The acknowledgement is the section at the end of a document where a notary public verifies that the signer of the document states he/she actually signed it. Typical language is: "State of ______, County of ______ (signed and sealed) On ____, 20__, before me, a notary public for said state, personally appeared _______, personally known to me, or proved to be said person by proper proof, and acknowledged that he executed the above Deed." Then the notary signs the acknowledgment and puts on his/her seal, which is usually a rubber stamp, although some still use a metal seal. The person acknowledging that he/she signed must be prepared to verify their identity with a driver's license or other accepted form of identification, and must sign the notary's journal. The acknowledgment is required for many official forms and vital for any document which must be recorded by the County Recorder or Recorder of Deeds, including deeds, deeds of trust, mortgages, powers of attorney that may involve real estate, some leases and various other papers.

Acknowledgments may also be drafted to affirm a variety of matters, acting in effect as a written confirmation of an act such as receipt of goods, services, or payment.

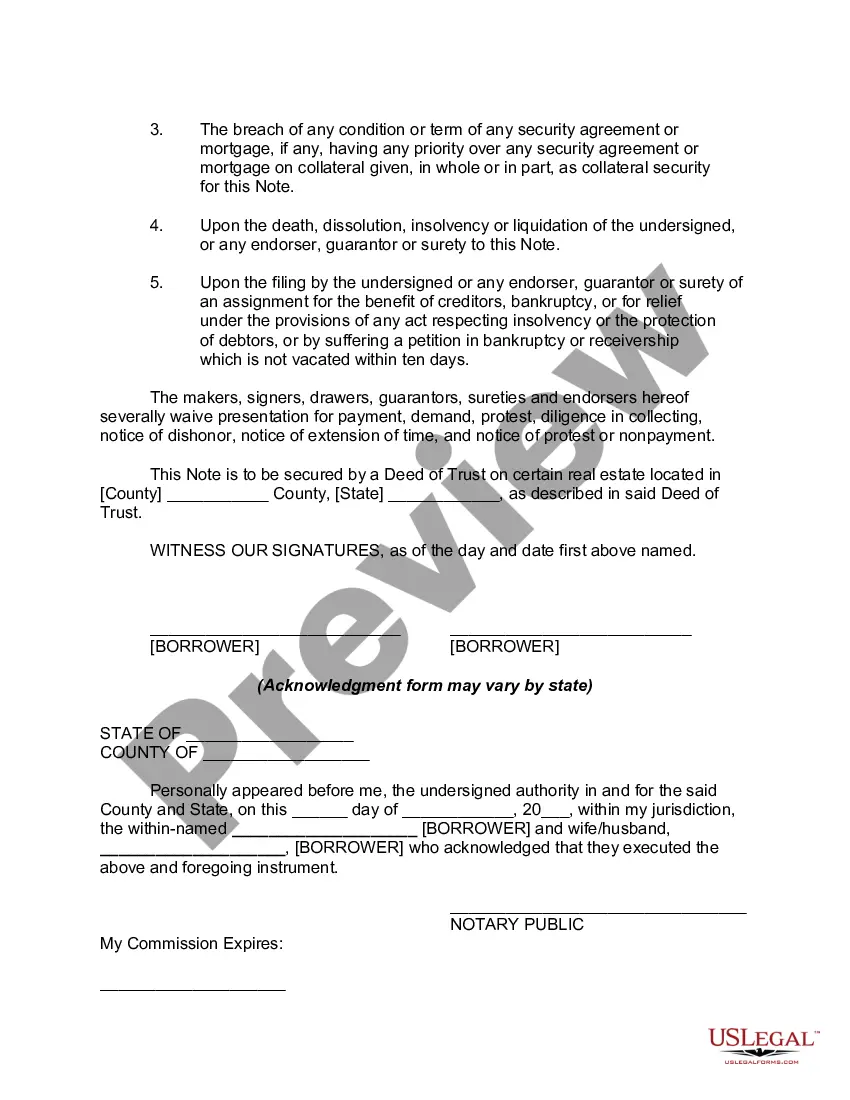

A promissory note, with acknowledgment, is a legally binding document used in the state of Indiana to establish a formal agreement between a lender and a borrower. This written contract outlines the terms and conditions of a loan or debt, including the amount borrowed, interest rate, repayment schedule, late payment penalties, and any other relevant terms. In Indiana, there are several types of promissory notes that can be used with acknowledgment, each serving a specific purpose: 1. Secured Promissory Note: This type of note includes collateral, such as property or assets, which the borrower offers as a guarantee for repayment. In case of default, the lender can seize the collateral to recover the outstanding debt. 2. Unsecured Promissory Note: Unlike the secured option, this note does not require collateral. The borrower's promise to repay the loan is solely based on their creditworthiness and trustworthiness. However, this type of note typically carries a higher interest rate to compensate for the increased risk to the lender. 3. Demand Promissory Note: This note grants the lender the right to request full repayment of the loan at any time, without specifying a fixed term. The borrower must comply with the demand within a certain period, typically 30-90 days. 4. Installment Promissory Note: This note establishes a specific repayment plan, specifying regular installment amounts, due dates, and the overall repayment period. This option offers borrowers the convenience of repaying the loan in smaller, manageable increments. 