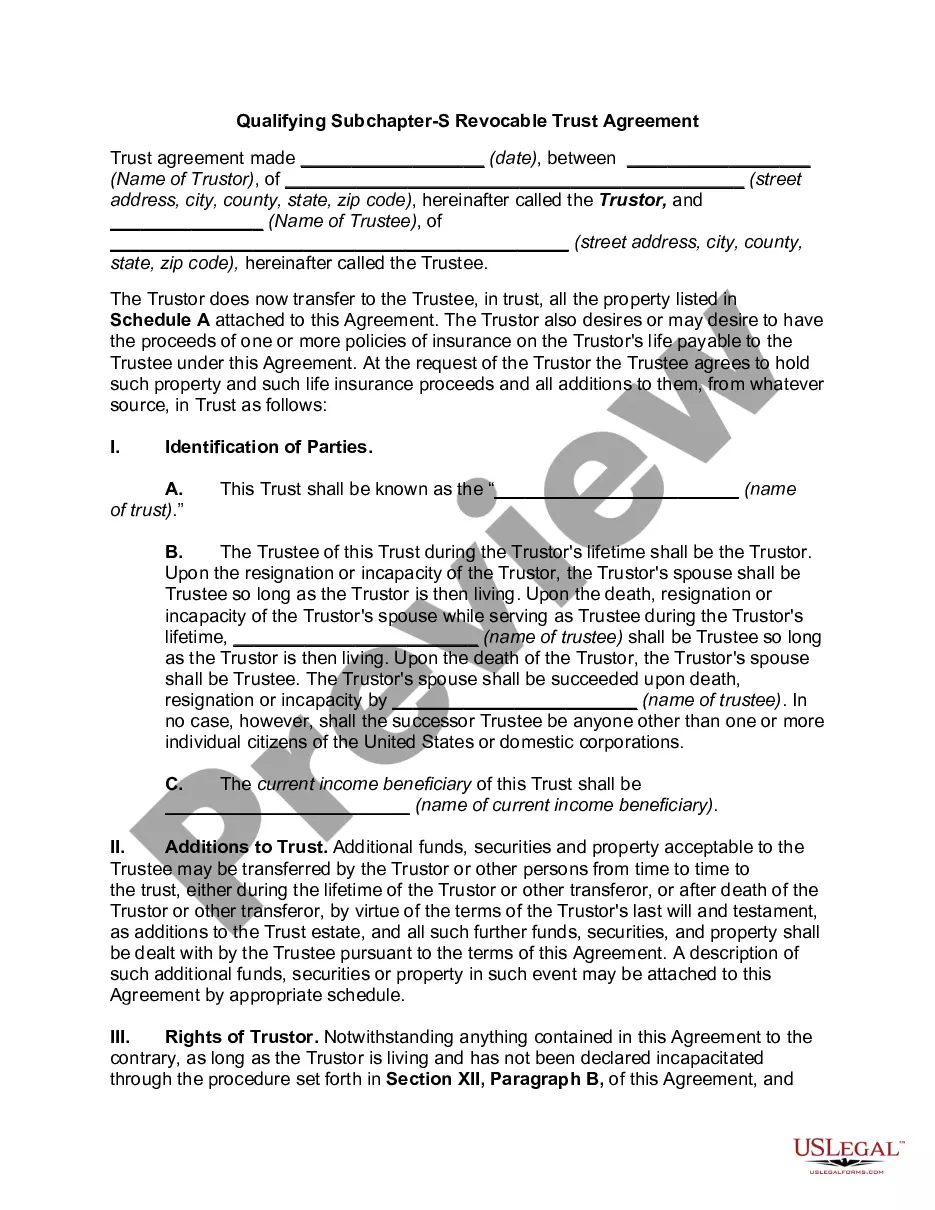

An Indiana Qualifying Subchapter-S Revocable Trust Agreement is a legal document that establishes a trust in the state of Indiana, utilizing the specific provisions of Subchapter S of the Internal Revenue Code. This type of trust is primarily formed for tax planning purposes and allows for certain tax advantages. A Subchapter S Revocable Trust Agreement is designed to meet the requirements and qualifications set forth in the Internal Revenue Code for Subchapter S corporations. By employing this structure within a trust, the income, deductions, and tax liabilities of the trust can pass through to the trust beneficiaries, reducing the overall tax burden. These types of trusts are commonly used for estate planning purposes, as they offer flexibility and tax efficiency. The creator of the trust, known as the granter or settler, can establish provisions to ensure the orderly transfer of assets and distribution of income to beneficiaries upon their death or incapacity. Within the realm of Indiana Qualifying Subchapter-S Revocable Trust Agreements, there can be different variations or specific types tailored to the individual needs and circumstances of the granter. Some common examples include: 1. Indiana Qualifying Subchapter-S Revocable Living Trust: This type of trust becomes effective during the granter's lifetime and allows for the management and distribution of assets while also providing the benefits of a Subchapter S corporation. 2. Indiana Qualifying Subchapter-S Revocable Testamentary Trust: Unlike a living trust, this type of trust is established through a will and becomes effective after the granter's death. It can include specific provisions to address the transfer of assets to Subchapter S entities or take advantage of the trust's tax benefits. 3. Indiana Qualifying Subchapter-S Revocable Charitable Remainder Trust: A variation of the trust that incorporates charitable giving, allowing for the granter to transfer assets while retaining an income interest for a specified period. This type of trust not only benefits the granter but also supports charitable causes. In conclusion, an Indiana Qualifying Subchapter-S Revocable Trust Agreement is a specialized legal document that utilizes the provisions of Subchapter S within the Internal Revenue Code to establish a flexible and tax-efficient trust structure. By employing this type of trust, individuals can effectively plan for the management, transfer, and tax consequences of their assets. The various types of Indiana Qualifying Subchapter-S Revocable Trust Agreements can be tailored to suit specific needs, ensuring the intended outcomes are achieved.

