Indiana Breakdown of Savings for Budget and Emergency Fund

Description

How to fill out Breakdown Of Savings For Budget And Emergency Fund?

Finding the appropriate legal document format can be quite a challenge.

Clearly, there are numerous templates available online, but how will you acquire the legal form you require.

Utilize the US Legal Forms website. The platform offers a vast selection of templates, including the Indiana Summary of Savings for Budget and Emergency Fund, which can be utilized for both business and personal needs.

You can preview the document using the Review button and read the form description to ensure it is suitable for you.

- All templates are reviewed by professionals and comply with federal and state regulations.

- If you are already registered, sign in to your account and click the Download button to obtain the Indiana Summary of Savings for Budget and Emergency Fund.

- Use your account to review the legal templates you have previously purchased.

- Go to the My documents section of your account and download another copy of the document you need.

- If you are a new user of US Legal Forms, here are straightforward instructions to follow.

- First, make sure you have chosen the correct form for your location/state.

Form popularity

FAQ

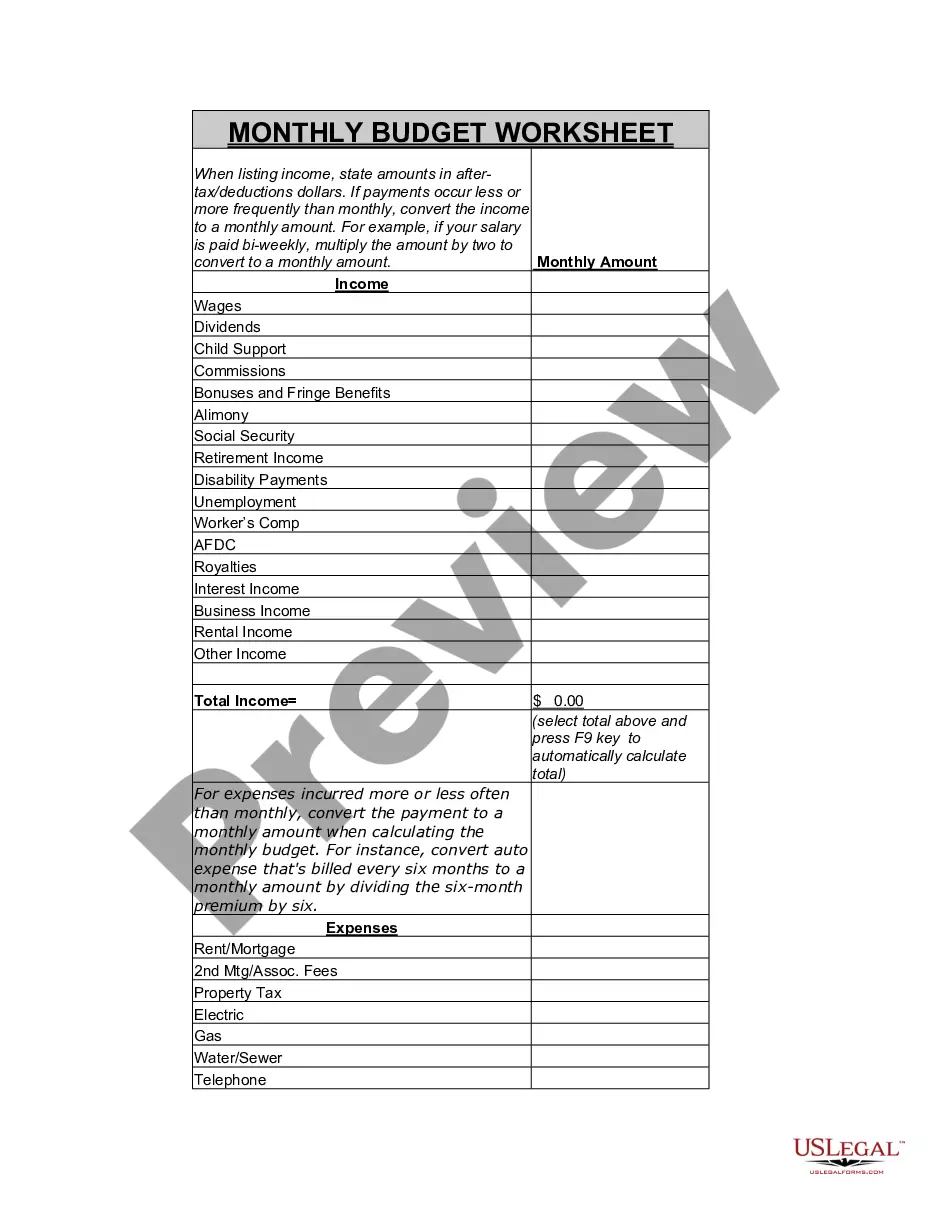

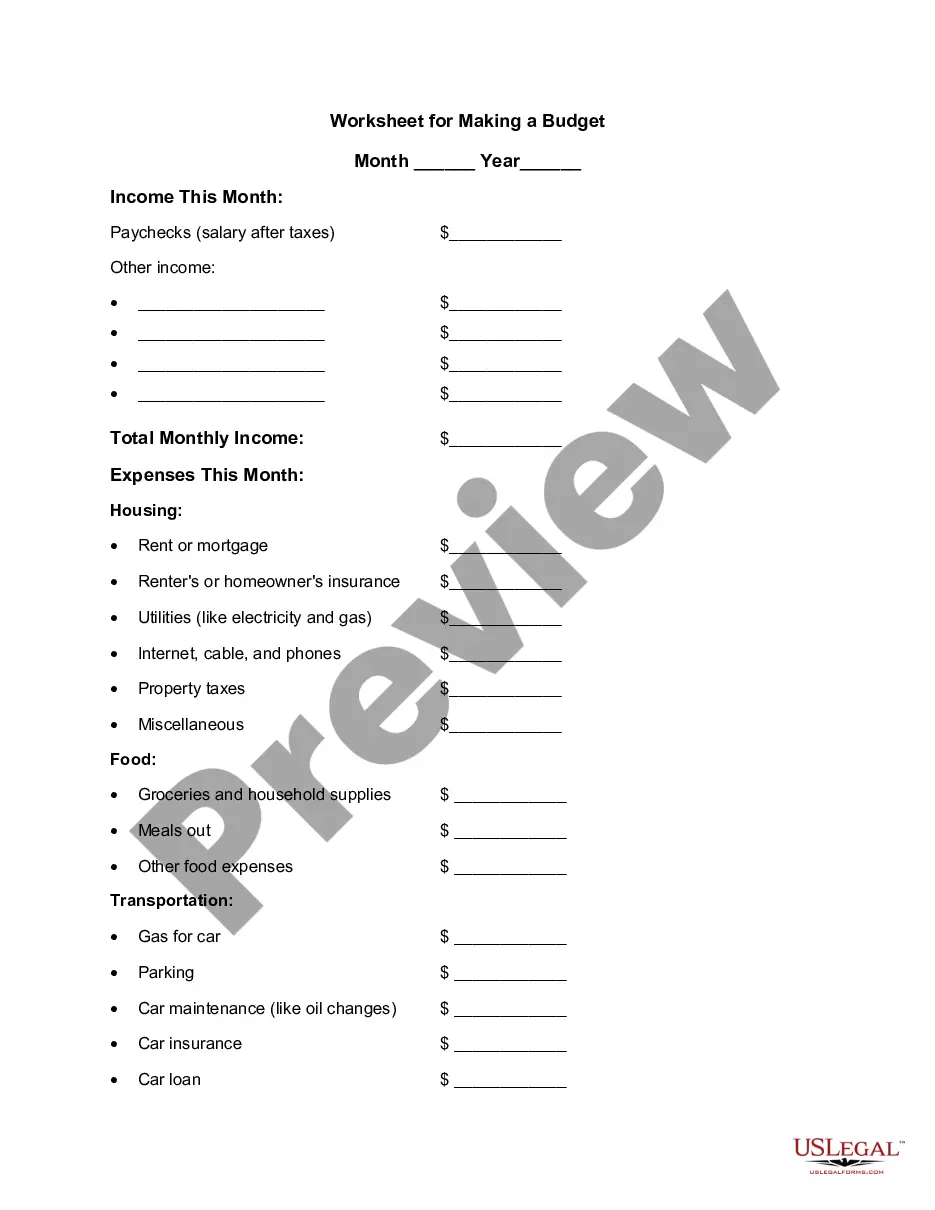

An emergency fund is necessary for peace of mind and smoothing out financial bumps in the road. Let's look at the average emergency fund size by age and how much we should have. According to Federal Reserve data, the average savings amount is $8,863 in America as of 2019.

