Indiana Checklist for Proving Entertainment Expenses

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Checklist For Proving Entertainment Expenses?

Are you in a scenario where you need documents for either business or personal reasons almost daily? There are numerous legitimate form templates accessible online, but finding ones you can trust is challenging.

US Legal Forms offers thousands of template forms, including the Indiana Checklist for Documenting Entertainment Expenditures, designed to meet state and federal requirements.

If you are already acquainted with the US Legal Forms website and possess an account, simply sign in. After that, you can download the Indiana Checklist for Documenting Entertainment Expenditures template.

- Select the form you need and verify it is for your specific city/state.

- Utilize the Review feature to evaluate the document.

- Examine the description to confirm that you have chosen the correct form.

- If the form does not meet your requirements, use the Search box to find the form that fits your needs and preferences.

- Once you locate the correct form, click Get now.

- Choose the pricing plan you want, enter the necessary information to set up your account, and pay for the order using your PayPal or credit card.

- Select a convenient format and download your copy.

Form popularity

FAQ

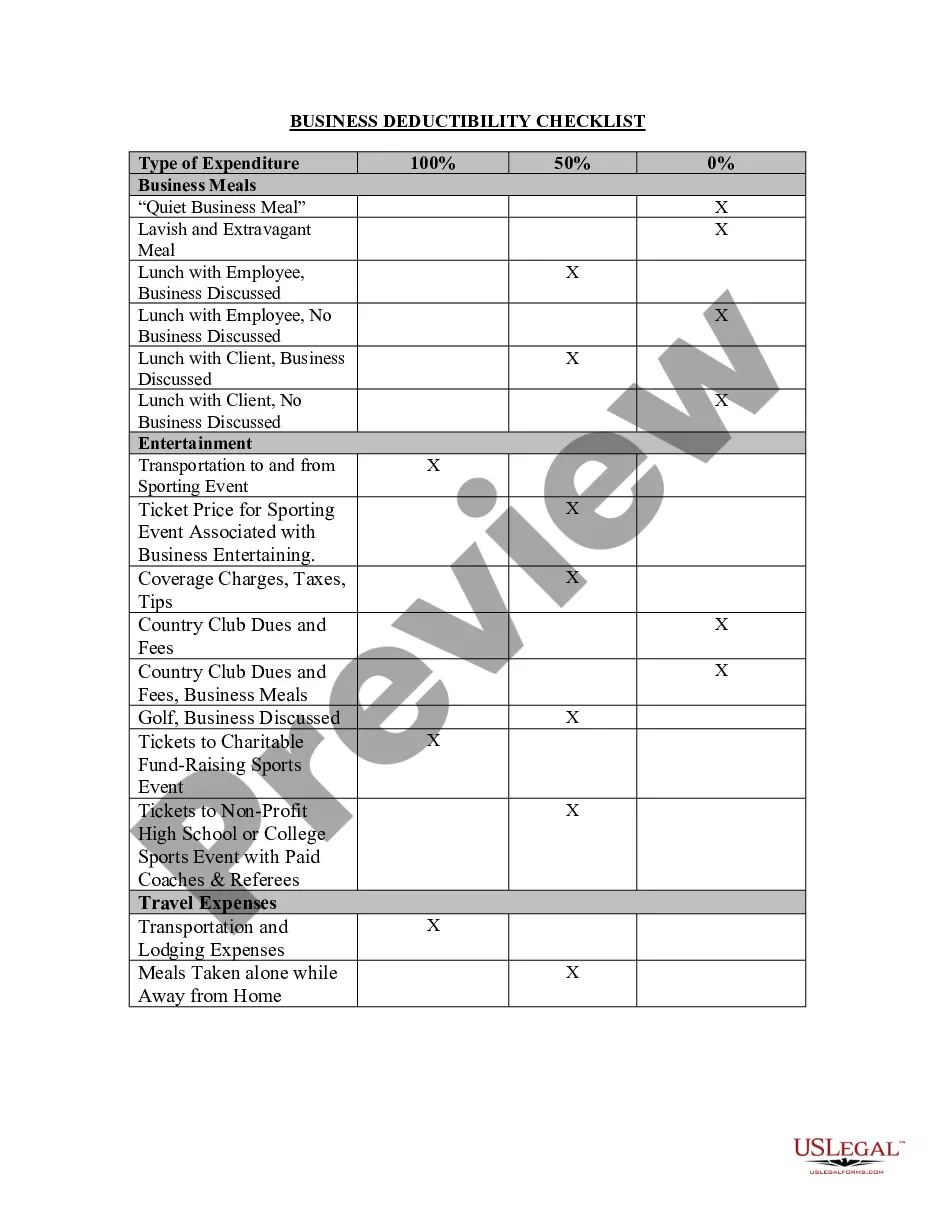

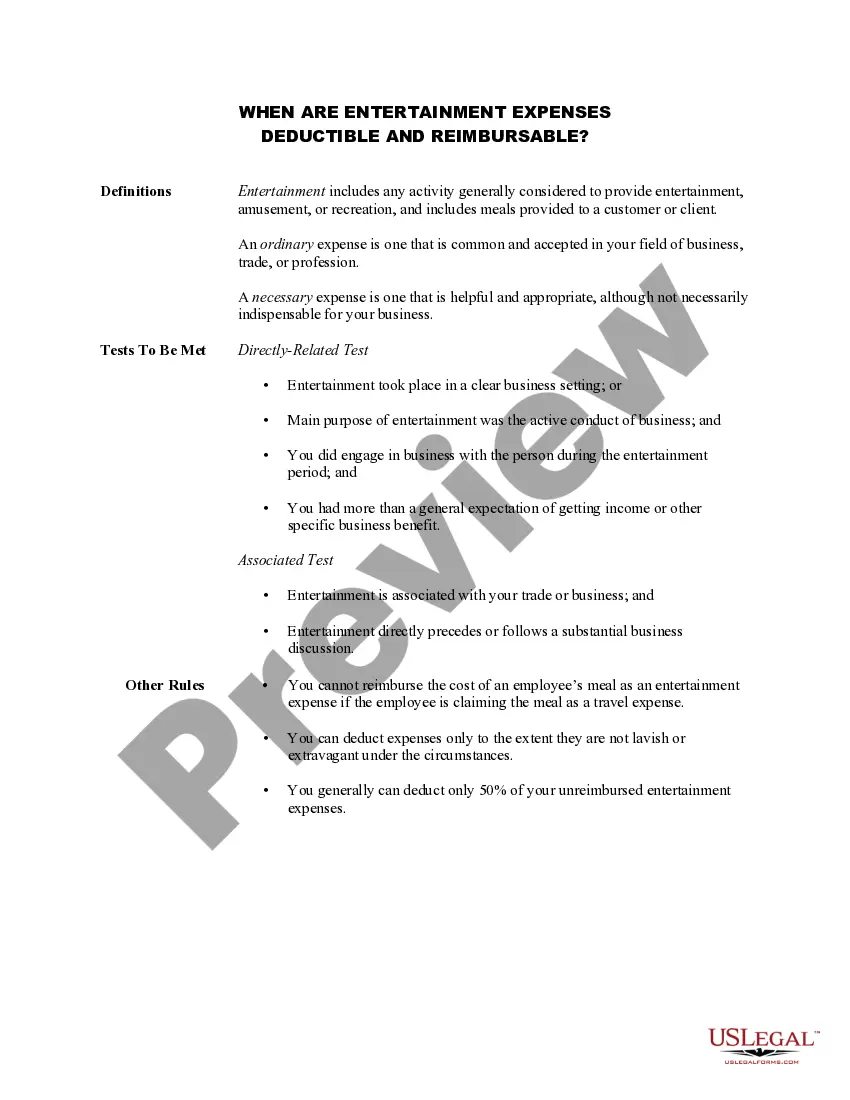

Entertainment expenses include the cost of meals you provide to customers or clients, whether the meal alone is the entertainment or it's a part of other entertainment (for example, refreshments at a football game). A meal expense includes the cost of food, beverages, taxes, and tips.

Entertainment expenses, like a sporting event or tickets to a show, are still non-deductible. However, team-building activities for employees are deductible.

