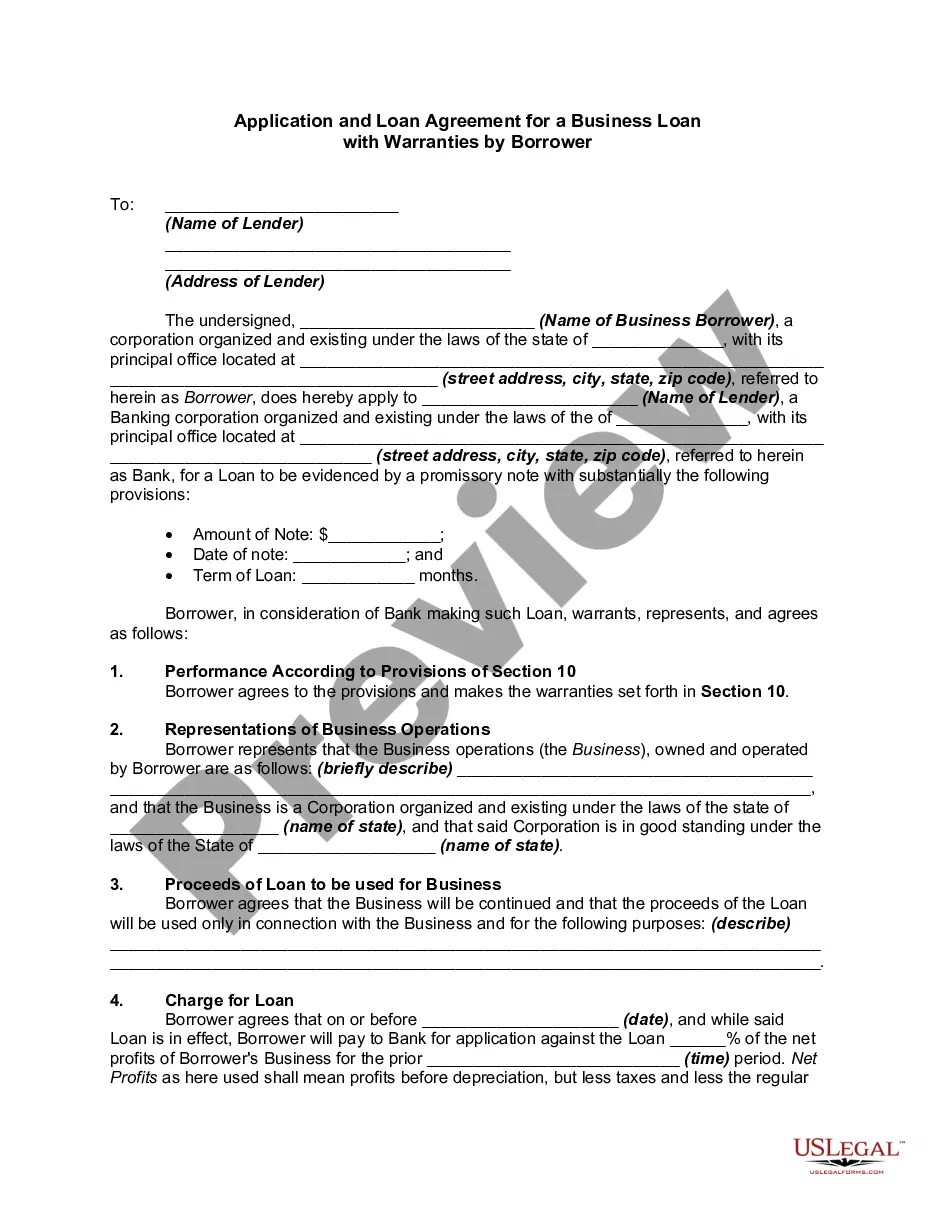

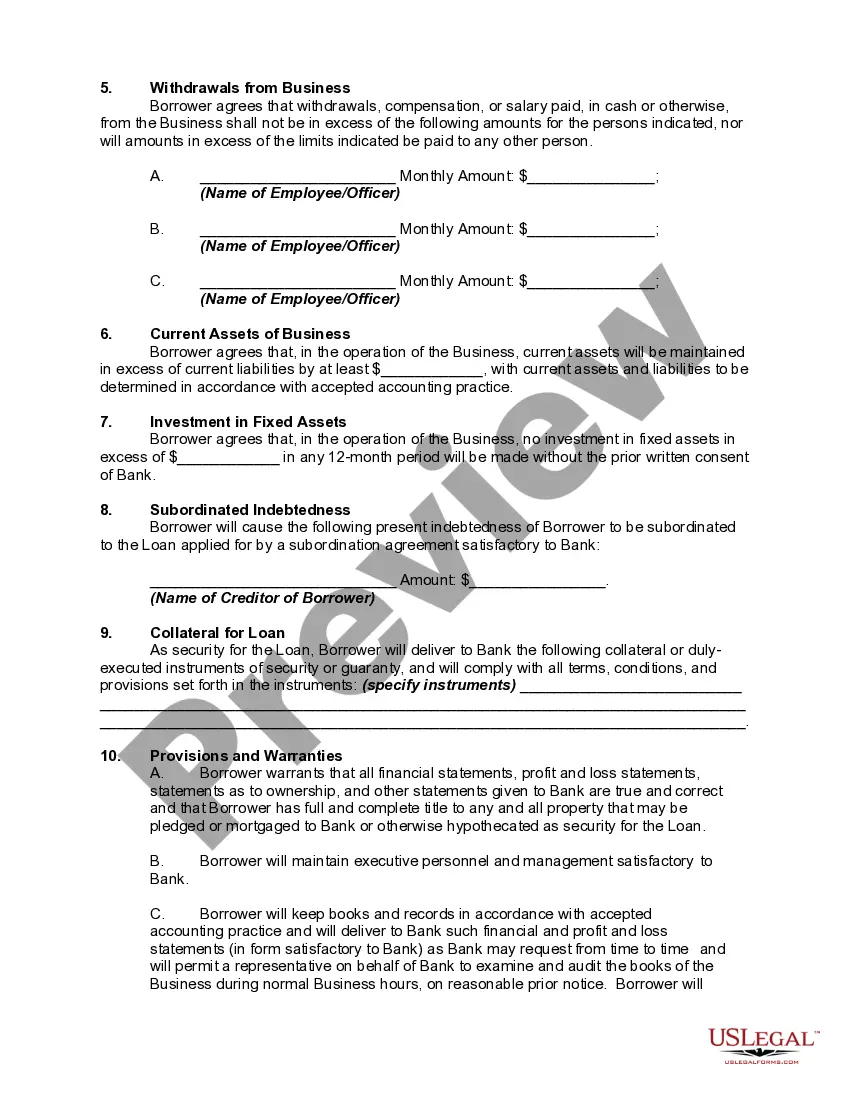

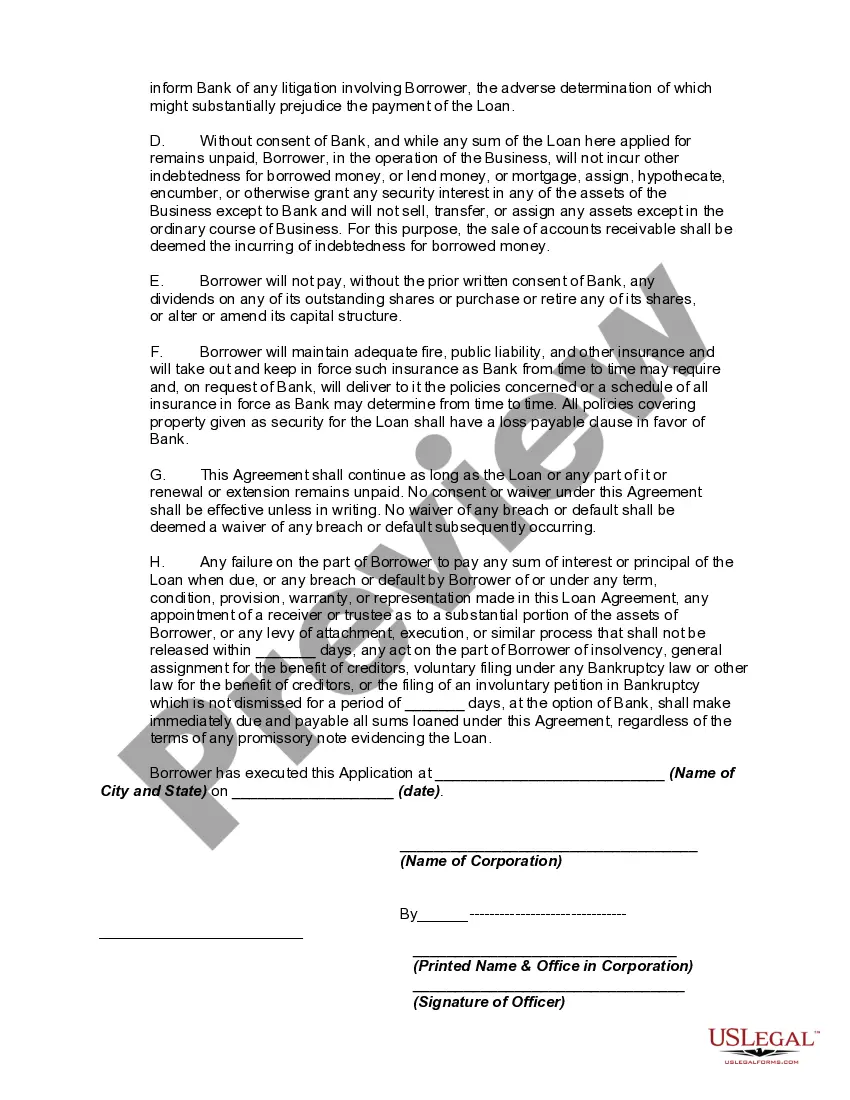

As a general matter, a loan by a bank is the borrowing of money by a person or entity who promises to return it on or before a specific date, with interest, or who pledges collateral as security for the loan and promises to redeem it at a specific later date. Loans are usually made on the basis of applications, together with financial statements submitted by the applicants.

