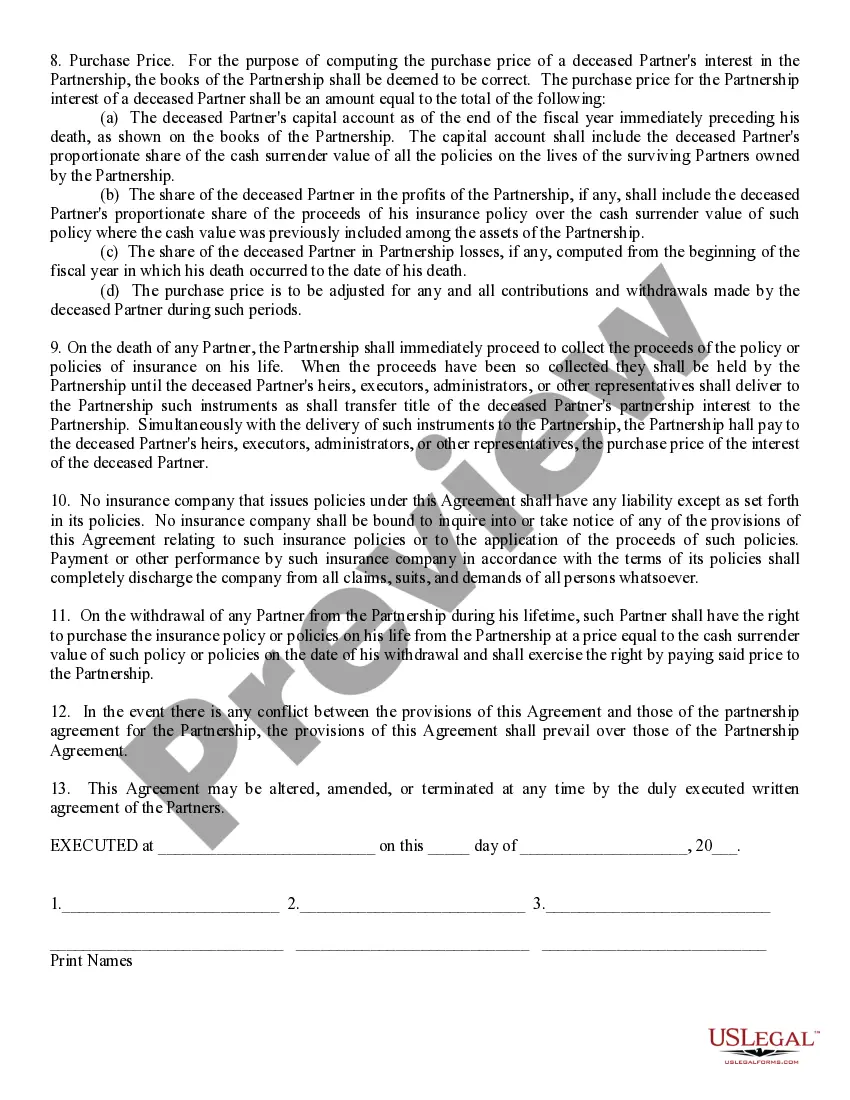

Title: Indiana Sale of Deceased Partner's Interest: Understanding the Process and Types Description: When a partner passes away, their ownership interest in a business partnership becomes a part of their estate. In Indiana, the sale of a deceased partner's interest involves specific legal procedures that should be followed to ensure a smooth transition of ownership. This detailed description explains the process and explores different types of Indiana Sale of Deceased Partner's Interest. 1. Indiana Sale of Deceased Partner's Interest — Process: Upon the death of a partner, the first step is to review the partnership agreement to determine how the deceased partner's interest should be handled. Often, the agreement includes provisions outlining the sale or transfer of the interest. If no specific provisions are mentioned, the Indiana Revised Uniform Partnership Act (RPA) governs the situation. Next, the surviving partners or the executor of the deceased partner's estate should obtain a fair market value appraisal of the interest. This appraisal determines the value of the deceased partner's share in the partnership. Once the value is determined, the surviving partners or the estate executor can explore different options for selling the deceased partner's interest. These options include selling the interest to a third party, offering it to the existing partners, or liquidating the partnership. 2. Types of Indiana Sale of Deceased Partner's Interest: a. Sale to a Third Party: In this scenario, the interest of the deceased partner is sold to an external individual or entity. Both the surviving partners and the deceased partner's estate should agree on the terms of the sale, including the selling price and any necessary buyout arrangements. b. Offer to Existing Partners: If the partnership agreement grants the surviving partners the right of first refusal, they have the opportunity to purchase the deceased partner's interest. The remaining partners can negotiate the terms of the sale, considering the value appraisal and their own financial resources. c. Liquidation of the Partnership: When it is not feasible or practical to sell the deceased partner's interest, the partnership may opt for liquidation. In this case, the partnership will be dissolved, and the assets will be sold to settle obligations and distribute remaining proceeds to partners, including the estate of the deceased partner. Conclusion: The Indiana sale of a deceased partner's interest involves a careful process to ensure a fair and legal transition of ownership. Partnerships should seek legal guidance to navigate the specific provisions of the partnership agreement or rely on the RPA when outlining the sale and valuation process. Having a clear understanding of the available options, such as selling to a third party, offering to existing partners, or liquidating the partnership, helps partners or estate executors make informed decisions to honor the deceased partner's interests.