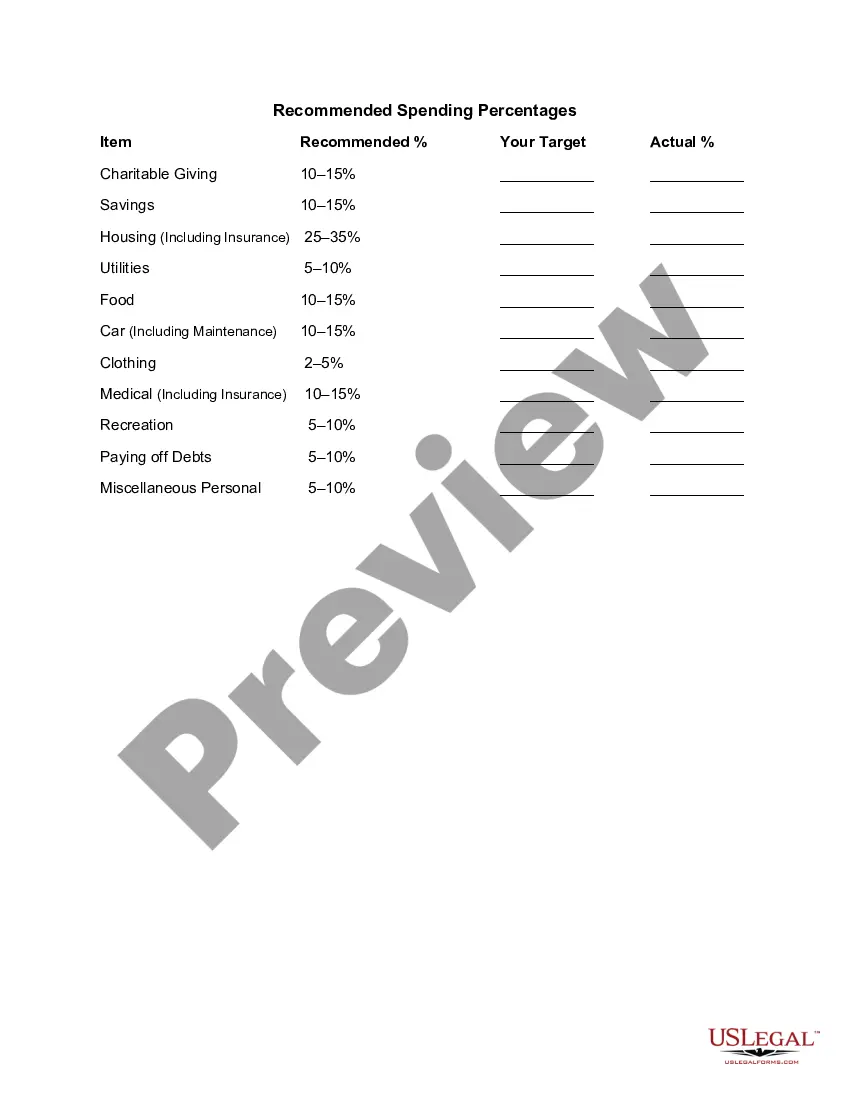

Senator Elizabeth Warren popularized the so-called "50/20/30 budget rule" (sometimes labeled "50-30-20") in her book, All Your Worth: The Ultimate Lifetime Money Plan. The basic rule is to divide up after-tax income and allocate it to spend: 50% on needs, 30% on wants, and socking away 20% to savings.

It's all about your personal expenses Those include things like rent or mortgage payments, utilities, healthcare expenses, and food. If your monthly essentials come to $2,500 a month, and you're comfortable with a four-month emergency fund, then you should be set with a $10,000 savings account balance.

While the size of your emergency fund will vary depending on your lifestyle, monthly costs, income, and dependents, the rule of thumb is to put away at least three to six months' worth of expenses.

Our 50/30/20 calculator divides your take-home income into suggested spending in three categories: 50% of net pay for needs, 30% for wants and 20% for savings and debt repayment.

Senator Elizabeth Warren popularized the so-called "50/20/30 budget rule" (sometimes labeled "50-30-20") in her book, All Your Worth: The Ultimate Lifetime Money Plan. The basic rule is to divide up after-tax income and allocate it to spend: 50% on needs, 30% on wants, and socking away 20% to savings.

70% is for monthly expenses (anything you spend money on). 20% goes into savings, unless you have pressing debt (see below for my definition), in which case it goes toward debt first. 10% goes to donation/tithing, or investments, retirement, saving for college, etc.

While the size of your emergency fund will vary depending on your lifestyle, monthly costs, income, and dependents, the rule of thumb is to put away at least three to six months' worth of expenses.

The short answer is that you should save a minimum of 20 percent of your income. At least 10 percent to 15 percent of that should go toward your retirement accounts. The other 5 to 10 percent of that should go toward a combination of building an emergency fund, creating other long-term savings, and paying down debt.

Most experts recommend keeping three to six months' worth of expenses in an emergency fund, but some situations warrant more. Some experts recommend a smaller emergency fund while you're paying off debt. If your job is secure and you don't have a lot of expenses, you may be able to save less.