Tax relief for staff entertainingStaff entertaining is generally considered to be an allowable business expense and is therefore tax deductible. Allowable costs in this context include food, drink, entertainment, venue hire, transport and overnight accommodation.

Generally, the IRS doesn't allow business to deduct costs for activities generally considered entertainment, amusement, or recreation, or for a facility used in connection with such activity. Taking a client or customer 200bto an "experience" is no longer deductible.

The 2018 Tax Cuts and Jobs Act brought a few big changes to meals and entertainment deductions. The biggest one: entertainment expenses are no longer deudctible.

Anything considered to constitute entertainment, amusement, or recreation is nondeductible, including the cost of facilities used in connection with these activities. This is unchanged from 2018 tax reform.

If you have to pay FBT on the entertainment expense, then you can claim it as a business expense and it will reduce your taxable income. If you do not pay FBT on your entertainment expense, you cannot claim it as a business expense and therefore cannot use it to reduce your taxable income.

Businesses will be permitted to fully deduct business meals that would normally be 50% deductible. Although this change will not affect your 2020 tax return, the savings will offer a 100% deduction in 2021 and 2022 for food and beverages provided by a restaurant.

Here are some common examples of 100% deductible meals and entertainment expenses:A company-wide holiday party.Food and drinks provided free of charge for the public.Food included as taxable compensation to employees and included on the W-2.

As part of the 2018 tax reform created by the Tax Cuts and Jobs Act (TCJA), Congress made several significant changes to the deductions for meals, entertainment, and employee fringe benefits, including making business entertainment expenses entirely nondeductible and reducing the deduction for most meals to 50%.