Indiana General Journal

Description

How to fill out General Journal?

US Legal Forms - one of the largest collections of legal forms in the United States - offers a variety of legal document templates that you can download or print.

By using the website, you can discover numerous forms for business and personal purposes, categorized by type, state, or keywords. You can quickly find the latest forms such as the Indiana General Journal.

If you already have a subscription, Log In and download the Indiana General Journal from the US Legal Forms library. The Download button will appear on each form you view. You can access all previously downloaded forms in the My documents section of your account.

Complete the transaction. Use your credit card or PayPal account to finalize the payment.

Choose the format and download the form to your device. Make edits. Fill out, modify, print, and sign the downloaded Indiana General Journal. Each template you add to your account has no expiration date and belongs to you indefinitely. Therefore, if you want to download or print another copy, simply visit the My documents section and click on the form you desire. Access the Indiana General Journal through US Legal Forms, which boasts one of the most extensive collections of legal document templates. Utilize a vast array of professional and state-specific templates that satisfy your business or personal requirements.

- Ensure you have selected the correct form for your area/county.

- Use the Preview option to review the content of the form.

- Read the form description to confirm you have chosen the correct one.

- If the form does not meet your needs, use the Search feature at the top of the screen to find the appropriate one.

- If you are satisfied with the form, confirm your choice by clicking the Purchase now button.

- Then, select the payment plan you prefer and provide your information to create an account.

Form popularity

FAQ

The basic rules governing journals, including the Indiana General Journal, are essential for accurate accounting. Ensure each entry records all necessary details, follow the dual aspect concept by including both debits and credits, and maintain clarity in descriptions. Abiding by these rules facilitates easy tracking and verification of financial information.

To make a general journal entry in the Indiana General Journal, start by clearly defining the transaction. List the date, the involved accounts, and designate which will be debited and which will be credited. Write a concise description to explain the purpose of the entry, ensuring accuracy in amounts.

Examples of general journal entries in the Indiana General Journal can include recording sales transactions, purchases on credit, or adjusting entries for accrued expenses. Each example will illustrate the debit and credit accounts involved, which showcases how transactions affect the overall accounting cycle.

When using the Indiana General Journal in accounting, it’s vital to establish consistency and accuracy. Always record transactions promptly, ensure that every entry reflects truthfully to the accounts involved, and provide adequate descriptions. Regular reconciliation of entries helps maintain the integrity of your records.

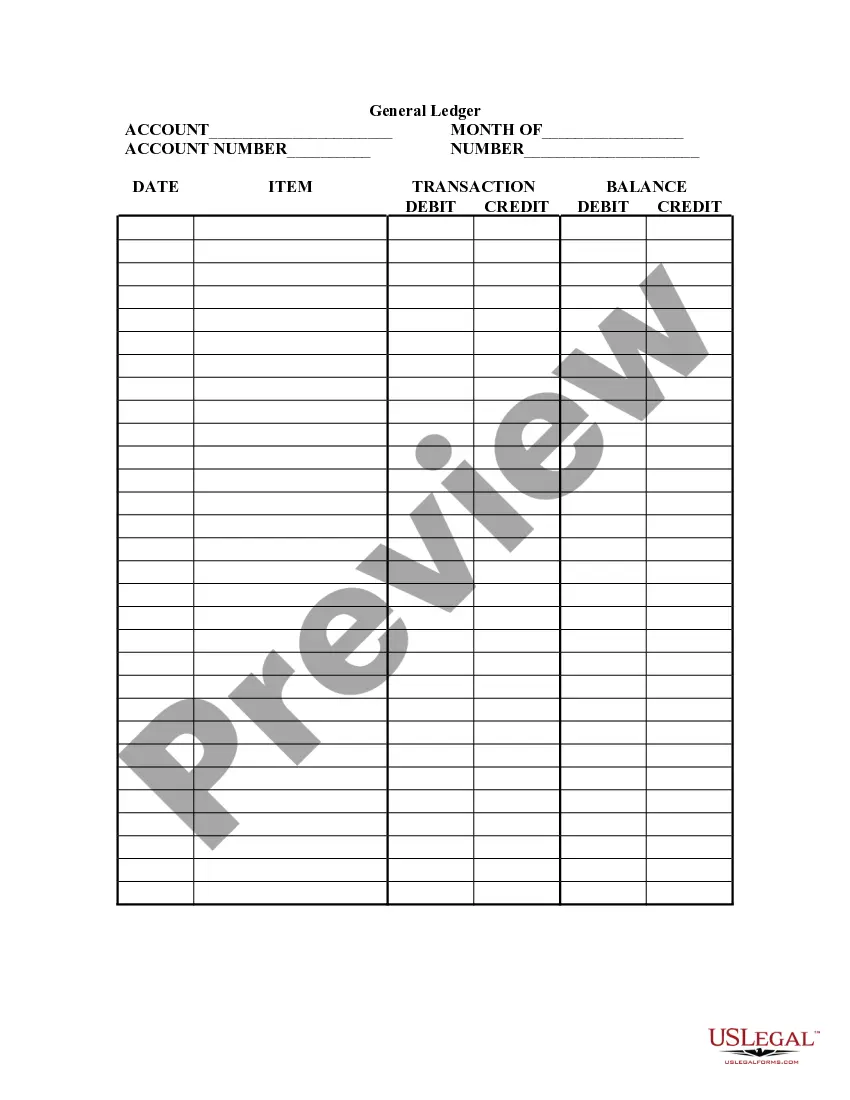

The Indiana General Journal and the general ledger serve distinct purposes in accounting. The general journal records transactions in chronological order, whereas the general ledger organizes these entries by account. This makes it easier to track financial activities and balances associated with specific accounts.

The Indiana General Journal serves various functions, including recording initial transactions, providing a chronological history of all entries, facilitating adjustments, enabling regular financial reviews, and serving as a basis for compiling the general ledger. Each of these uses contributes to maintaining orderly and accurate financial records.

Writing in the Indiana General Journal requires a clear layout. Start with the date, followed by account names, and state the amounts to be debited or credited. Use concise language to describe each transaction, ensuring you maintain a logical flow that others can understand.

Recording a general journal entry in the Indiana General Journal involves a few simple steps. First, jot down the date of the transaction, then list the account titles along with their respective debits and credits. Don’t forget to provide a clear description of the transaction for future reference.

To efficiently use the Indiana General Journal, follow some key guidelines. Keep your entries organized by date, be specific with descriptions, and record transactions immediately to avoid mistakes. Regularly review your entries to ensure accuracy and completeness, which will aid in financial reporting.

When using the Indiana General Journal, adhere to these three fundamental rules: first, each transaction must be recorded in chronological order; second, every entry must have an equal amount of debits and credits; and finally, ensure that clear and concise descriptions accompany each entry for easy reference.