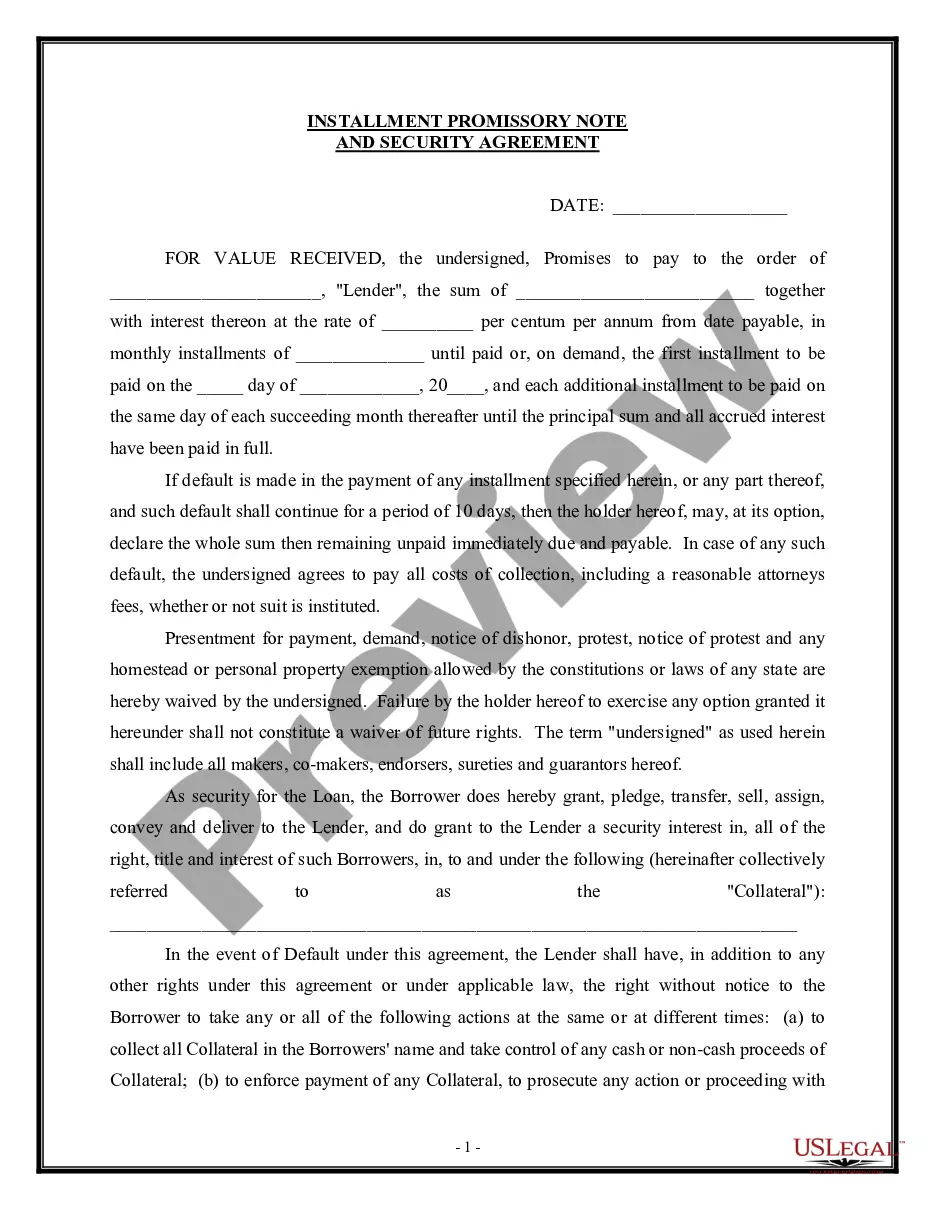

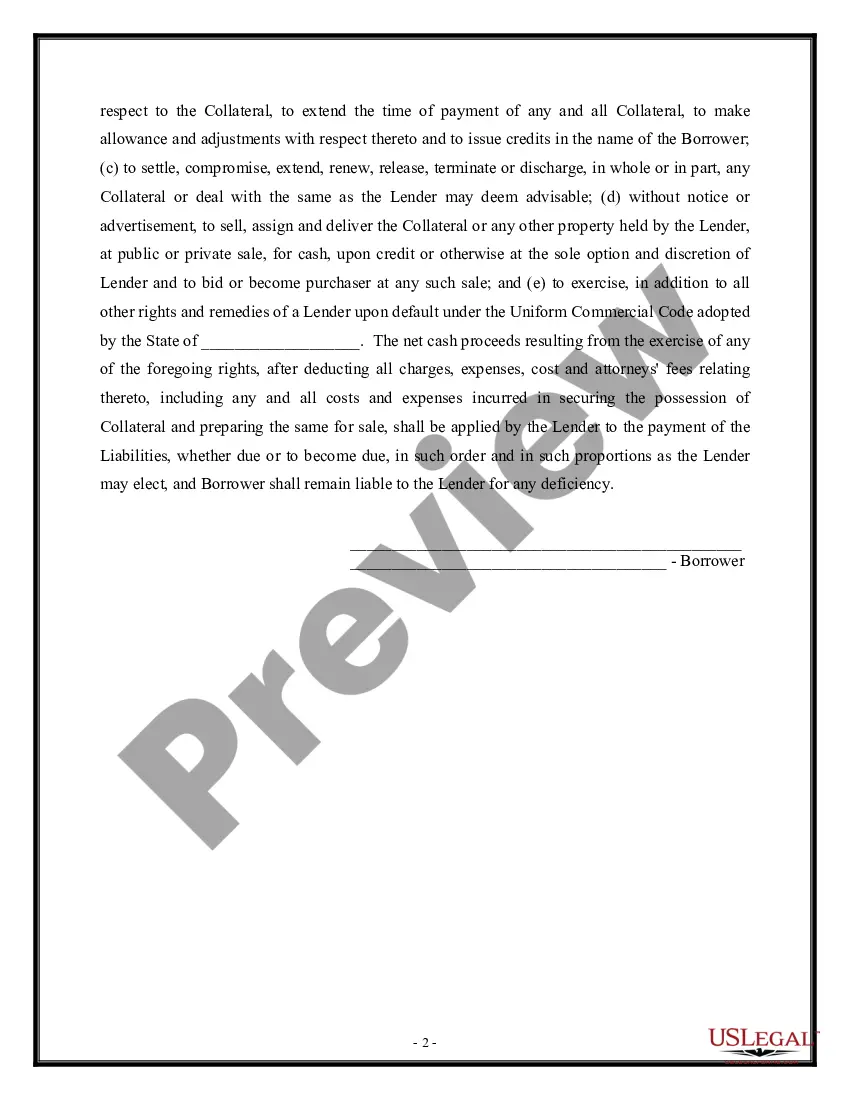

Indiana Installment Promissory Note and Security Agreement is a legal document that outlines the terms and conditions of a loan agreement between a lender and a borrower in Indiana. This agreement serves as a written record of the loan, ensuring that both parties are aware of their rights and obligations. The Indiana Installment Promissory Note and Security Agreement specifies the principal amount of the loan, the interest rate charged, the repayment schedule, and any other specific terms that both parties have agreed upon. It also includes provisions to protect the lender's interests by providing collateral in the form of security agreement. In Indiana, there are different types of Installment Promissory Note and Security Agreements, depending on the nature of the loan and the specific requirements of the parties involved. Some common variations include secured and unsecured installment promissory notes. A secured installment promissory note requires the borrower to provide collateral, such as real estate, vehicles, or other valuable assets, as security against the loan. The collateral serves as a guarantee to the lender that, in the event of default, they have the right to seize and sell the secured property to recover the outstanding loan amount. On the other hand, an unsecured installment promissory note does not require collateral as security. This type of agreement relies solely on the borrower's promise to repay the loan according to the agreed terms. In an unsecured note, the lender may have fewer options to recover their money if the borrower defaults. Whether secured or unsecured, an Indiana Installment Promissory Note and Security Agreement serves as a legally binding contract between the lender and borrower. It is recommended that both parties carefully review and understand the terms before signing, and seek legal advice if necessary to ensure compliance with Indiana state laws and regulations. In conclusion, the Indiana Installment Promissory Note and Security Agreement is a crucial document in loan transactions within the state. Its purpose is to establish clear terms and obligations for both the borrower and lender while safeguarding the lender's interests. By using this agreement, parties can ensure a transparent and fair lending process while complying with Indiana laws.

