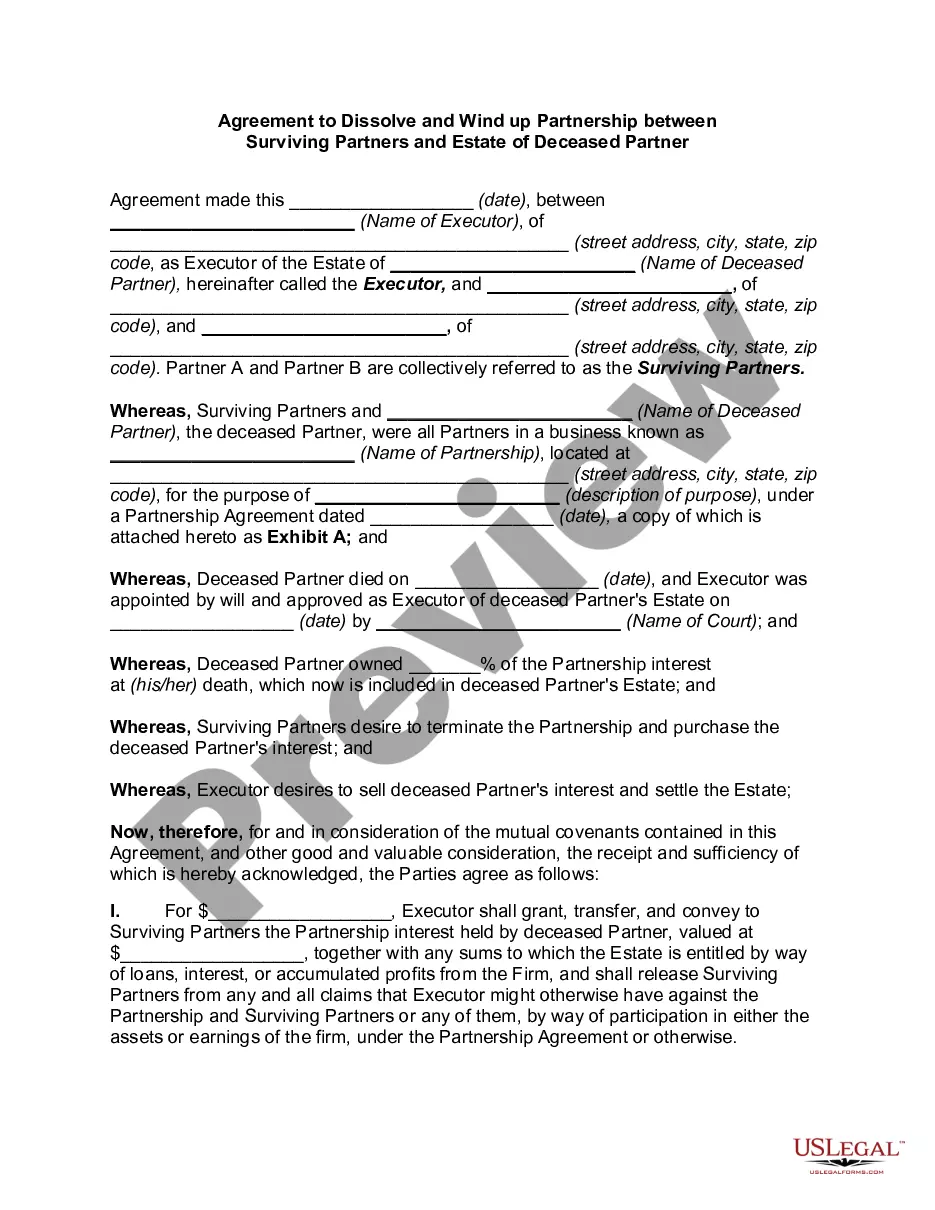

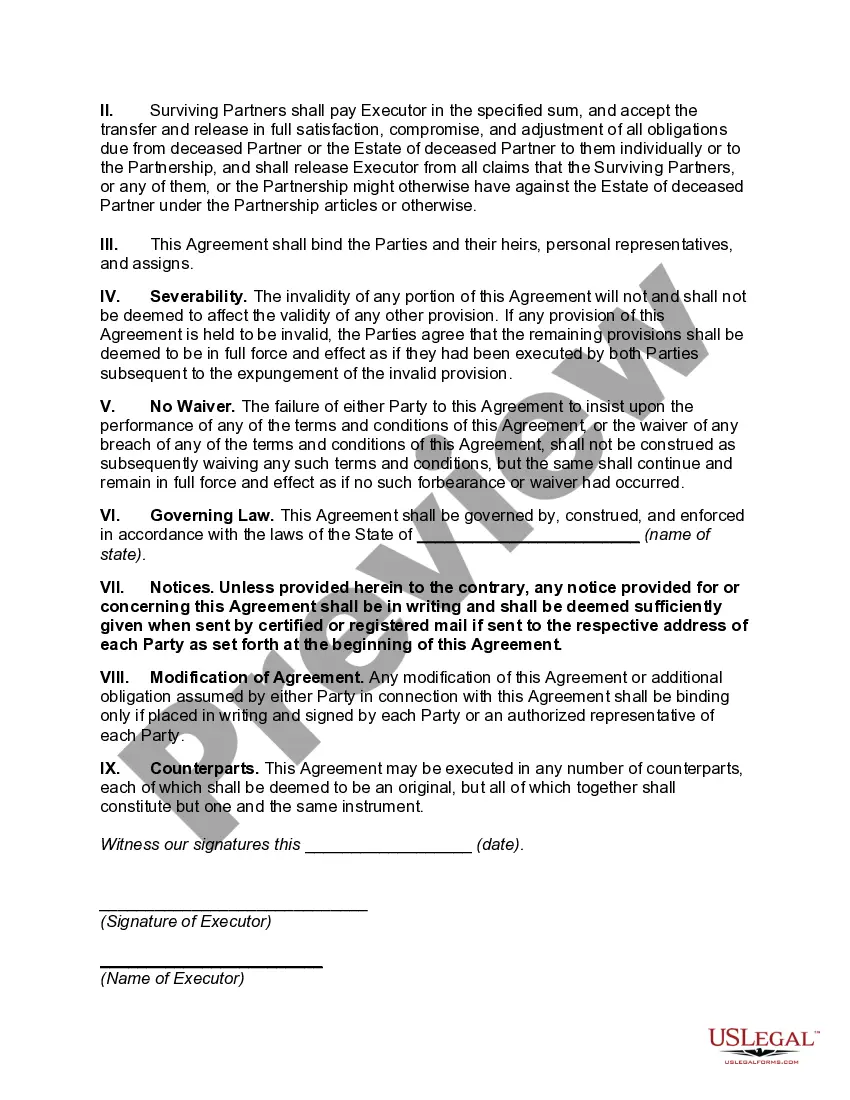

The Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner is a legal document that outlines the process of terminating a partnership and distributing its assets and liabilities when one of the partners passes away. This agreement is crucial in ensuring a smooth and fair dissolution of the partnership. There are various types of Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner, including: 1. General Partnership Agreement: This is the most common type of partnership, where all partners share equal rights and responsibilities. The Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner for a general partnership will outline how the surviving partners will settle the deceased partner's share in the business and allocate the remaining assets. 2. Limited Partnership Agreement: In a limited partnership, there are both general partners who have management control and limited partners who primarily provide capital. The Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner for a limited partnership will address the distribution of assets and liabilities considering the different roles and rights of each partner. 3. Limited Liability Partnership Agreement: This type of partnership provides liability protection to partners, similar to a corporation. When a partner in a limited liability partnership passes away, the Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner will lay out the process of settling the deceased partner's interest without affecting the other partners' limited liability protection. In the Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner, various key elements and clauses must be included. These include: 1. Identification of the partnership: The agreement should clearly state the name of the partnership, along with the date it was formed and the names of the partners involved. 2. Dissolution: The agreement should specify that the partnership is being dissolved due to the death of one of the partners. 3. Distribution of assets and liabilities: It is important to detail how the partnership's assets and liabilities will be distributed among the surviving partners and the estate of the deceased partner. This may involve selling off assets, settling outstanding debts, and allocating remaining profits or losses. 4. Buyout provisions: If the surviving partners wish to buy out the deceased partner's share in the partnership, provisions for a fair valuation and payment terms should be included in the agreement. 5. Tax implications: It is essential to address any tax implications that may arise from the dissolution of the partnership, including potential capital gains or losses. 