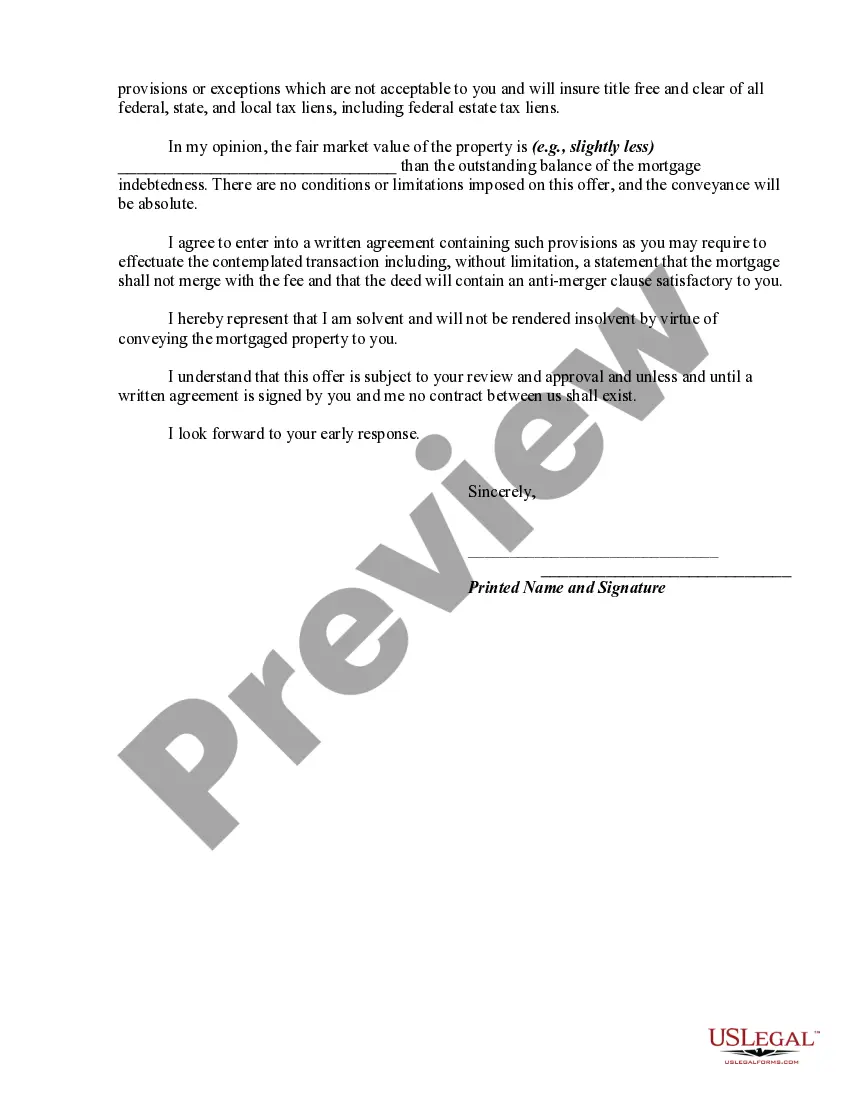

A deed in lieu of foreclosure is a method sometimes used by a lienholder on property to avoid a lengthy and expensive foreclosure process, with a deed in lieu of foreclosure a foreclosing lienholder agrees to have the ownership interest transferred to the bank/lienholder as payment in full. The debtor basically deeds the property to the bank instead of them paying for foreclosure proceedings. Therefore, if a debtor fails to make mortgage payments and the bank is about to foreclose on the property, the deed in lieu of foreclosure is an option that chooses to give the bank ownership of the property rather than having the bank use the legal process of foreclosure.

Title: Indiana Offer by Borrower of Deed in Lieu of Foreclosure: Understanding the Process and Benefits Introduction: In Indiana, a borrower facing foreclosure may consider an Offer by Borrower of Deed in Lieu of Foreclosure as a potential solution to their financial difficulties. This powerful alternative enables the borrower to transfer the property title to the lender, usually a mortgage company or bank, instead of undergoing the traditional foreclosure process. This article aims to provide a detailed description of what this process entails, highlighting the benefits it offers and potential variations in its implementation. Keywords: Indiana, Offer by Borrower of Deed in Lieu of Foreclosure, foreclosure process, borrower, lender, property title, financial difficulties, alternative 1. Understanding the Offer by Borrower of Deed in Lieu of Foreclosure in Indiana: The Offer by Borrower of Deed in Lieu of Foreclosure is a legal agreement in which a borrower voluntarily transfers the property's ownership rights to the lender. It allows the borrower to avoid foreclosure, which can have significant long-term consequences, and instead find a mutually beneficial solution with the lender. 2. Process and Requirements: a. Initiation: The borrower must approach their lender with an official written offer, expressing their intention to transfer the property's title in lieu of foreclosure. This offer should outline the borrower's financial circumstances, the reasons for their inability to continue making loan payments, and a proposal for the deed transfer. b. Lender Assessment: The lender will evaluate the borrower's offer, financial situation, and the property's market value to determine if accepting the deed in lieu is beneficial to them. They may require additional documentation, such as proof of financial hardship, tax records, or property assessment reports. c. Negotiation: If the lender finds the offer suitable, they may initiate negotiations with the borrower to determine the terms and conditions of the deed transfer. These negotiations include discussing potential financial incentives or obligations, such as forgiving a portion of the remaining debt or limiting any liability on the borrower's part. d. Final Agreement: Once both parties agree on the terms, a legally binding agreement is executed, formalizing the transfer of the property's title to the lender, thereby avoiding foreclosure. 3. Benefits of the Offer by Borrower of Deed in Lieu of Foreclosure: a. Avoiding Foreclosure: By proactively transferring the property title to the lender, borrowers can prevent the potentially damaging consequences of a foreclosure on their credit history, saving their future borrowing prospects. b. Speed and Efficiency: Deed in lieu of foreclosure offers a faster and less complex resolution compared to the traditional foreclosure process. The borrower can swiftly transition out of financial distress and alleviate the emotional burden associated with foreclosure. c. Relieve Debt Burden: Depending on negotiations, lenders may absolve the borrower of any remaining mortgage debt or reduce it significantly, offering a fresh start to the borrower's financial situation. d. Maintaining Dignity and Privacy: Unlike the public nature of foreclosure proceedings, this option provides a more private exit strategy, allowing borrowers to minimize public exposure and maintain their dignity throughout the process. Types of Indiana Offer by Borrower of Deed in Lieu of Foreclosure: While the process of Offer by Borrower of Deed in Lieu of Foreclosure generally follows the described steps, variations may exist in terms negotiated between the parties. These variations could include the specifics of debt reduction, financial incentives, or conditions associated with any remaining debt liability. Conclusion: The Offer by Borrower of