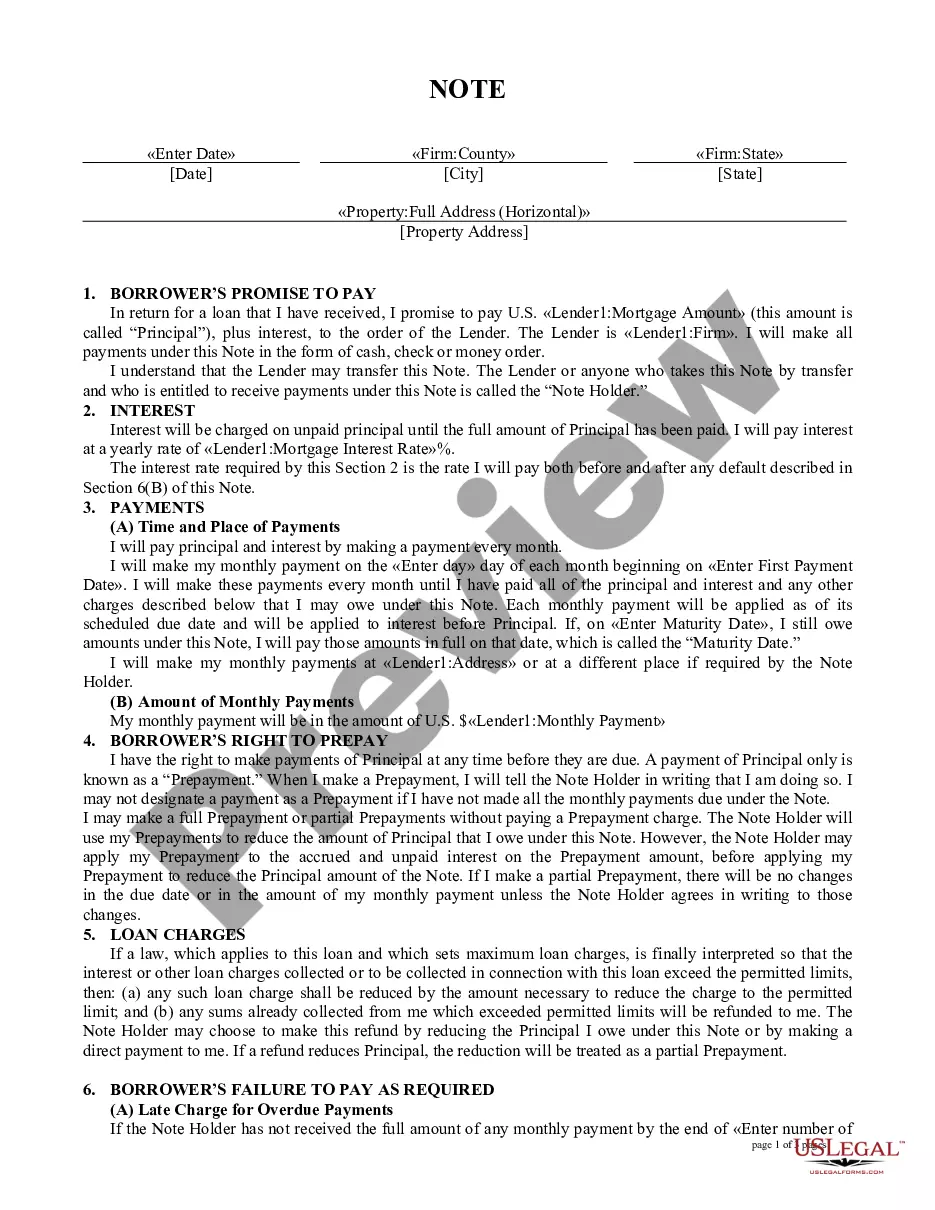

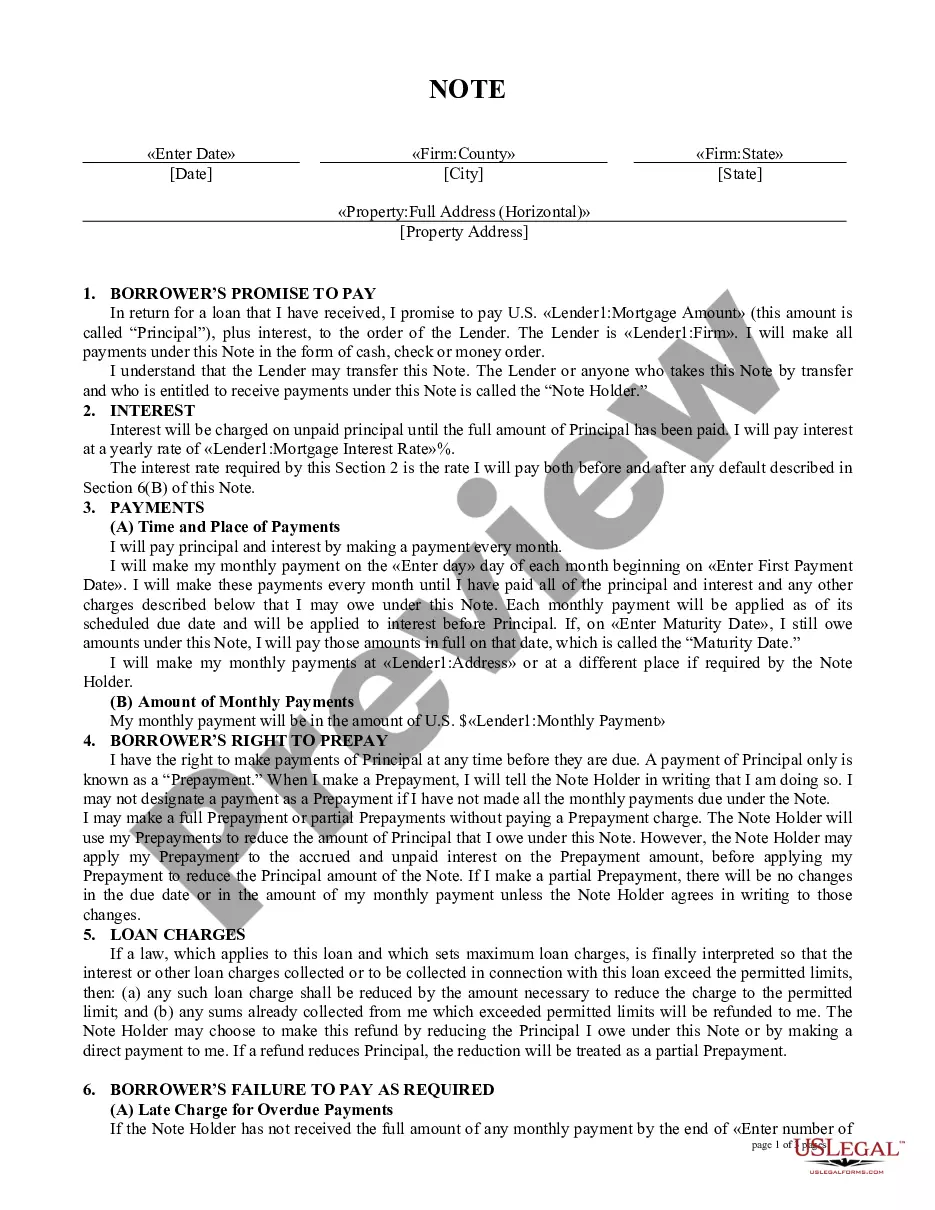

Indiana Mortgage Note

Description

How to fill out Mortgage Note?

US Legal Forms - one of many most significant libraries of legitimate types in the States - offers a wide range of legitimate file layouts you can download or produce. Using the website, you may get a large number of types for business and personal purposes, categorized by classes, states, or search phrases.You can get the latest types of types just like the Indiana Mortgage Note in seconds.

If you already possess a subscription, log in and download Indiana Mortgage Note through the US Legal Forms collection. The Obtain switch will appear on each type you see. You have access to all earlier downloaded types within the My Forms tab of your profile.

If you want to use US Legal Forms initially, here are straightforward directions to help you get started out:

- Be sure you have selected the proper type for your personal metropolis/area. Go through the Preview switch to analyze the form`s content. Look at the type outline to actually have selected the appropriate type.

- When the type doesn`t fit your demands, use the Lookup area at the top of the monitor to discover the one that does.

- Should you be content with the shape, affirm your choice by visiting the Get now switch. Then, select the costs prepare you like and provide your accreditations to register for an profile.

- Method the financial transaction. Utilize your charge card or PayPal profile to complete the financial transaction.

- Choose the formatting and download the shape on the gadget.

- Make adjustments. Complete, revise and produce and sign the downloaded Indiana Mortgage Note.

Each design you added to your money does not have an expiry date and it is the one you have permanently. So, in order to download or produce another backup, just go to the My Forms portion and click on about the type you require.

