This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

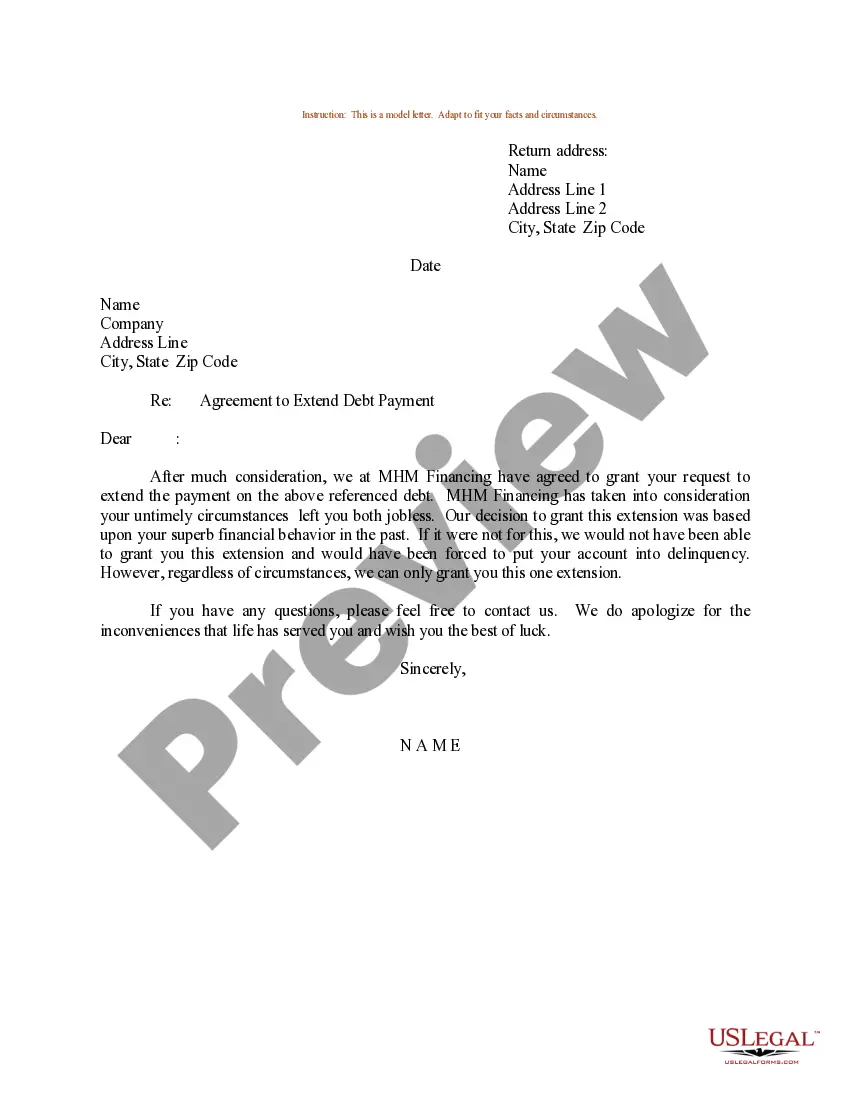

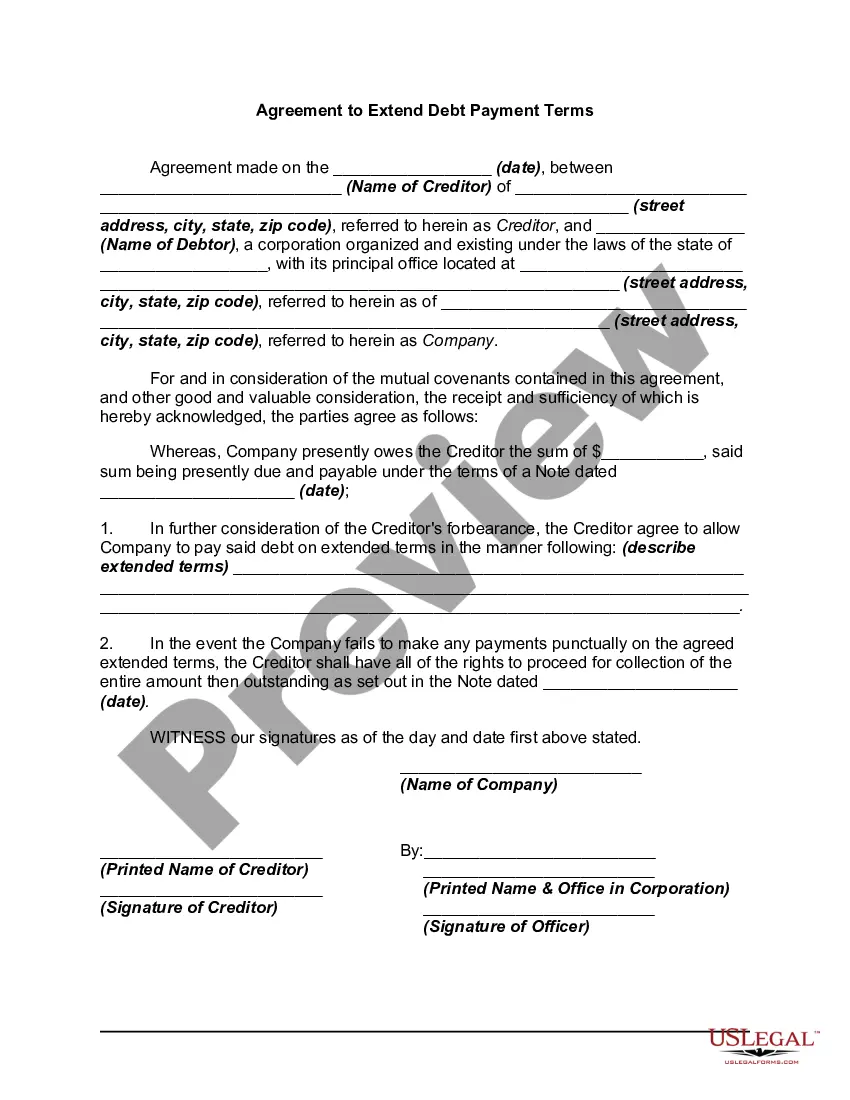

Indiana Agreement to Extend Debt Payment

Instant download

Description

Free preview

How to fill out Agreement To Extend Debt Payment?

Have you found yourself in a situation where you require paperwork for either business or specific reasons almost daily.

There are numerous legal document templates accessible online, but finding ones you can trust isn’t simple.

US Legal Forms offers a multitude of form templates, including the Indiana Agreement to Extend Debt Payment, which are designed to comply with both federal and state regulations.

Once you have located the right form, click on Get now.

Select the pricing plan you prefer, complete the necessary information to create your account, and pay for the transaction using your PayPal or credit card.

- If you are already familiar with the US Legal Forms website and possess an account, simply Log In.

- After logging in, you can download the Indiana Agreement to Extend Debt Payment template.

- If you do not have an account and wish to start using US Legal Forms, follow these instructions.

- Locate the form you require and ensure it is for the correct area/region.

- Utilize the Preview button to examine the form.

- Review the description to confirm that you have selected the correct form.

- If the form isn’t what you’re searching for, use the Search field to find the form that fits your needs.

Form popularity

FAQ

For the 2025 tax year, you can file taxes as early as January 1, 2026. If you are under an Indiana Agreement to Extend Debt Payment, you may want to file as early as possible to avoid any late fees and manage your debt effectively. Early filing allows you to address any issues before deadlines approach, ensuring a more organized approach to your financial responsibilities. Consider using platforms like uslegalforms to simplify your filing process.

The IRS typically begins approving refunds in late January or early February each year. In 2025, you can expect refunds to be processed around the same time, but specific timelines may vary. If you have an Indiana Agreement to Extend Debt Payment, be sure to consider how your tax refund status affects your overall financial situation. Staying updated with IRS announcements can help you plan accordingly.

Yes, Indiana does accept federal extensions for partnerships. If a partnership files for a federal extension, it generally gets an automatic extension for Indiana taxes as well. However, if you have an Indiana Agreement to Extend Debt Payment, you may need to comply with specific stipulations outlined in that agreement. It's wise to consult with a tax advisor to ensure you meet all local requirements.

