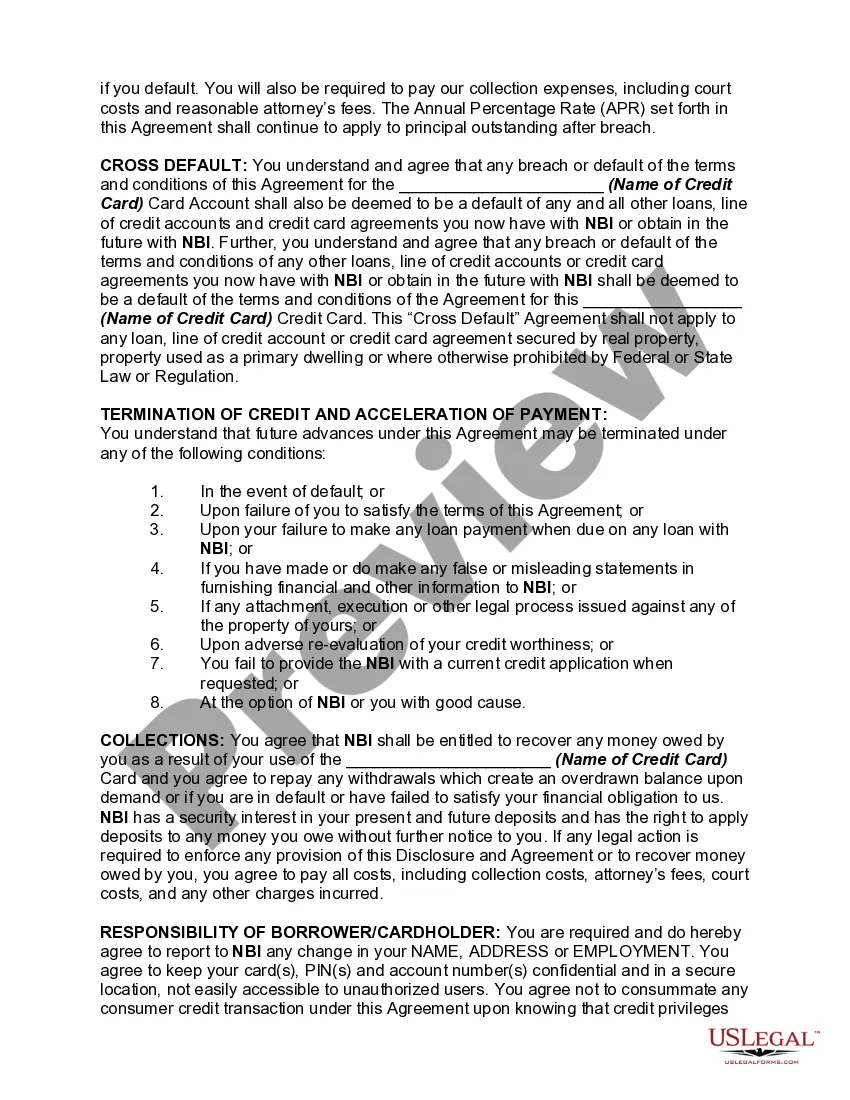

The Indiana Credit Card Agreement and Disclosure Statement is a crucial document that outlines the terms and conditions, fees, and interest rates associated with a credit card issued in the state of Indiana. This agreement serves as a contract between the credit card issuer and the cardholder, detailing the rights and responsibilities of both parties. The primary purpose of the Indiana Credit Card Agreement and Disclosure Statement is to provide the cardholder with a comprehensive understanding of the credit card's features, costs, and obligations associated with its use. It ensures transparency and consumer protection by clearly explaining the terms of the credit card agreement. Key elements included in the agreement and disclosure statement involve the annual percentage rate (APR), which represents the cost of borrowing on the credit card. It also covers the grace period, payment due dates, minimum payment requirements, late payment fees, and over-limit fees. Moreover, the agreement may address cash advances, balance transfers, and promotional offers, such as introductory APR's or bonus rewards. It is essential for cardholders to carefully review these sections to fully comprehend any advantages or restrictions associated with their credit card. Additionally, the Indiana Credit Card Agreement and Disclosure Statement typically discuss liability for unauthorized charges, dispute resolution processes, and the cardholder's responsibilities in case of a lost or stolen card. These sections ensure both parties have a clear understanding of how to handle potential issues or fraudulent activities. While there may not be specific types of Indiana Credit Card Agreement and Disclosure Statements, they are unique to each credit card issuer. Different credit card companies, financial institutions, or banks may have their own templates, terms, and conditions. Therefore, it is crucial for individuals to review and compare multiple agreements before selecting a credit card that suits their financial needs. In conclusion, the Indiana Credit Card Agreement and Disclosure Statement is a detailed document that provides cardholders with key information regarding the terms, costs, and obligations associated with their credit card. By carefully reviewing and understanding this agreement, individuals can make informed decisions and effectively manage their credit card accounts.