Obtain access to the Indiana Mortgage Note with US Legal Forms, the most substantial collection of legitimate file layouts. Use a large number of expert and express-specific layouts that meet your organization or personal needs and demands.

Form popularity

FAQ

A secured note is guaranteed by an interest in an asset that is worth at least the amount of the note. If you have a mortgage or an automobile loan, you are the borrower in a secured note. In the case of a mortgage, you hold a secured note with your home pledged as collateral.

Promissory Note Vs. Mortgage. A promissory note is a document between the lender and the borrower in which the borrower promises to pay back the lender, it is a separate contract from the mortgage. The mortgage is a legal document that ties or "secures" a piece of real estate to an obligation to repay money.

A loan note can offer greater flexibility than a simple loan agreement, while still being legally actionable should it need to be upheld in court. They are also much easier to enforce than an informal IOU because the legal terms of the agreement are much more clearly defined.

So, as a rule of thumb, if someone is on the Deed, they must be on the Mortgage. But just because they are on the Mortgage, doesn't mean they are on the Note.

Although it is legally enforceable, a promissory note is less formal than a loan agreement and is suitable where smaller sums of money are involved. However, its terms - which can include a specific date of repayment, interest rate and repayment schedule - are more certain than those of an IOU.

A promissory note is a written agreement containing the details of the mortgage loan, whereas a mortgage is a loan that is secured by real property. A promissory note is often referred to as a mortgage, but they are separate contracts.

A borrower usually must sign a promissory note along with the mortgage. The promissory note gives legal protections to the lender if the borrower defaults on the debt and provides clarification to the borrower so that they understand their repayment obligations.