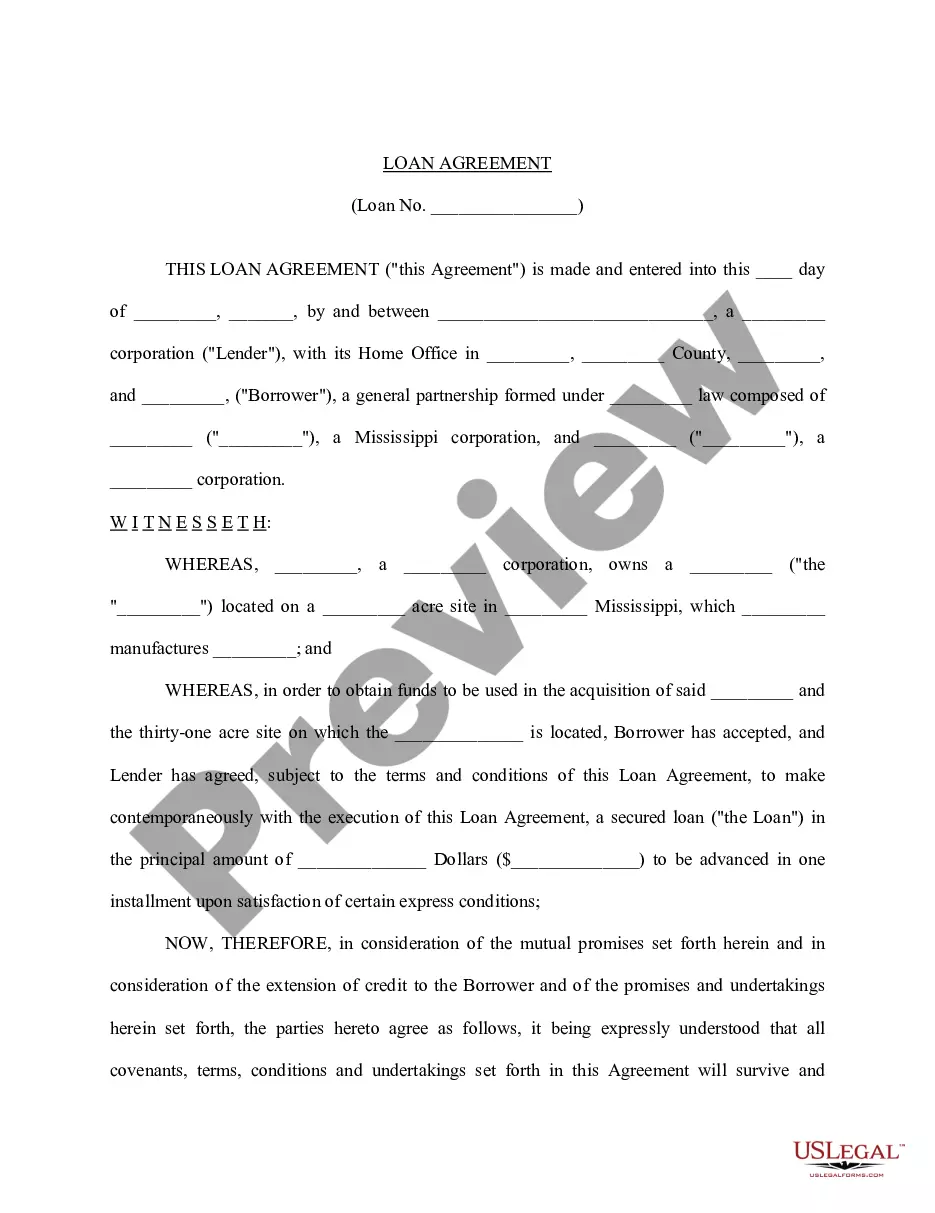

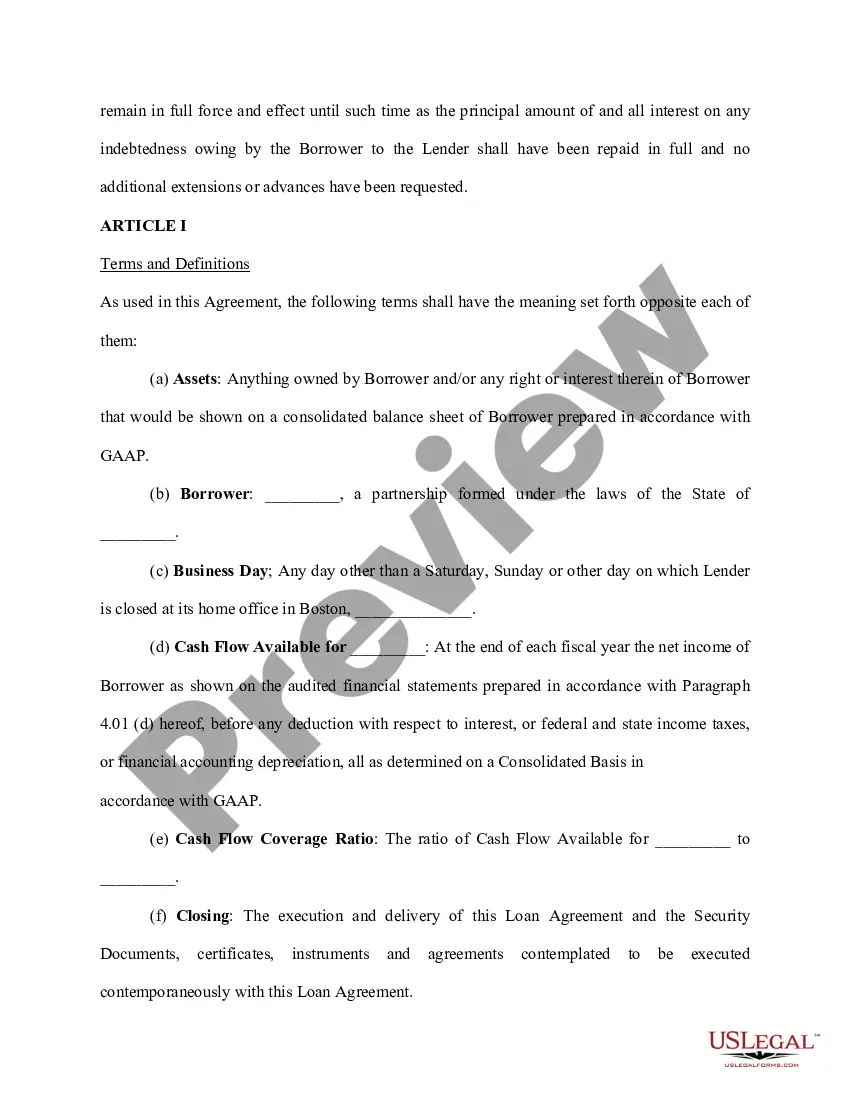

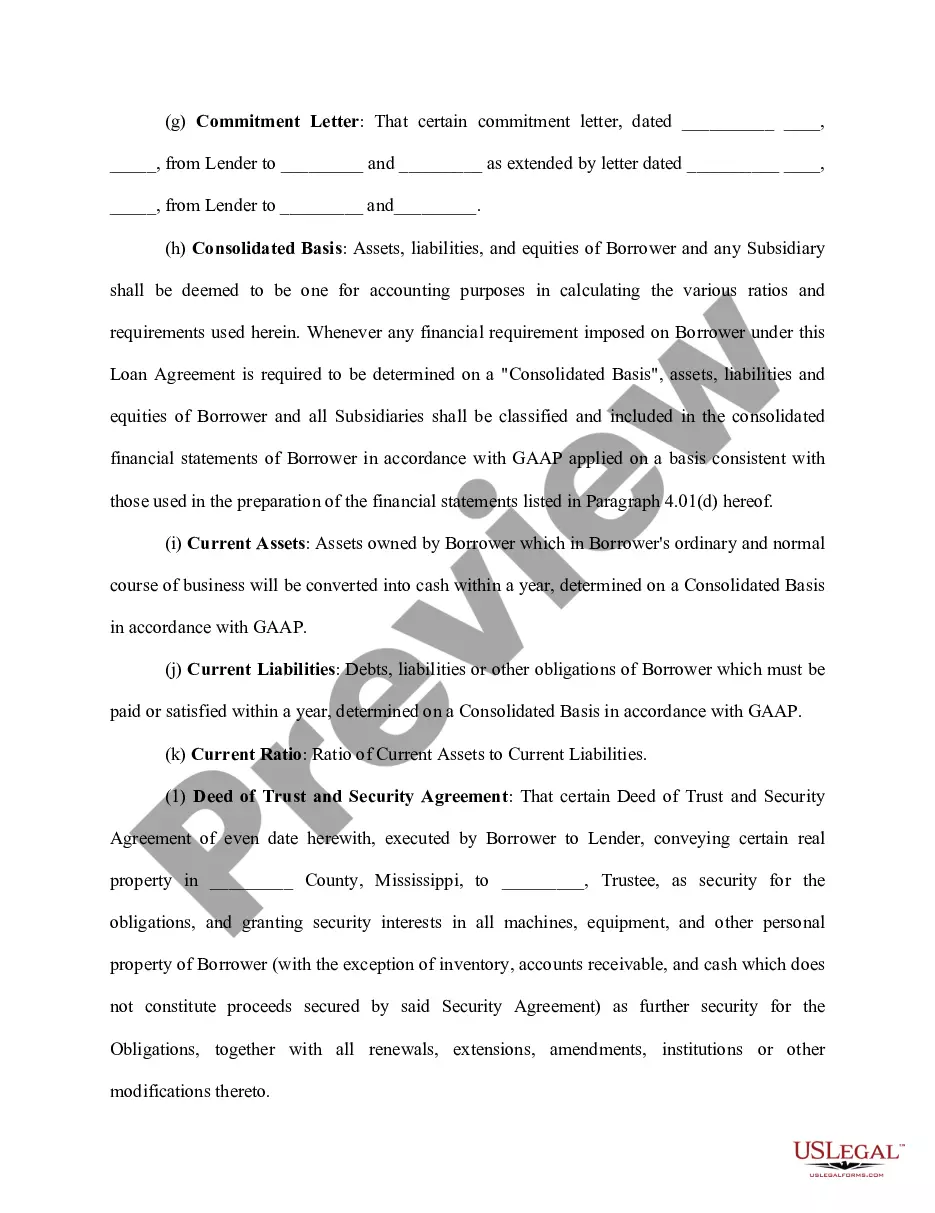

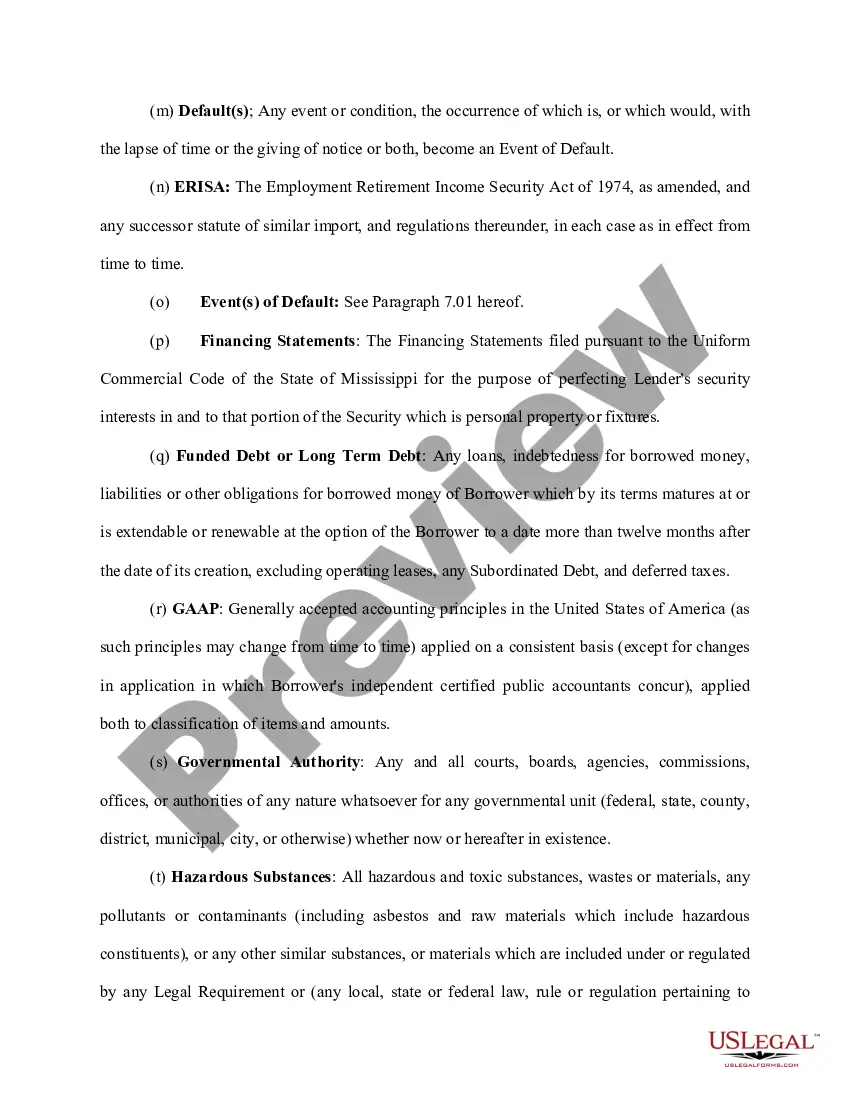

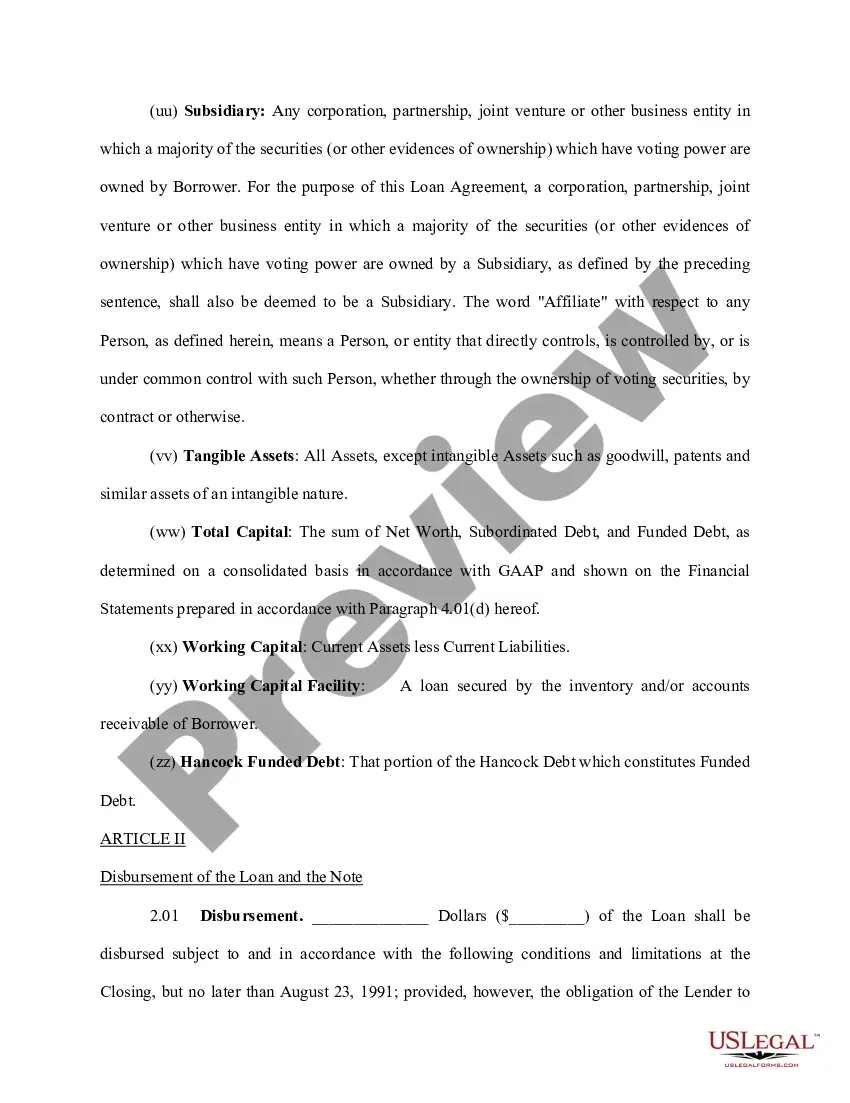

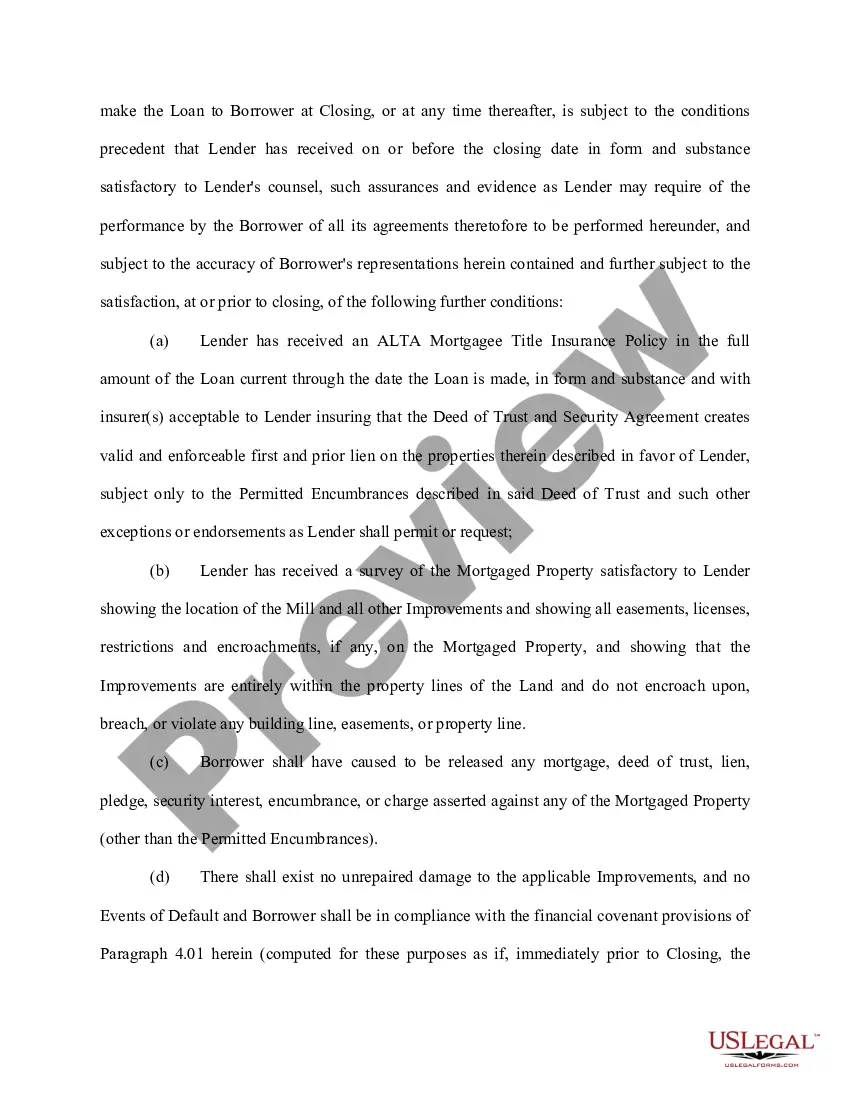

Indiana Loan Agreement for Employees is a legally binding document outlining the terms and conditions under which an employee can borrow funds from their employer. This agreement is designed to protect both the employer and the employee by clearly defining the loan terms and repayment obligations. The Indiana Loan Agreement for Employees typically includes the following key elements: loan amount, interest rate, repayment schedule, late payment fees, and any applicable penalties or provisions for early repayment. The agreement also specifies the purpose of the loan, whether it is for personal or business use. There are several types of Indiana Loan Agreements for Employees that may be offered by employers, depending on their