Indiana Credit Card Agreement and Disclosure Statement

Description

How to fill out Indiana Credit Card Agreement And Disclosure Statement?

Have you been in the position in which you will need paperwork for possibly enterprise or person reasons almost every day time? There are plenty of legitimate file layouts available on the net, but finding ones you can rely on isn`t straightforward. US Legal Forms delivers 1000s of develop layouts, such as the Indiana Credit Card Agreement and Disclosure Statement, that happen to be created to satisfy state and federal specifications.

When you are already knowledgeable about US Legal Forms site and also have a free account, merely log in. Following that, you are able to download the Indiana Credit Card Agreement and Disclosure Statement design.

Unless you come with an account and wish to start using US Legal Forms, follow these steps:

- Obtain the develop you will need and ensure it is for the appropriate town/county.

- Make use of the Review option to review the form.

- Look at the explanation to actually have chosen the correct develop.

- If the develop isn`t what you are seeking, utilize the Research industry to obtain the develop that fits your needs and specifications.

- Once you find the appropriate develop, click on Purchase now.

- Select the prices strategy you need, complete the specified info to create your bank account, and buy your order making use of your PayPal or credit card.

- Choose a practical document formatting and download your duplicate.

Find each of the file layouts you may have bought in the My Forms food selection. You can obtain a more duplicate of Indiana Credit Card Agreement and Disclosure Statement at any time, if possible. Just select the necessary develop to download or print the file design.

Use US Legal Forms, by far the most considerable selection of legitimate varieties, to conserve some time and stay away from faults. The service delivers professionally made legitimate file layouts that you can use for a selection of reasons. Make a free account on US Legal Forms and begin creating your life easier.

Form popularity

FAQ

Terms and conditions for a credit card spell out the fees and interest charges you could incur as a cardholder. This document provides the credit card's annual percentage rate (APR) for purchases, the APR for balance transfers, the APR for cash advances, and the penalty APR.

Definition. A credit card disclosure is a document that outlines all of the fees, costs, interest rates, and terms that a customer could experience while using the credit card. Institutions that offer credit cards are required by law to disclose this information.

You should be able to find pricing and terms information adjacent to any credit card application. If you can't locate this information, contact the issuer directly and request it. They are required by law to give it to you.

In addition to pricing information, your credit card agreement will include every detail of your credit card including: The types of transactions you can make on your credit card. Your credit limit and information about how your credit card issuer can change it. Details about using your credit card in another country.

Not only will your credit rating suffer, but the creditor can use the same collection methods against you as against the primary borrower, including suing you or garnishing your wages.

A cardholder agreement is a legal document outlining the terms under which a credit card is offered to a customer. Among other provisions, the cardholder agreement states the annual percentage rate (APR) of the card, as well as how the card's minimum payments are calculated.

1?? As such, customers considering accepting a new credit card should carefully review their cardholder agreement in order to confirm that the actual provisions of the card are as advertised. Although their details vary, most cardholder agreements are written using a similar format and in a straightforward tone.

You may also have your interest rates raised to the penalty APR for all new purchases. One missed or late minimum payment also could mean that you lose your introductory APR and have to start paying the higher long term rate on your existing balance. Late or missed payments can also hurt your credit history.