Indiana Sale of Deceased Partner's Interest

Description

How to fill out Indiana Sale Of Deceased Partner's Interest?

If you want to aggregate, download, or print authentic document templates, utilize US Legal Forms, the largest array of legal forms available online.

Leverage the website's straightforward and convenient search to obtain the documents you need.

Different templates for business and personal purposes are categorized by types and states, or keywords. Use US Legal Forms to acquire the Indiana Sale of Deceased Partner's Interest with just a few clicks.

Every legal document template you purchase is yours forever. You will have access to all forms you downloaded within your account.

Stay competitive and download, and print the Indiana Sale of Deceased Partner's Interest with US Legal Forms. There are countless professional and state-specific forms you can utilize for your business or personal needs.

- If you are already a US Legal Forms customer, Log Into your account and click on the Download option to find the Indiana Sale of Deceased Partner's Interest.

- You can also access forms you previously downloaded in the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Make sure you have selected the form for your appropriate area/region.

- Step 2. Use the Preview option to review the form's details. Don't forget to read the information.

- Step 3. If you are not satisfied with the form, use the Search field at the top of the screen to find other variations of the legal form template.

- Step 4. Once you have identified the form you need, click on the Purchase now option. Choose your preferred payment plan and provide your details to register for an account.

- Step 5. Complete the transaction. You can use your Visa, Mastercard, or PayPal account to finalize the payment.

- Step 6. Choose the format of the legal form and download it to your device.

- Step 7. Complete, edit, and print or sign the Indiana Sale of Deceased Partner's Interest.

Form popularity

FAQ

Car title transfer in Indiana In Indiana, the vehicle buyer can complete a title transfer online through the BMV's virtual portal or in person at a local branch. It must be done within 45 days of the change of ownership or you will be subject to late fees.

A TOD Beneficiary who has acquired ownership of a vehicle, as a result of being listed on the vehicle's Indiana Certificate of Title as a TOD beneficiary, must take the Indiana title containing the TOD designation and a copy of the decedent's death certificate to a BMV license branch to apply for a new Indiana title.

A TOD Beneficiary who has acquired ownership of a vehicle, as a result of being listed on the vehicle's Indiana Certificate of Title as a TOD beneficiary, must take the Indiana title containing the TOD designation and a copy of the decedent's death certificate to a BMV license branch to apply for a new Indiana title.

A TOD beneficiary or any beneficiary who acquires a vehicle through inheritance must take the title designating them as such, along with a copy of the deceased person's death certificate to an Indiana Bureau of Motor Vehicles location to apply for a new title. They must also pay state title and transfer fees.

A transfer on death deed can be a very helpful planning tool when designing an estate plan. Indiana is one of many states that allows the transfer of real property by a transfer on death deed.

Transferring Ownership Of A Vehicle Registered In The Name Of A Deceased ParentID and Death Certificate of the deceased;Will nominating an Executor or if there is no Will a Nomination Form signed by all the heirs of the deceased parent nominating a family member as an Executor;ID of the nominated Executor; and.More items...

There is no federal inheritance taxthat is, a tax on the sum of assets an individual receives from a deceased person. However, a federal estate tax applies to estates larger than $11.7 million for 2021 and $12.06 million for 2022. The tax is assessed only on the portion of an estate that exceeds those amounts.

In general, estates or beneficiaries of Indiana residents are required to file an inheritance tax return (Form IH-6) if the value of transfers to any beneficiary is greater than the exemption allowed for that beneficiary.

Inheritances are not considered income for federal tax purposes, whether you inherit cash, investments or property. However, any subsequent earnings on the inherited assets are taxable, unless it comes from a tax-free source.

Class A. This group includes the deceased person's parents, children, stepchildren, grandparents, grandchildren, and other lineal ancestors and lineal descendants. These people don't owe tax unless they inherit more than $100,000.

Interesting Questions

More info

Interconnect Wolters Kluwer Interconnect History Help Login A new way of making connections between computers. The interface is based on WSL, the Windows Virtual Machine Environment.