individual policies and needs. These include: 1. Indiana Personal Loan Agreement for Employees: This type of agreement allows employees to borrow funds for personal use, such as debt consolidation, home improvement, or emergency expenses. 2. Indiana Education Loan Agreement for Employees: Employers may offer this type of agreement to help employees fund their education expenses, such as tuition fees, textbooks, or certification programs. 3. Indiana Relocation Loan Agreement for Employees: In cases where an employee needs to relocate for work purposes, employers may provide a loan to cover moving expenses, temporary accommodation costs, or other related expenses. 4. Indiana Home Loan Agreement for Employees: Some employers offer home loans to help employees with the down payment or closing costs when purchasing a new home. It is important to note that the specific terms and conditions of the Indiana Loan Agreement for Employees may vary depending on the employer's policies and the nature of the loan. Employees should carefully review the agreement and seek legal advice if needed before entering into any loan agreement. This ensures they fully understand their rights and responsibilities throughout the loan term.

Indiana Loan Agreement for Employees

Description

How to fill out Indiana Loan Agreement For Employees?

If you wish to complete, acquire, or print out lawful papers themes, use US Legal Forms, the biggest variety of lawful forms, which can be found on the Internet. Use the site`s easy and hassle-free lookup to obtain the papers you require. A variety of themes for company and personal purposes are sorted by classes and states, or keywords. Use US Legal Forms to obtain the Indiana Loan Agreement for Employees in just a handful of mouse clicks.

In case you are currently a US Legal Forms client, log in to your profile and click the Obtain switch to obtain the Indiana Loan Agreement for Employees. You may also access forms you in the past saved inside the My Forms tab of your own profile.

