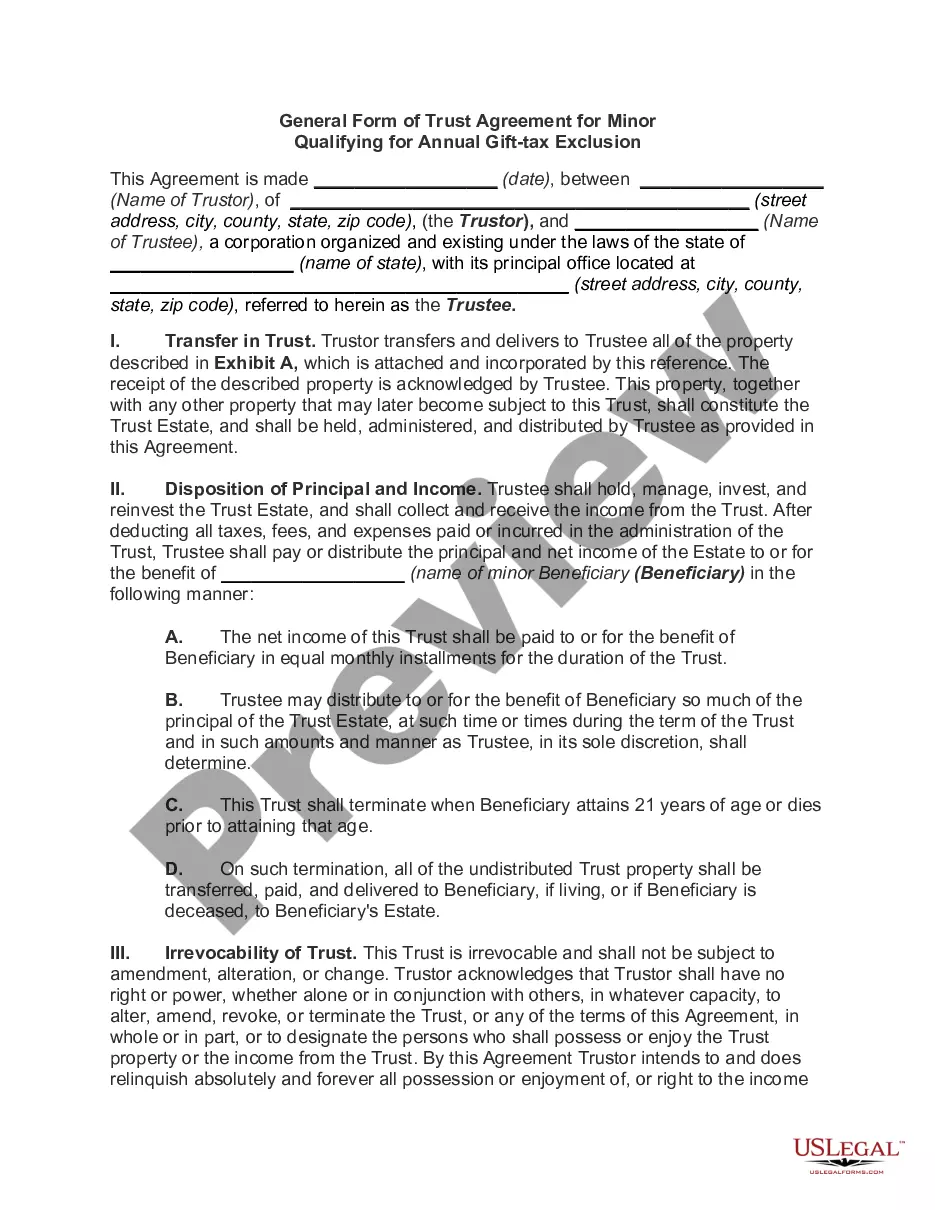

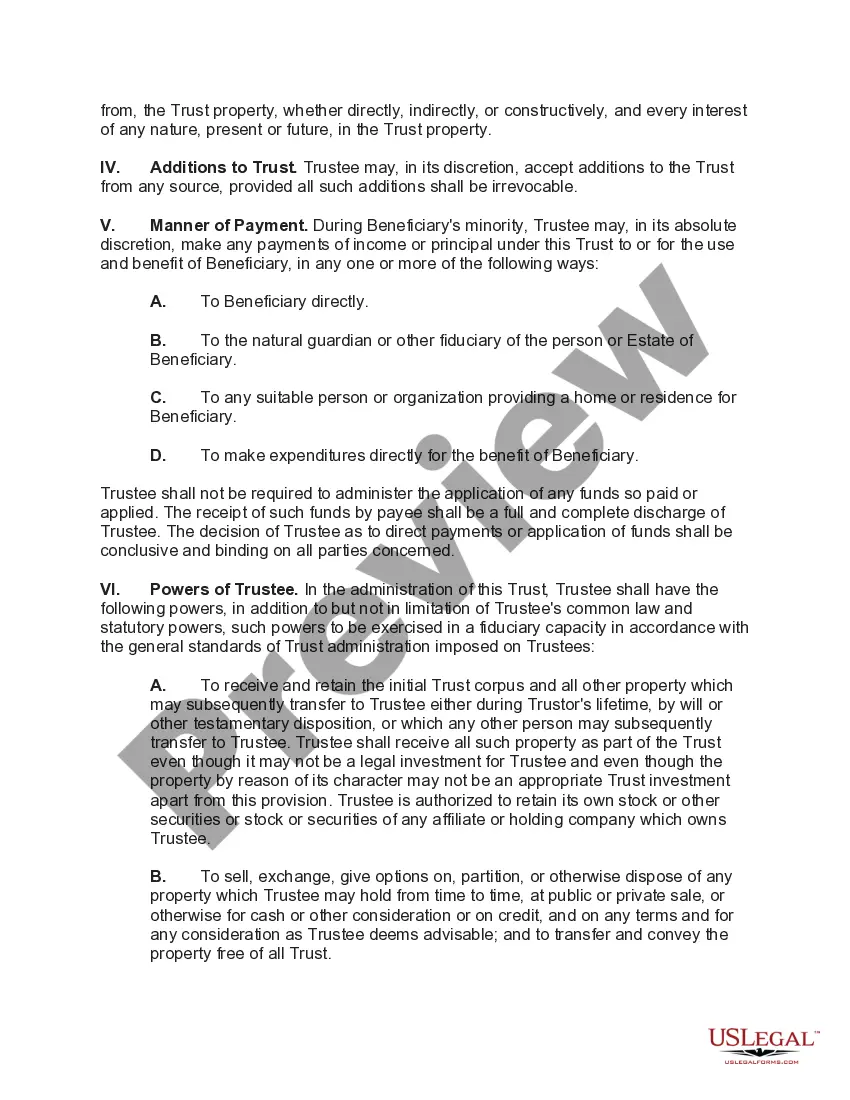

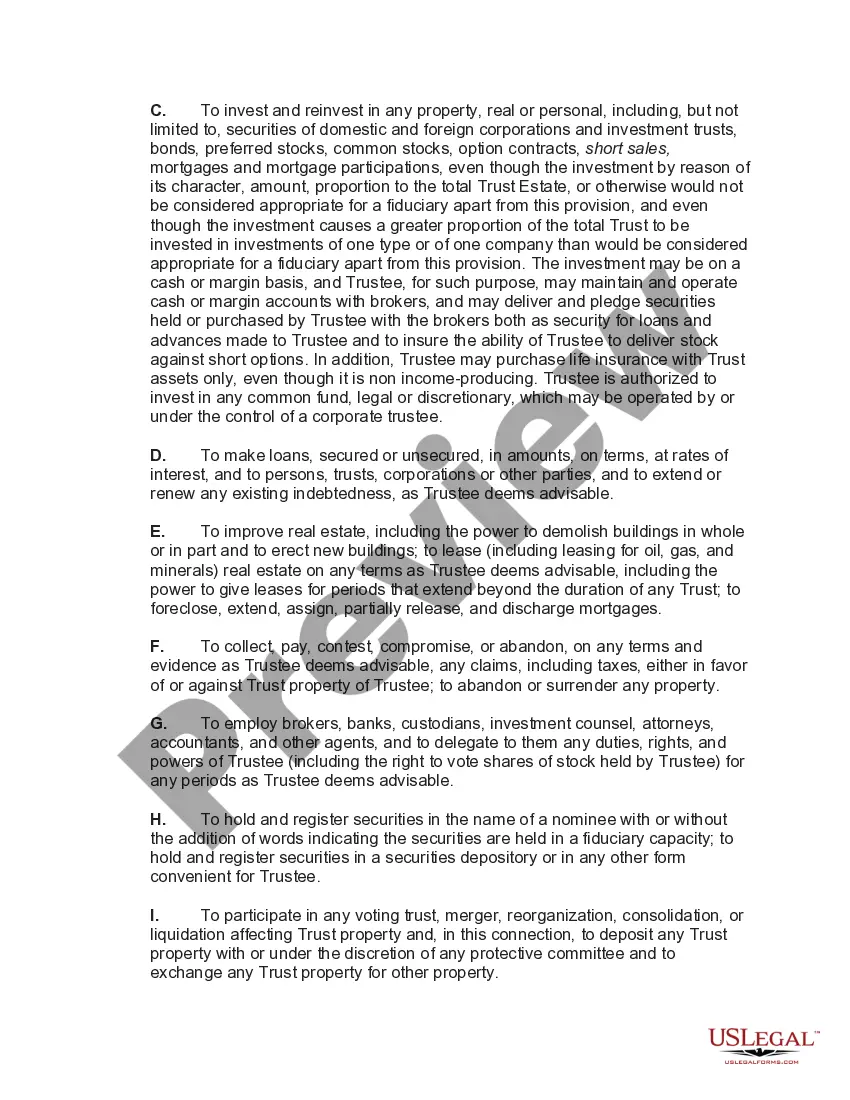

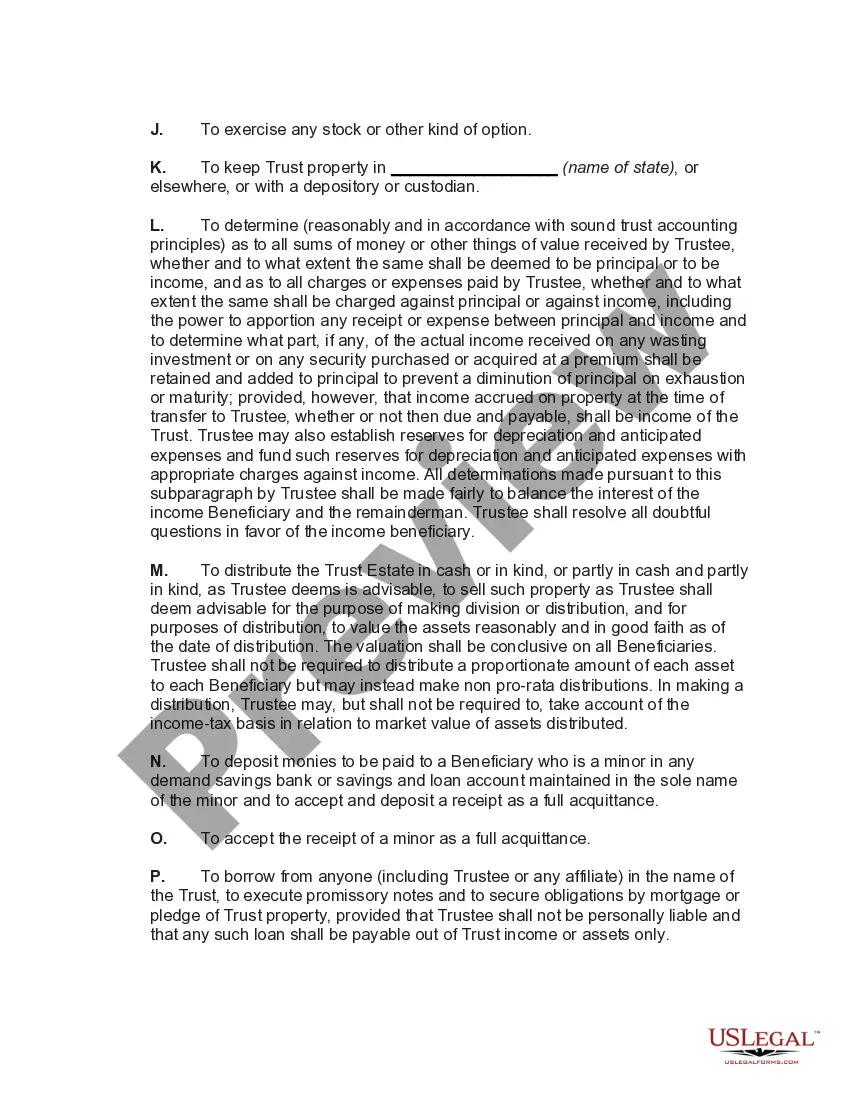

The Indiana General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion is a legal document that allows individuals to create a trust for a minor, while taking advantage of the annual gift tax exclusion provided by the Internal Revenue Service (IRS). This agreement helps in establishing a legally binding arrangement that ensures the proper management and distribution of assets to benefit the minor. In Indiana, there are several types of General Form of Trust Agreements for Minor Qualifying for Annual Gift Tax Exclusion that can be used depending on the specific needs and preferences of the granter. Some common variations include: 1. Revocable Trust Agreement: This type of trust allows the granter to have full control and authority over the assets placed in the trust. The granter retains the right to modify or terminate the trust during their lifetime, providing them with flexibility in managing the trust for the benefit of the minor. 