Indiana Qualifying Subchapter-S Revocable Trust Agreement

Description

How to fill out Indiana Qualifying Subchapter-S Revocable Trust Agreement?

Choosing the best lawful document format can be quite a struggle. Of course, there are tons of templates available online, but how can you get the lawful kind you require? Utilize the US Legal Forms internet site. The services gives a huge number of templates, for example the Indiana Qualifying Subchapter-S Revocable Trust Agreement, which can be used for organization and personal requires. All the varieties are examined by professionals and meet up with federal and state demands.

Should you be presently listed, log in in your accounts and then click the Download key to get the Indiana Qualifying Subchapter-S Revocable Trust Agreement. Make use of accounts to appear through the lawful varieties you have bought earlier. Proceed to the My Forms tab of the accounts and get one more duplicate of your document you require.

Should you be a fresh consumer of US Legal Forms, here are straightforward recommendations that you can stick to:

- Very first, ensure you have chosen the correct kind for your personal town/county. You may examine the shape while using Review key and browse the shape outline to guarantee this is the best for you.

- In case the kind fails to meet up with your expectations, use the Seach field to obtain the correct kind.

- When you are positive that the shape is suitable, click the Acquire now key to get the kind.

- Opt for the prices plan you want and enter in the needed information and facts. Design your accounts and buy an order making use of your PayPal accounts or Visa or Mastercard.

- Choose the file file format and acquire the lawful document format in your product.

- Full, change and print out and indication the attained Indiana Qualifying Subchapter-S Revocable Trust Agreement.

US Legal Forms may be the greatest library of lawful varieties where you can find numerous document templates. Utilize the company to acquire professionally-produced files that stick to express demands.

Form popularity

FAQ

Yes, the IRS allows the estate of a deceased shareholder to be an S-Corporation shareholder. Note the language deceased shareholder. This indicates, correctly, that an estate can step in and become an S-Corp shareholder when a typical shareholder dies.

Types of Trusts Permitted as Shareholders of an S Corporation. Only certain kinds of trusts can be S corporation owners. The trust needs to be a U.S.-based trust under one of the following classifications: Grantor Sub-part E.

The main difference between an ESBT and a QSST is that an ESBT may have multiple income beneficiaries, and the trust does not have to distribute all income. Unlike with the QSST, the trustee, rather than the beneficiary, must make the election.

TRUSTS COMMONLY USED TO HOLD S CORPORATION STOCK Three commonly used types of ongoing trusts qualify as S corporation shareholders: grantor trusts, qualified subchapter S trusts (QSSTs) and electing small business trusts (ESBTs).

To obtain relief, the trustee of an ESBT or the current income beneficiary of a QSST must sign and file the appropriate election form, which must include the following statements: A statement from the trustee of the ESBT or the current income beneficiary of the QSST that includes the information required by Regs.

A trust can hold stock in an S corp only if it (1) is treated as owned by its grantor for income tax purposes under us grantor trust rules, (2) was a grantor trust immediately before its grantor's death (the trust can be a shareholder only for two years from that date), (3) received stock from the will of a decedent (

The main difference between an ESBT and a QSST is that an ESBT may have multiple income beneficiaries, and the trust does not have to distribute all income. Unlike with the QSST, the trustee, rather than the beneficiary, must make the election.

A Qualified Subchapter S Trust, commonly referred to as a QSST Election, or a Q-Sub election, is a Qualified Subchapter S Subsidiary Election made on behalf of a trust that retains ownership as the shareholder of an S corporation, a corporation in the United States which votes to be taxed.

Since a revocable trust is not treated as separate from the grantor, it is an eligible S corporation shareholder while the grantor is alive.

Net investment income tax of a QSST 1411(a)(2)). The tax also applies to QSSTs to the extent the net investment income is retained in the trust. Although the S corporation income of a QSST is taxed to the individual income beneficiary, capital gain on the sale of the S corporation stock is taxed at the trust level.