Indiana Installment Promissory Note and Security Agreement

Description

How to fill out Indiana Installment Promissory Note And Security Agreement?

You may spend hrs on-line trying to find the legitimate document design that fits the federal and state specifications you will need. US Legal Forms gives 1000s of legitimate varieties that happen to be examined by pros. It is possible to download or print out the Indiana Installment Promissory Note and Security Agreement from our service.

If you already possess a US Legal Forms account, you may log in and then click the Download key. Following that, you may total, edit, print out, or indicator the Indiana Installment Promissory Note and Security Agreement. Each legitimate document design you get is the one you have for a long time. To obtain one more duplicate of the purchased develop, check out the My Forms tab and then click the related key.

If you use the US Legal Forms internet site initially, stick to the simple recommendations under:

- Initially, be sure that you have selected the right document design to the area/metropolis that you pick. Read the develop outline to ensure you have picked out the proper develop. If readily available, use the Preview key to look throughout the document design at the same time.

- If you want to locate one more model of the develop, use the Search field to find the design that fits your needs and specifications.

- When you have discovered the design you would like, simply click Get now to continue.

- Pick the costs prepare you would like, type your accreditations, and sign up for a merchant account on US Legal Forms.

- Total the purchase. You may use your charge card or PayPal account to cover the legitimate develop.

- Pick the structure of the document and download it to your product.

- Make alterations to your document if needed. You may total, edit and indicator and print out Indiana Installment Promissory Note and Security Agreement.

Download and print out 1000s of document layouts using the US Legal Forms Internet site, which offers the most important assortment of legitimate varieties. Use professional and status-certain layouts to take on your company or person requirements.