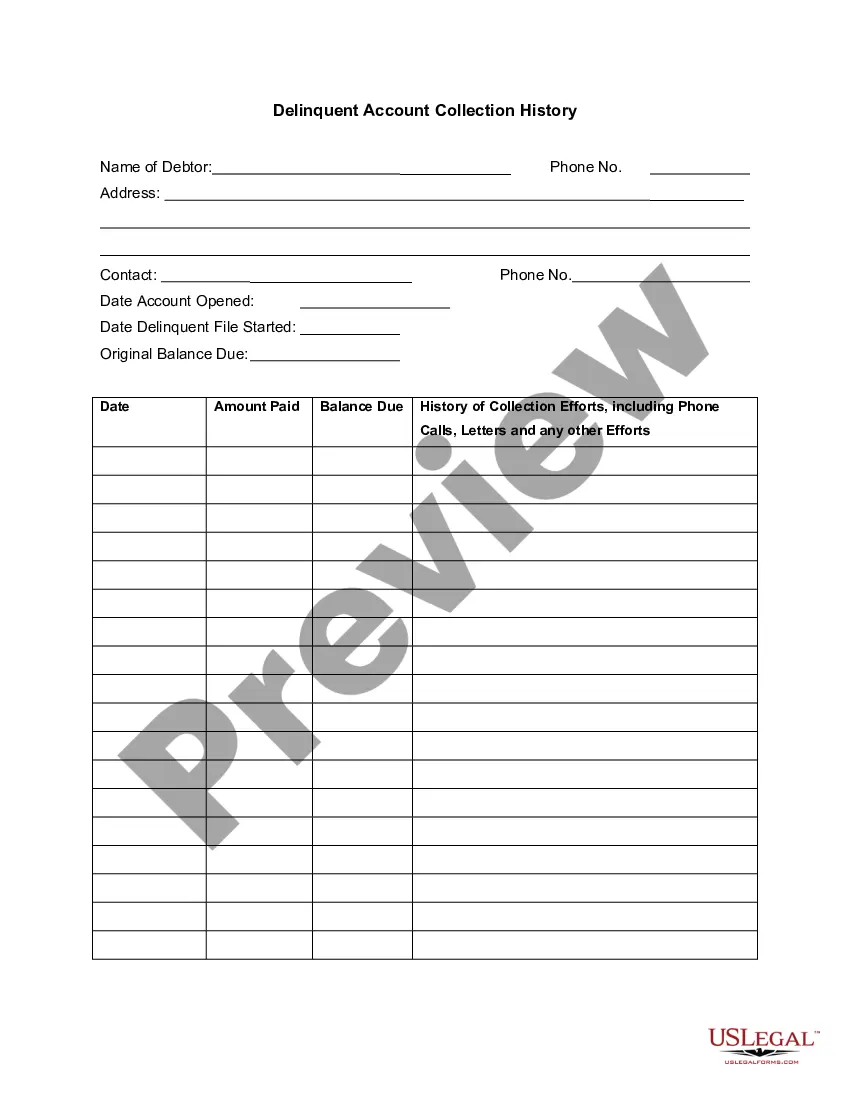

This is a form to track progress on a delinquent customer account and to record collection efforts.

