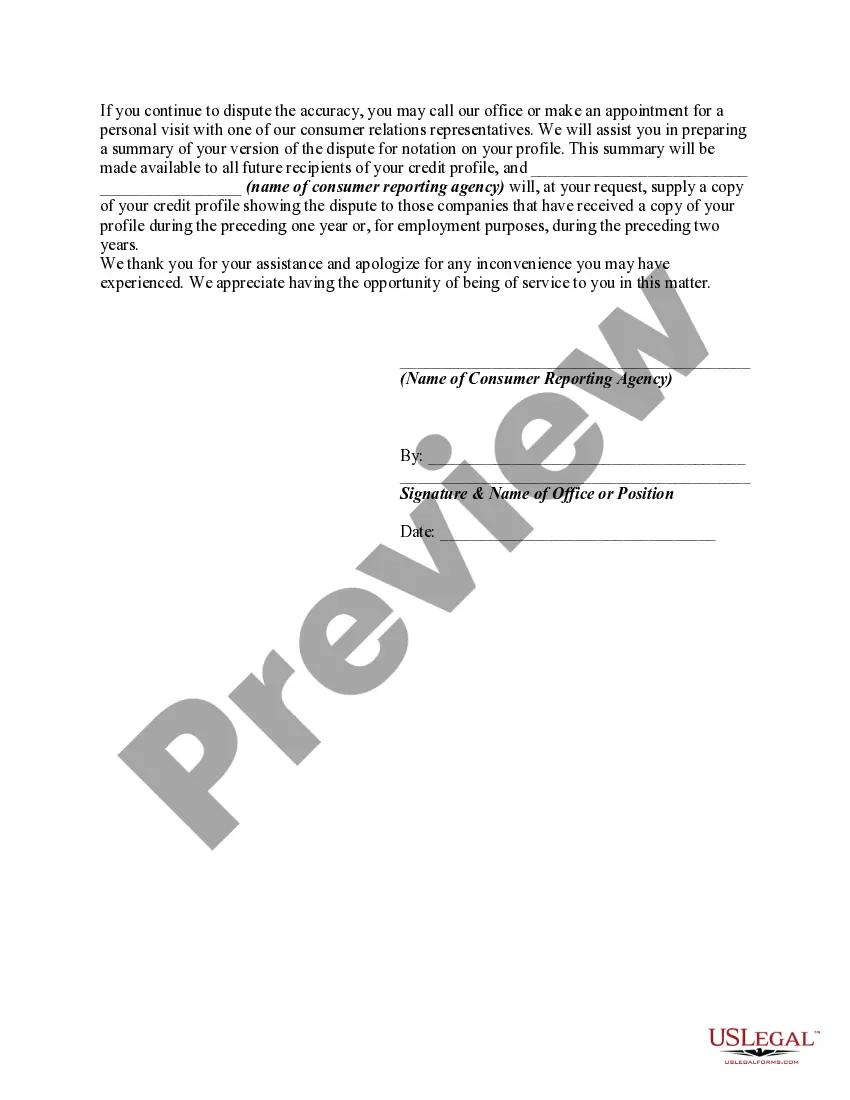

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

Indiana Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute In the state of Indiana, consumers have certain rights regarding disputed credit information and the investigation process. When a consumer disputes inaccurate or incomplete information on their credit report, the credit reporting agencies are obligated to conduct an investigation and provide a result of the investigation within a specific timeframe. It is important for consumers to understand their rights in this process and the potential outcomes. During the investigation process, the credit reporting agencies contact the source of the disputed information, which can be a creditor, lender, or other data provider. The source is required to provide accurate and verifiable information to the credit reporting agency to support their claims. The investigation is conducted with the aim of resolving the dispute and ensuring the accuracy of the consumer's credit report. To ensure transparency and consumer protection, Indiana law requires that the result of the investigation be provided to the consumer in writing. The result of the investigation should include whether the disputed information was verified as accurate, updated, or deleted from the consumer's credit report. It is essential for consumers to carefully review the result of the investigation to understand the actions taken by the credit reporting agencies. In the event that the disputed information is verified as accurate, the consumer has the right to request the inclusion of a statement in their credit file explaining their side of the story. This statement, known as a consumer statement, becomes a part of the consumer's credit report and can be seen by future lenders or creditors. The consumer statement provides an opportunity for the consumer to explain any extenuating circumstances or provide additional context related to the disputed information. If the consumer disagrees with the result of the investigation, Indiana law provides them with the right to further dispute the credit information and continue the investigation process. In such cases, the consumer must provide any additional supporting documentation or evidence to substantiate their claims. The credit reporting agencies are then obligated to conduct a re-investigation and provide the consumer with the updated result within a reasonable timeframe. It is worth noting that consumers may have different types of disputes depending on the nature of the credit information in question. These disputes can range from inaccuracies in personal identification information, such as name or address, to more complex issues related to credit accounts, payment history, or public records. Regardless of the type of dispute, consumers in Indiana have the right to expect a thorough and timely investigation process and a clear disclosure of the result. In conclusion, Indiana law ensures that consumers have certain rights in the result of an investigation related to disputed credit information. Consumers in Indiana have the right to a written disclosure of the investigation result, including whether the disputed information was verified and the actions taken by the credit reporting agencies. If the dispute is not resolved to their satisfaction, consumers have the right to continue the dispute process and provide additional evidence. Understanding these rights can empower consumers in their efforts