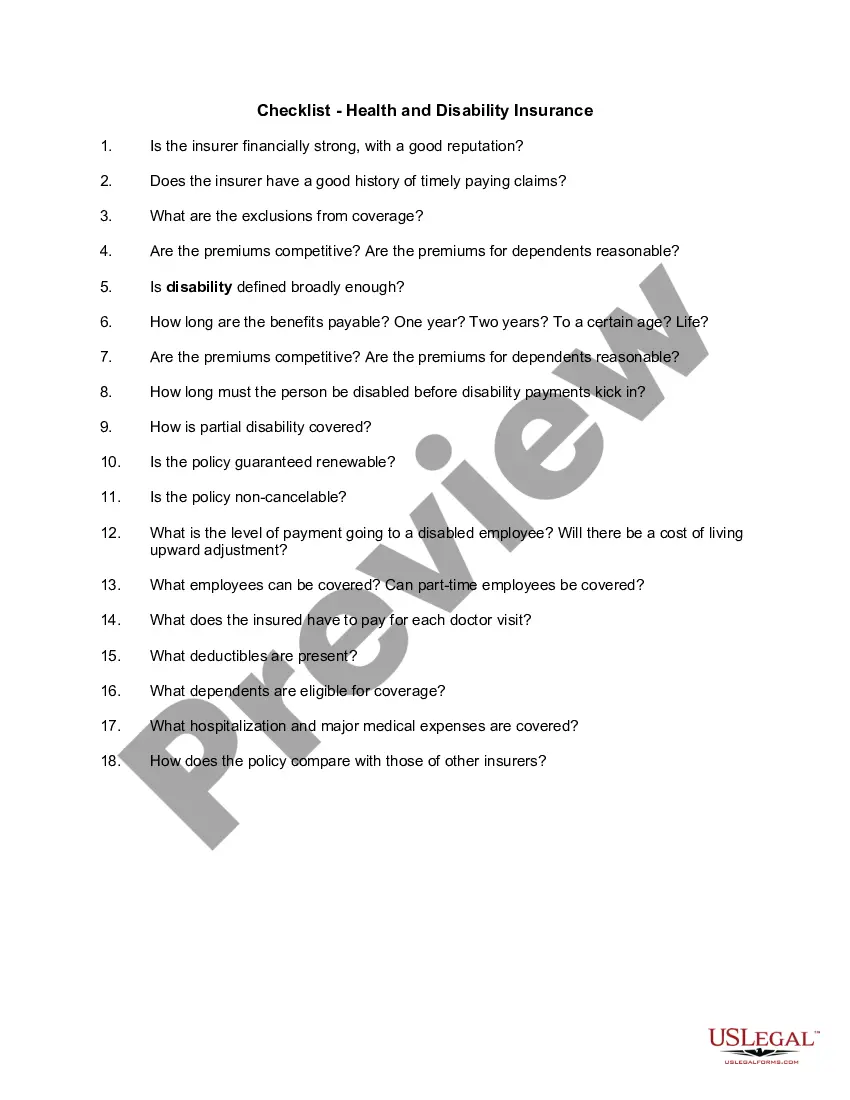

Indiana Checklist — Health and Disability Insurance: A Comprehensive Guide for Residents When it comes to ensuring your well-being and peace of mind, having the right health and disability insurance in Indiana is essential. This comprehensive checklist will provide you with detailed information about the types of coverage available and assist you in selecting the most suitable insurance options for your needs. 1. Health Insurance: — Individual Health Insurance: This type of coverage is suitable for individuals who are not eligible for employer-sponsored plans or government programs. — Group Health Insurance: Typically provided by employers, this insurance covers a group of individuals and often offers more comprehensive coverage at a lower cost. — Medicare: Aimed at senior citizens, Medicare is a federal health insurance program that provides coverage for medical services, hospital stays, and prescription drugs. — Medicaid: Designed for individuals and families with limited income, Medicaid is a state and federal program that offers free or low-cost health coverage. 2. Disability Insurance: — Short-Term Disability Insurance: This type of insurance provides coverage for a limited period when an individual is unable to work due to illness, injury, or pregnancy. — Long-Term Disability Insurance: Long-term disability insurance offers coverage for an extended period, helping to replace lost income in the event of a long-term disability that prohibits work. 3. Key Factors to Consider: — Benefit Coverage: Assess the policies to determine the extent of coverage they offer, including hospitalization, doctor visits, prescription drugs, and preventative care. — Network of Providers: Ensure that your preferred healthcare providers and hospitals are within the insurer's network to maximize coverage and reduce out-of-pocket expenses. — Premiums and Deductibles: Compare costs between different insurers, considering both monthly premiums and deductibles, to find the most affordable option that meets your needs. — Prescription Drugs: Evaluate whether the insurance covers necessary medications and inquire about any restrictions or exceptions when it comes to specific drugs. — Additional Benefits: Some insurance plans may include extra benefits such as wellness programs, maternity coverage, dental and vision care, or telemedicine services. Determine if these supplementary benefits align with your requirements. 4. Enrollment and Eligibility: — Open Enrollment: Indiana typically follows the nationwide open enrollment period, during which individuals can enroll or make changes to their health insurance plan. It usually takes place between November and December for coverage effective in the following year. — Qualifying Life EventsOutsideof the open enrollment period, individuals experiencing certain life events, such as marriage, divorce, birth, adoption, or loss of job-based coverage, may be eligible for a Special Enrollment Period. Remember, it is crucial to conduct thorough research, compare different plans, and seek professional advice to make the most informed decision about your health and disability insurance coverage in Indiana. By carefully considering these factors and reviewing various options, you can safeguard your health and financial well-being for the future.

Indiana Checklist - Health and Disability Insurance

Description

How to fill out Indiana Checklist - Health And Disability Insurance?

Are you presently inside a placement in which you need to have papers for sometimes enterprise or person functions nearly every time? There are tons of legal file layouts accessible on the Internet, but locating kinds you can trust is not easy. US Legal Forms gives 1000s of form layouts, like the Indiana Checklist - Health and Disability Insurance, that happen to be composed to fulfill federal and state specifications.

In case you are already knowledgeable about US Legal Forms internet site and also have a free account, simply log in. Following that, you can obtain the Indiana Checklist - Health and Disability Insurance design.

Unless you provide an accounts and need to begin using US Legal Forms, abide by these steps:

- Get the form you need and make sure it is for that appropriate metropolis/state.

- Take advantage of the Preview key to examine the form.

- Read the explanation to actually have chosen the proper form.

- When the form is not what you`re searching for, take advantage of the Look for field to get the form that meets your needs and specifications.

- Once you find the appropriate form, click Get now.

- Opt for the rates plan you need, submit the required details to generate your bank account, and purchase the order utilizing your PayPal or bank card.

- Decide on a handy paper structure and obtain your duplicate.

Discover every one of the file layouts you may have bought in the My Forms food selection. You can aquire a additional duplicate of Indiana Checklist - Health and Disability Insurance at any time, if necessary. Just click the required form to obtain or print out the file design.

Use US Legal Forms, probably the most comprehensive collection of legal types, to conserve time and stay away from errors. The assistance gives expertly made legal file layouts which can be used for a selection of functions. Produce a free account on US Legal Forms and initiate producing your daily life easier.