Indiana Delinquent Account Collection History refers to the documentation and record keeping of past due accounts in the state of Indiana. When an account becomes delinquent, it means that the account holder has failed to make the required payments within the specified timeframe. The Indiana Delinquent Account Collection History tracks these delinquent accounts and provides a comprehensive overview of the collection efforts made by creditors or collection agencies. Keywords: Indiana, delinquent account, collection history, documentation, record keeping, past due accounts, account holder, payments, timeframe, creditors, collection agencies. There are various types of Indiana Delinquent Account Collection History, including: 1. Personal Loans: This category includes delinquent accounts related to personal loans taken by individuals for various purposes, such as education, medical expenses, or home improvements. 2. Credit Cards: Delinquent accounts associated with credit cards fall under this category. It includes individuals who have failed to pay their credit card bills within the specified time, resulting in a negative impact on their credit history. 3. Auto Loans: Delinquencies related to auto loans, where borrowers have fallen behind on their car loan payments, are recorded in this category. Failure to make timely payments could lead to repossession of the vehicle. 4. Mortgage Loans: Delinquencies in mortgage payments are significant as they can lead to foreclosure. This category includes accounts where homeowners are unable to make their monthly mortgage payments. 5. Student Loans: Delinquent accounts within the student loan category occur when borrowers are unable to make their scheduled loan payments, resulting in default. These accounts have unique collection procedures governed by federal regulations. 6. Utility Bills: Late payment or non-payment of utility bills, such as electricity, water, or gas, can lead to delinquent accounts. These often result in collection efforts by utility companies or third-party collection agencies. 7. Medical Bills: Unpaid medical bills can also result in delinquent accounts. Those who fail to pay their medical bills within the specified timeframe may face collection actions from healthcare providers or medical billing companies. 8. Commercial Loans: Delinquencies in commercial loans are relevant to businesses. When companies or organizations fail to repay their loans according to the agreed terms, their accounts become delinquent, leading to collection efforts. 9. Personal Lines of Credit: Delinquent accounts associated with personal lines of credit, where individuals have exceeded their credit limits or failed to make the required payments, are included in this category. It is important to note that the Indiana Delinquent Account Collection History serves as a crucial reference for creditors, lenders, and collection agencies to evaluate an individual or business's creditworthiness and risk when extending further credit or dealing with outstanding debts. It assists in determining appropriate collection strategies and potential legal actions to recover the overdue amounts.Indiana Delinquent Account Collection History refers to the documentation and record keeping of past due accounts in the state of Indiana. When an account becomes delinquent, it means that the account holder has failed to make the required payments within the specified timeframe. The Indiana Delinquent Account Collection History tracks these delinquent accounts and provides a comprehensive overview of the collection efforts made by creditors or collection agencies. Keywords: Indiana, delinquent account, collection history, documentation, record keeping, past due accounts, account holder, payments, timeframe, creditors, collection agencies. There are various types of Indiana Delinquent Account Collection History, including: 1. Personal Loans: This category includes delinquent accounts related to personal loans taken by individuals for various purposes, such as education, medical expenses, or home improvements. 2. Credit Cards: Delinquent accounts associated with credit cards fall under this category. It includes individuals who have failed to pay their credit card bills within the specified time, resulting in a negative impact on their credit history. 3. Auto Loans: Delinquencies related to auto loans, where borrowers have fallen behind on their car loan payments, are recorded in this category. Failure to make timely payments could lead to repossession of the vehicle. 4. Mortgage Loans: Delinquencies in mortgage payments are significant as they can lead to foreclosure. This category includes accounts where homeowners are unable to make their monthly mortgage payments. 5. Student Loans: Delinquent accounts within the student loan category occur when borrowers are unable to make their scheduled loan payments, resulting in default. These accounts have unique collection procedures governed by federal regulations. 6. Utility Bills: Late payment or non-payment of utility bills, such as electricity, water, or gas, can lead to delinquent accounts. These often result in collection efforts by utility companies or third-party collection agencies. 7. Medical Bills: Unpaid medical bills can also result in delinquent accounts. Those who fail to pay their medical bills within the specified timeframe may face collection actions from healthcare providers or medical billing companies. 8. Commercial Loans: Delinquencies in commercial loans are relevant to businesses. When companies or organizations fail to repay their loans according to the agreed terms, their accounts become delinquent, leading to collection efforts. 9. Personal Lines of Credit: Delinquent accounts associated with personal lines of credit, where individuals have exceeded their credit limits or failed to make the required payments, are included in this category. It is important to note that the Indiana Delinquent Account Collection History serves as a crucial reference for creditors, lenders, and collection agencies to evaluate an individual or business's creditworthiness and risk when extending further credit or dealing with outstanding debts. It assists in determining appropriate collection strategies and potential legal actions to recover the overdue amounts.