to maintain accurate and fair credit reports.Indiana Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute In the state of Indiana, consumers have certain rights regarding disputed credit information and the investigation process. When a consumer disputes inaccurate or incomplete information on their credit report, the credit reporting agencies are obligated to conduct an investigation and provide a result of the investigation within a specific timeframe. It is important for consumers to understand their rights in this process and the potential outcomes. During the investigation process, the credit reporting agencies contact the source of the disputed information, which can be a creditor, lender, or other data provider. The source is required to provide accurate and verifiable information to the credit reporting agency to support their claims. The investigation is conducted with the aim of resolving the dispute and ensuring the accuracy of the consumer's credit report. To ensure transparency and consumer protection, Indiana law requires that the result of the investigation be provided to the consumer in writing. The result of the investigation should include whether the disputed information was verified as accurate, updated, or deleted from the consumer's credit report. It is essential for consumers to carefully review the result of the investigation to understand the actions taken by the credit reporting agencies. In the event that the disputed information is verified as accurate, the consumer has the right to request the inclusion of a statement in their credit file explaining their side of the story. This statement, known as a consumer statement, becomes a part of the consumer's credit report and can be seen by future lenders or creditors. The consumer statement provides an opportunity for the consumer to explain any extenuating circumstances or provide additional context related to the disputed information. If the consumer disagrees with the result of the investigation, Indiana law provides them with the right to further dispute the credit information and continue the investigation process. In such cases, the consumer must provide any additional supporting documentation or evidence to substantiate their claims. The credit reporting agencies are then obligated to conduct a re-investigation and provide the consumer with the updated result within a reasonable timeframe. It is worth noting that consumers may have different types of disputes depending on the nature of the credit information in question. These disputes can range from inaccuracies in personal identification information, such as name or address, to more complex issues related to credit accounts, payment history, or public records. Regardless of the type of dispute, consumers in Indiana have the right to expect a thorough and timely investigation process and a clear disclosure of the result. In conclusion, Indiana law ensures that consumers have certain rights in the result of an investigation related to disputed credit information. Consumers in Indiana have the right to a written disclosure of the investigation result, including whether the disputed information was verified and the actions taken by the credit reporting agencies. If the dispute is not resolved to their satisfaction, consumers have the right to continue the dispute process and provide additional evidence. Understanding these rights can empower consumers in their efforts to maintain accurate and fair credit reports.