5. Balloon Promissory Note: A balloon note features a set of regular installment payments, but with a larger one-time payment due at the end of the loan term. This structure allows the borrower to have lower monthly payments throughout the agreement but requires a substantial final payment. To ensure the enforceability of a promissory note in Indiana, it is essential to have the document acknowledged. An acknowledgment is a formal declaration, usually performed before a notary public, that verifies the identity of the signatories and confirms that they have willingly and freely signed the note. This step adds a layer of legal protection to both parties involved in the loan agreement. When drafting an Indiana Promissory Note — With Acknowledgment, it is crucial to consult with an attorney or use a reliable template to ensure compliance with all relevant state laws and regulations. Additionally, including details such as the borrower's and lender's names, contact information, the date of the agreement, and clearly defining the loan terms will create a comprehensive and legally binding promissory note.A promissory note, with acknowledgment, is a legally binding document used in the state of Indiana to establish a formal agreement between a lender and a borrower. This written contract outlines the terms and conditions of a loan or debt, including the amount borrowed, interest rate, repayment schedule, late payment penalties, and any other relevant terms. In Indiana, there are several types of promissory notes that can be used with acknowledgment, each serving a specific purpose: 1. Secured Promissory Note: This type of note includes collateral, such as property or assets, which the borrower offers as a guarantee for repayment. In case of default, the lender can seize the collateral to recover the outstanding debt. 2. Unsecured Promissory Note: Unlike the secured option, this note does not require collateral. The borrower's promise to repay the loan is solely based on their creditworthiness and trustworthiness. However, this type of note typically carries a higher interest rate to compensate for the increased risk to the lender. 3. Demand Promissory Note: This note grants the lender the right to request full repayment of the loan at any time, without specifying a fixed term. The borrower must comply with the demand within a certain period, typically 30-90 days. 4. Installment Promissory Note: This note establishes a specific repayment plan, specifying regular installment amounts, due dates, and the overall repayment period. This option offers borrowers the convenience of repaying the loan in smaller, manageable increments. 5. Balloon Promissory Note: A balloon note features a set of regular installment payments, but with a larger one-time payment due at the end of the loan term. This structure allows the borrower to have lower monthly payments throughout the agreement but requires a substantial final payment. To ensure the enforceability of a promissory note in Indiana, it is essential to have the document acknowledged. An acknowledgment is a formal declaration, usually performed before a notary public, that verifies the identity of the signatories and confirms that they have willingly and freely signed the note. This step adds a layer of legal protection to both parties involved in the loan agreement. When drafting an Indiana Promissory Note — With Acknowledgment, it is crucial to consult with an attorney or use a reliable template to ensure compliance with all relevant state laws and regulations. Additionally, including details such as the borrower's and lender's names, contact information, the date of the agreement, and clearly defining the loan terms will create a comprehensive and legally binding promissory note.