If you are using US Legal Forms initially, refer to the instructions beneath:

- Step 1. Be sure you have selected the form to the right area/region.

- Step 2. Make use of the Review method to look through the form`s content material. Don`t neglect to read the description.

- Step 3. In case you are unhappy together with the kind, take advantage of the Look for discipline towards the top of the screen to discover other versions in the lawful kind format.

- Step 4. After you have identified the form you require, go through the Get now switch. Opt for the prices strategy you choose and add your qualifications to register for the profile.

- Step 5. Approach the transaction. You can utilize your charge card or PayPal profile to accomplish the transaction.

- Step 6. Choose the file format in the lawful kind and acquire it in your product.

- Step 7. Comprehensive, revise and print out or sign the Indiana Loan Agreement for Employees.

Every single lawful papers format you purchase is your own eternally. You may have acces to every kind you saved in your acccount. Go through the My Forms area and pick a kind to print out or acquire yet again.

Contend and acquire, and print out the Indiana Loan Agreement for Employees with US Legal Forms. There are millions of skilled and status-particular forms you may use for your company or personal requirements.

Form popularity

FAQ

For a personal loan agreement to be enforceable, it must be documented in writing, as well as signed and dated by all parties involved. It's also a good idea to have the document notarized or signed by a witness.

Loan agreements typically include covenants, value of collateral involved, guarantees, interest rate terms and the duration over which it must be repaid.

There are 10 basic provisions that should be in a loan agreement. Identity of the parties. The names of the lender and borrower need to be stated. ... Date of the agreement. ... Interest rate. ... Repayment terms. ... Default provisions. ... Signatures. ... Choice of law. ... Severability.

What a personal loan agreement should include Legal names and address of both parties. Names and address of the loan cosigner (if applicable). Amount to be borrowed. Date the loan is to be provided. Repayment date. Interest rate to be charged (if applicable). Annual percentage rate (if applicable).

First and foremost, understand that personal loan agreements fall into the classification of contracts. Technically, you don't have to notarize these documents. But if you want to make this document legally binding, then notarization is the best course of action.

What should be in a personal loan contract? Names and addresses of the lender and the borrower. Information about the loan co-borrower or cosigner, if it's a joint personal loan. Loan amount and the method for disbursement (lump sum, installments, etc.) Date the loan was provided. Expected repayment date.