Deed in Lieu of Foreclosure in Indiana provides borrowers with an opportunity to avoid the detrimental effects of foreclosure, offering a mutually beneficial solution for both parties involved. By understanding the process and its advantages, homeowners facing financial hardship can make informed decisions and work towards a more stable financial future.Title: Indiana Offer by Borrower of Deed in Lieu of Foreclosure: Understanding the Process and Benefits Introduction: In Indiana, a borrower facing foreclosure may consider an Offer by Borrower of Deed in Lieu of Foreclosure as a potential solution to their financial difficulties. This powerful alternative enables the borrower to transfer the property title to the lender, usually a mortgage company or bank, instead of undergoing the traditional foreclosure process. This article aims to provide a detailed description of what this process entails, highlighting the benefits it offers and potential variations in its implementation. Keywords: Indiana, Offer by Borrower of Deed in Lieu of Foreclosure, foreclosure process, borrower, lender, property title, financial difficulties, alternative 1. Understanding the Offer by Borrower of Deed in Lieu of Foreclosure in Indiana: The Offer by Borrower of Deed in Lieu of Foreclosure is a legal agreement in which a borrower voluntarily transfers the property's ownership rights to the lender. It allows the borrower to avoid foreclosure, which can have significant long-term consequences, and instead find a mutually beneficial solution with the lender. 2. Process and Requirements: a. Initiation: The borrower must approach their lender with an official written offer, expressing their intention to transfer the property's title in lieu of foreclosure. This offer should outline the borrower's financial circumstances, the reasons for their inability to continue making loan payments, and a proposal for the deed transfer. b. Lender Assessment: The lender will evaluate the borrower's offer, financial situation, and the property's market value to determine if accepting the deed in lieu is beneficial to them. They may require additional documentation, such as proof of financial hardship, tax records, or property assessment reports. c. Negotiation: If the lender finds the offer suitable, they may initiate negotiations with the borrower to determine the terms and conditions of the deed transfer. These negotiations include discussing potential financial incentives or obligations, such as forgiving a portion of the remaining debt or limiting any liability on the borrower's part. d. Final Agreement: Once both parties agree on the terms, a legally binding agreement is executed, formalizing the transfer of the property's title to the lender, thereby avoiding foreclosure. 3. Benefits of the Offer by Borrower of Deed in Lieu of Foreclosure: a. Avoiding Foreclosure: By proactively transferring the property title to the lender, borrowers can prevent the potentially damaging consequences of a foreclosure on their credit history, saving their future borrowing prospects. b. Speed and Efficiency: Deed in lieu of foreclosure offers a faster and less complex resolution compared to the traditional foreclosure process. The borrower can swiftly transition out of financial distress and alleviate the emotional burden associated with foreclosure. c. Relieve Debt Burden: Depending on negotiations, lenders may absolve the borrower of any remaining mortgage debt or reduce it significantly, offering a fresh start to the borrower's financial situation. d. Maintaining Dignity and Privacy: Unlike the public nature of foreclosure proceedings, this option provides a more private exit strategy, allowing borrowers to minimize public exposure and maintain their dignity throughout the process. Types of Indiana Offer by Borrower of Deed in Lieu of Foreclosure: While the process of Offer by Borrower of Deed in Lieu of Foreclosure generally follows the described steps, variations may exist in terms negotiated between the parties. These variations could include the specifics of debt reduction, financial incentives, or conditions associated with any remaining debt liability. Conclusion: The Offer by Borrower of Deed in Lieu of Foreclosure in Indiana provides borrowers with an opportunity to avoid the detrimental effects of foreclosure, offering a mutually beneficial solution for both parties involved. By understanding the process and its advantages, homeowners facing financial hardship can make informed decisions and work towards a more stable financial future.