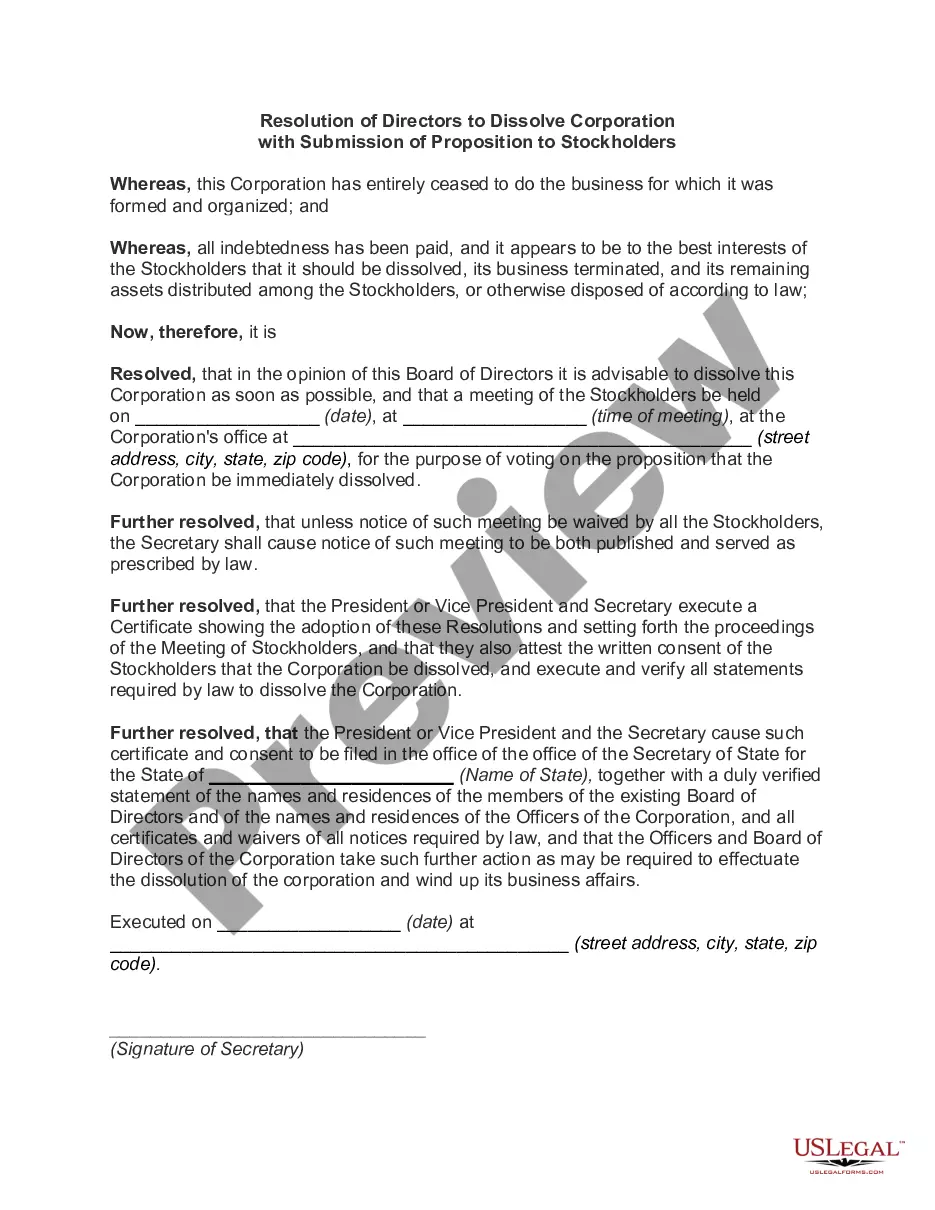

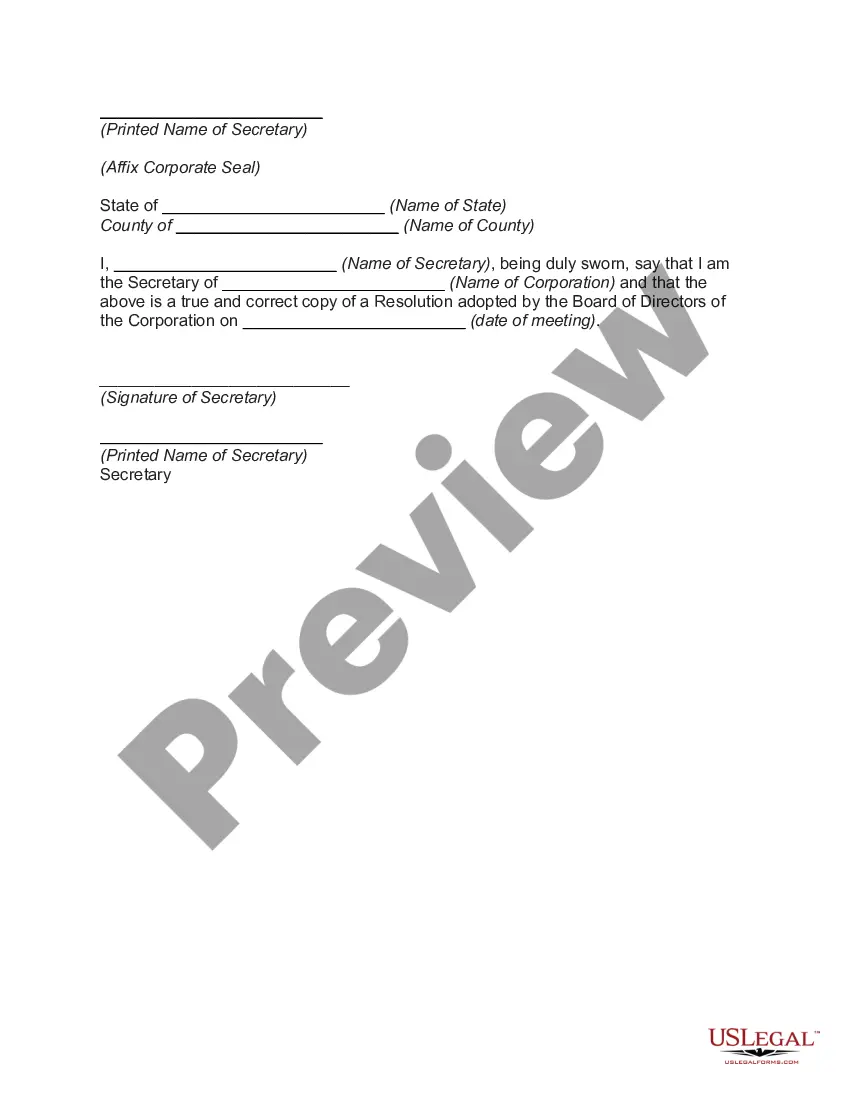

The Indiana Resolution of Directors to Dissolve Corporation with Submission of Proposition to Stockholders is a legal process followed by corporations operating in the state of Indiana, USA, to officially dissolve their company. This detailed description will outline the essential elements and steps involved in this dissolution process, covering important keywords related to this topic. 1. Indiana Corporation Dissolution: The Indiana Resolution of Directors to Dissolve Corporation is a legally required procedure that allows a corporation to wind up its affairs, liquidate its assets, and ultimately dissolve according to the state's laws. 2. Board of Directors Resolution: The dissolution process begins when the corporation's board of directors passes a resolution to dissolve the company. This resolution signifies the board's unanimous decision and intent to dissolve the corporation. 3. Submission of Proposition to Stockholders: After the board has approved the dissolution, the proposition is then presented to the corporation's stockholders for their review and voting. The proposition outlines the reasons, plans, and details surrounding the dissolution, such as the timeline, distribution of assets, and termination of operations. 4. Majority Stockholder Approval: For the dissolution proposition to move forward, a designated percentage of stockholders, typically a majority or super majority, must approve the proposal. This ensures that the decision to dissolve the corporation reflects the will of the majority of stockholders. 5. Alternative Types of Indiana Resolution of Directors to Dissolve Corporation: — Voluntary Dissolution: This occurs when the board and stockholders decide mutually to dissolve the corporation due to various reasons, such as poor financial performance, strategic changes, or retiring directors. — Involuntary Dissolution: This happens when a corporation is forced to dissolve by the state due to non-compliance with legal requirements, failure to pay taxes, or significant legal violations. 6. Distribution of Assets and Liabilities: Once the proposition is approved, the corporation must handle the distribution of its remaining assets and settle any outstanding liabilities. This includes paying off debts, resolving pending legal matters, and distributing remaining funds or assets among stockholders as per their ownership interests. 7. Termination of Business Operations: During the dissolution process, the corporation halts its business operations, settles any open contracts or agreements, cancels licenses and permits, and notifies vendors, customers, and other relevant parties about the company's impending dissolution. 8. Legal Filings and Compliance Requirements: Throughout the dissolution process, the corporation must meet various legal obligations, such as filing the appropriate dissolution paperwork with the Indiana Secretary of State's office, providing financial reports, and fulfilling tax-related obligations. Failure to comply with these requirements can lead to penalties or legal consequences. Remember, seeking professional legal advice is crucial when navigating the Indiana Resolution of Directors to Dissolve Corporation process. This guide offers a broad overview of the topic, but specific circumstances may require tailored actions and adherence to Indiana state laws.