6. Dispute resolution: In the event of any disputes arising during the process of dissolving the partnership, the agreement should outline a suitable method for resolving these issues, such as mediation or arbitration. 7. Governing law: The Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner should clearly state that it is governed by the laws of the state of Indiana. When entering into an Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner, it is advisable to seek legal counsel to ensure compliance with all applicable laws and to customize the agreement according to the specific needs and circumstances of the partnership.

Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner

Description

How to fill out Indiana Agreement To Dissolve And Wind Up Partnership Between Surviving Partners And Estate Of Deceased Partner?

Have you been in a position where you need papers for sometimes company or personal uses nearly every day time? There are a variety of legitimate papers templates available online, but locating ones you can rely on isn`t straightforward. US Legal Forms offers a huge number of type templates, such as the Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner, that are composed to satisfy federal and state demands.

In case you are already acquainted with US Legal Forms internet site and also have a merchant account, just log in. After that, you are able to obtain the Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner format.

Should you not come with an bank account and want to begin using US Legal Forms, adopt these measures:

- Get the type you want and ensure it is for your proper town/county.

- Make use of the Preview key to analyze the shape.

- Look at the information to ensure that you have chosen the correct type.

- In the event the type isn`t what you are trying to find, use the Research industry to get the type that meets your needs and demands.

- When you get the proper type, click Get now.

- Choose the prices plan you would like, fill out the specified information and facts to generate your account, and buy the order using your PayPal or Visa or Mastercard.

- Pick a handy paper formatting and obtain your backup.

Find all the papers templates you might have bought in the My Forms food selection. You can obtain a further backup of Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner anytime, if required. Just select the necessary type to obtain or printing the papers format.

Use US Legal Forms, by far the most comprehensive selection of legitimate kinds, in order to save time and steer clear of mistakes. The services offers appropriately manufactured legitimate papers templates that can be used for a variety of uses. Produce a merchant account on US Legal Forms and begin generating your daily life a little easier.