You can begin filing your taxes in Indiana as early as January 1, 2026, for the 2025 tax year. For those with an Indiana Agreement to Extend Debt Payment, early filing can help manage your financial situation more effectively. Getting your documents ready in advance allows for a smoother process and can help in minimizing any penalties associated with late payments. Always consult a tax professional for personalized advice.

Path Lift occurs on February 15, 2026. This date is important as the IRS will not start processing certain tax returns until after this day. If you have an Indiana Agreement to Extend Debt Payment, understanding this timeline is crucial to plan your tax submission correctly. Be prepared to submit your documents well before this date to ensure a smooth filing process.

You can file your taxes in Indiana for the year 2025 starting January 1, 2026. However, if you have an Indiana Agreement to Extend Debt Payment, be sure to check your specific deadlines and requirements. This agreement may allow additional time for you to file beyond the usual deadlines, which can be beneficial for managing your tax obligations. It's advisable to stay informed about any updates from the state to ensure compliance.

To create a debt payment plan, start by assessing your total debt and monthly income. Outline a realistic budget that allows you to allocate funds toward your debts. Incorporating an Indiana Agreement to Extend Debt Payment can facilitate this plan by clearly defining your obligations and timelines for repayment.

Writing a debt agreement involves detailing the specifics of the owed amount, payment terms, and any applicable interest. Start by clearly identifying the parties and their obligations. Using an Indiana Agreement to Extend Debt Payment can simplify this process and ensure that you include all necessary components for a valid agreement.

In Indiana, the statute of limitations for most debts is six years. This period starts from the date of the last payment or the last acknowledgment of the debt. Understanding this timeframe is crucial when considering legal actions or negotiating an Indiana Agreement to Extend Debt Payment.

To write a debt payment agreement, explicitly state the debtor's obligations, including the total amount owed and the payment terms. Include sections for any interest rates, late fees, and a timeline for repayment. For those in Indiana, an Indiana Agreement to Extend Debt Payment can provide essential guidance in drafting an effective and enforceable agreement.