2. Irrevocable Trust Agreement: An irrevocable trust, on the other hand, cannot be modified or revoked once it is established. This type of trust provides more asset protection, as the assets no longer belong to the granter and are shielded from creditors or legal claims. However, this also means that the granter gives up control over the assets. 3. Testamentary Trust Agreement: This form of trust is created in a last will and testament, and only goes into effect upon the death of the granter. It allows the granter to specify how the assets should be managed and distributed for the benefit of the minor after their passing. The Indiana General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion typically includes key components such as the identification of the granter, trustee, and minor beneficiary. It also outlines the purpose of the trust, which is usually to provide for the minor's financial needs, including education, healthcare, and general support. The agreement also details the assets that will be placed in the trust, their valuation, and any specific instructions on how they should be managed, invested, or distributed. To qualify for the annual gift tax exclusion, the trust agreement must comply with the IRS regulations, which currently allow for a gift tax exclusion amount up to a certain limit. This limit is subject to change and should be verified with the most recent IRS guidelines. It is crucial to consult with a qualified attorney or legal professional when creating an Indiana General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion to ensure compliance with state laws and regulations. The attorney can provide guidance on selecting the appropriate type of trust agreement and assist in drafting a comprehensive and tailored document that meets the specific needs and goals of the granter.

Indiana General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion

Description

How to fill out Indiana General Form Of Trust Agreement For Minor Qualifying For Annual Gift Tax Exclusion?

Choosing the right legal file design could be a battle. Needless to say, there are a lot of themes accessible on the Internet, but how do you discover the legal type you need? Utilize the US Legal Forms site. The service delivers 1000s of themes, such as the Indiana General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion, which you can use for organization and private needs. Each of the kinds are examined by experts and meet federal and state needs.

When you are already listed, log in to your profile and click on the Obtain switch to have the Indiana General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion. Make use of your profile to look throughout the legal kinds you possess bought formerly. Visit the My Forms tab of your respective profile and have one more duplicate from the file you need.

When you are a brand new end user of US Legal Forms, listed below are simple directions for you to comply with:

- Initially, make sure you have selected the proper type for the metropolis/state. You can look over the shape utilizing the Preview switch and read the shape information to guarantee this is the best for you.

- When the type fails to meet your requirements, make use of the Seach industry to obtain the right type.

- Once you are sure that the shape is proper, click the Purchase now switch to have the type.

- Pick the costs prepare you need and enter the required details. Create your profile and pay for an order using your PayPal profile or credit card.

- Opt for the data file structure and acquire the legal file design to your system.

- Total, change and printing and sign the obtained Indiana General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion.

US Legal Forms will be the greatest local library of legal kinds where you can see a variety of file themes. Utilize the company to acquire skillfully-made files that comply with express needs.