The Federal Truth in Lending Act and the regulations promulgated under the Act apply to certain credit transactions, primarily those involving loans made to a natural person and intended for personal, family, or household purposes and for which a finance charge is made, or loans that are payable in more than four installments. However, said Act and regulations do not apply to a business loan of this type.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The Indiana Application and Loan Agreement for a Business Loan with Warranties by Borrower is a legal document used in the state of Indiana to facilitate the borrowing of funds by a business entity. This agreement outlines the terms and conditions under which the loan will be provided, including the repayment schedule, interest rates, and any additional fees or charges. The application portion of the agreement requires the borrower to provide detailed information about their business, such as its legal name, address, ownership structure, and financial history. Additionally, the borrower may also be required to disclose any outstanding debts, liens, or legal proceedings. The loan agreement section of the document establishes the specific terms of the loan, including the principal amount, interest rate, and repayment period. It also includes provisions for any collateral or guarantees provided by the borrower to secure the loan. These collateral arrangements can come in the form of real estate, equipment, inventory, or other valuable assets owned by the borrower. Furthermore, the "Warranties by Borrower" section of the agreement is crucial as it outlines the assurances made by the borrower regarding the accuracy and completeness of the information provided in the application. This section emphasizes that the borrower has the legal authority to enter into the agreement and that they have not withheld any material facts that could affect the lender's decision to extend the loan. It is important to note that there may be variations of the Indiana Application and Loan Agreement for a Business Loan with Warranties by Borrower, specific to various types of loans or industries. Some common types include: 1. Small Business Administration (SBA) Loan Agreement: This agreement is tailored for small businesses seeking financing through SBA loan programs, which offer government-backed guarantees to lenders. 2. Commercial Real Estate Loan Agreement: This agreement is designed for businesses looking to secure financing for the purchase, construction, or renovation of commercial properties. 3. Working Capital Loan Agreement: This agreement focuses on providing short-term funding to cover operational expenses or facilitate growth in a business's day-to-day operations. 4. Equipment Financing Loan Agreement: This type of agreement is used when businesses need funds to purchase or lease equipment necessary for their operations. In conclusion, the Indiana Application and Loan Agreement for a Business Loan with Warranties by Borrower is a comprehensive legal document that outlines the terms, conditions, and warranties associated with a business loan in Indiana. By carefully reviewing and understanding these agreements, both borrowers and lenders can ensure a smooth and mutually beneficial financial arrangement.The Indiana Application and Loan Agreement for a Business Loan with Warranties by Borrower is a legal document used in the state of Indiana to facilitate the borrowing of funds by a business entity. This agreement outlines the terms and conditions under which the loan will be provided, including the repayment schedule, interest rates, and any additional fees or charges. The application portion of the agreement requires the borrower to provide detailed information about their business, such as its legal name, address, ownership structure, and financial history. Additionally, the borrower may also be required to disclose any outstanding debts, liens, or legal proceedings. The loan agreement section of the document establishes the specific terms of the loan, including the principal amount, interest rate, and repayment period. It also includes provisions for any collateral or guarantees provided by the borrower to secure the loan. These collateral arrangements can come in the form of real estate, equipment, inventory, or other valuable assets owned by the borrower. Furthermore, the "Warranties by Borrower" section of the agreement is crucial as it outlines the assurances made by the borrower regarding the accuracy and completeness of the information provided in the application. This section emphasizes that the borrower has the legal authority to enter into the agreement and that they have not withheld any material facts that could affect the lender's decision to extend the loan. It is important to note that there may be variations of the Indiana Application and Loan Agreement for a Business Loan with Warranties by Borrower, specific to various types of loans or industries. Some common types include: 1. Small Business Administration (SBA) Loan Agreement: This agreement is tailored for small businesses seeking financing through SBA loan programs, which offer government-backed guarantees to lenders. 2. Commercial Real Estate Loan Agreement: This agreement is designed for businesses looking to secure financing for the purchase, construction, or renovation of commercial properties. 3. Working Capital Loan Agreement: This agreement focuses on providing short-term funding to cover operational expenses or facilitate growth in a business's day-to-day operations. 4. Equipment Financing Loan Agreement: This type of agreement is used when businesses need funds to purchase or lease equipment necessary for their operations. In conclusion, the Indiana Application and Loan Agreement for a Business Loan with Warranties by Borrower is a comprehensive legal document that outlines the terms, conditions, and warranties associated with a business loan in Indiana. By carefully reviewing and understanding these agreements, both borrowers and lenders can ensure a smooth and mutually beneficial financial arrangement.