Indiana Resolution of Directors to Dissolve Corporation with Submission of Proposition to Stockholders

Description

How to fill out Indiana Resolution Of Directors To Dissolve Corporation With Submission Of Proposition To Stockholders?

US Legal Forms - one of several most significant libraries of legal varieties in the States - delivers a wide array of legal papers web templates you can acquire or printing. Using the website, you can get a large number of varieties for company and person purposes, sorted by classes, says, or key phrases.You can get the most up-to-date types of varieties like the Indiana Resolution of Directors to Dissolve Corporation with Submission of Proposition to Stockholders within minutes.

If you already have a subscription, log in and acquire Indiana Resolution of Directors to Dissolve Corporation with Submission of Proposition to Stockholders from the US Legal Forms collection. The Download option can look on every single develop you view. You gain access to all in the past acquired varieties from the My Forms tab of your own account.

In order to use US Legal Forms the very first time, allow me to share basic guidelines to help you get started out:

- Be sure you have chosen the correct develop to your area/area. Go through the Preview option to analyze the form`s content material. Browse the develop description to actually have chosen the right develop.

- When the develop does not fit your needs, utilize the Search field on top of the monitor to get the one that does.

- If you are content with the shape, confirm your choice by clicking on the Purchase now option. Then, pick the prices program you like and give your qualifications to sign up on an account.

- Approach the deal. Use your charge card or PayPal account to accomplish the deal.

- Find the format and acquire the shape on your system.

- Make adjustments. Fill up, revise and printing and indicator the acquired Indiana Resolution of Directors to Dissolve Corporation with Submission of Proposition to Stockholders.

Each template you included in your bank account lacks an expiration day and is the one you have eternally. So, if you would like acquire or printing another copy, just proceed to the My Forms segment and click in the develop you need.

Obtain access to the Indiana Resolution of Directors to Dissolve Corporation with Submission of Proposition to Stockholders with US Legal Forms, the most comprehensive collection of legal papers web templates. Use a large number of expert and state-particular web templates that meet your organization or person requires and needs.