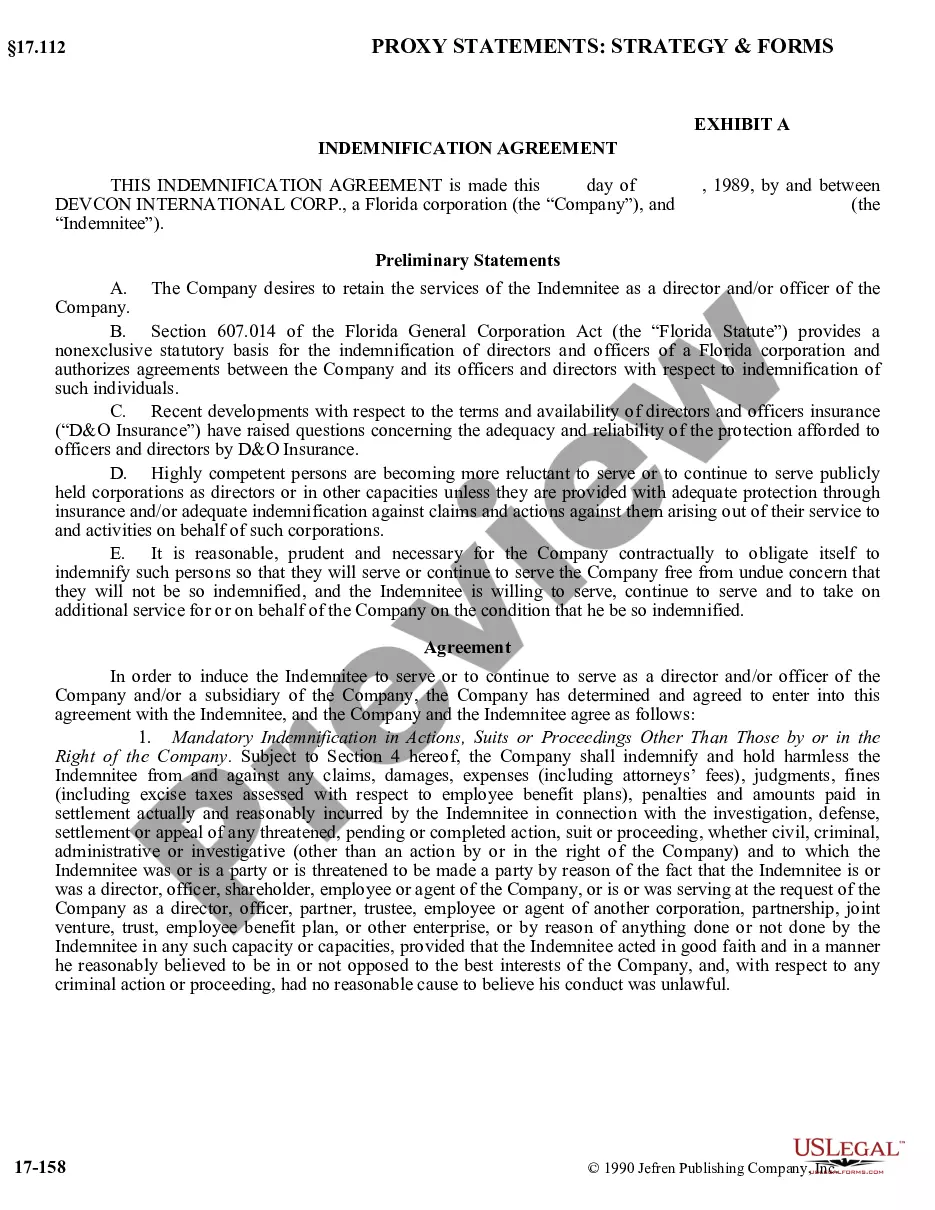

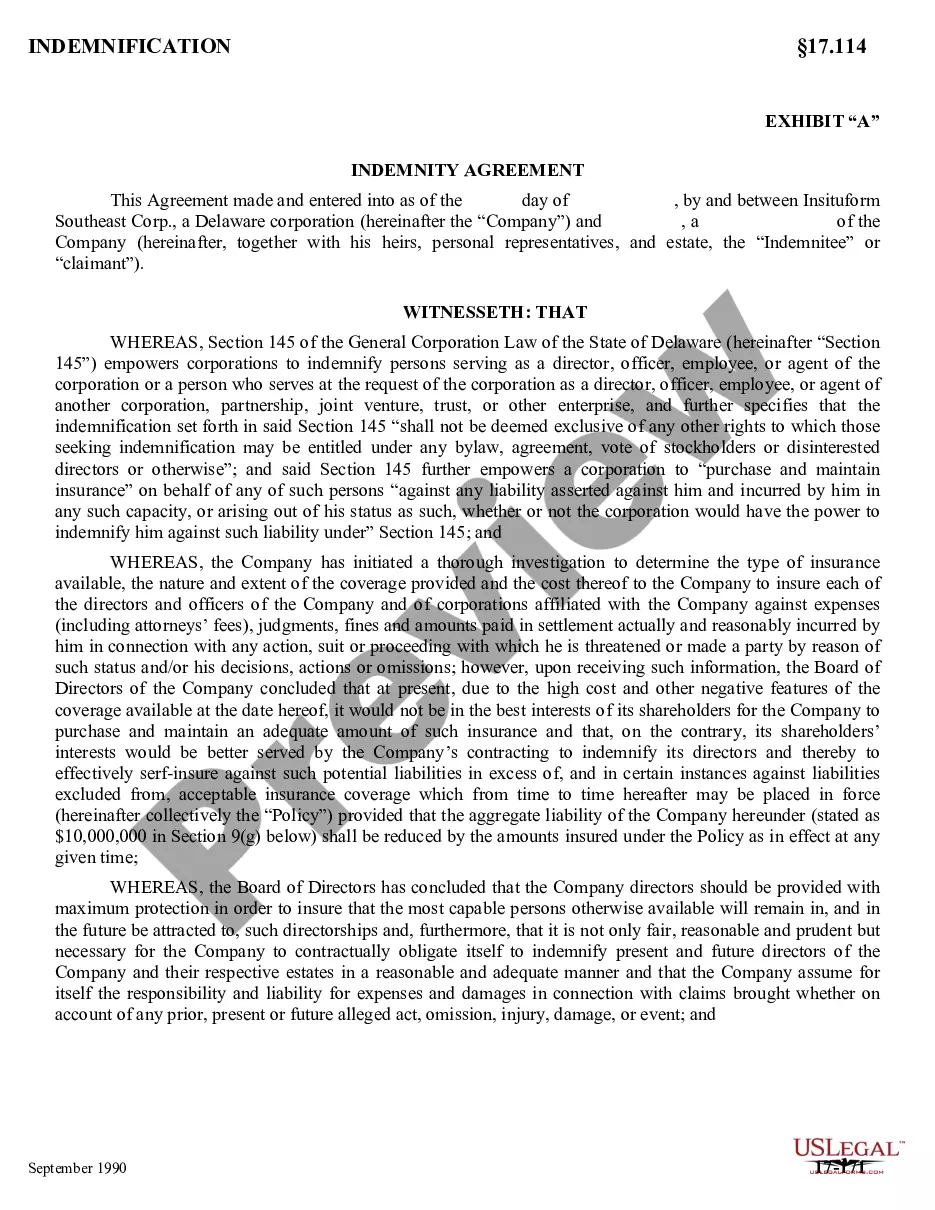

17-197C 17-197C . . . Indemnification Agreement to be entered into between corporation and its current and future directors and such current and future officers and other agents as directors may designate. The proposal includes description of procedural and substantive matters in Indemnification Agreements that are not addressed, or are addressed in less detail, in California law

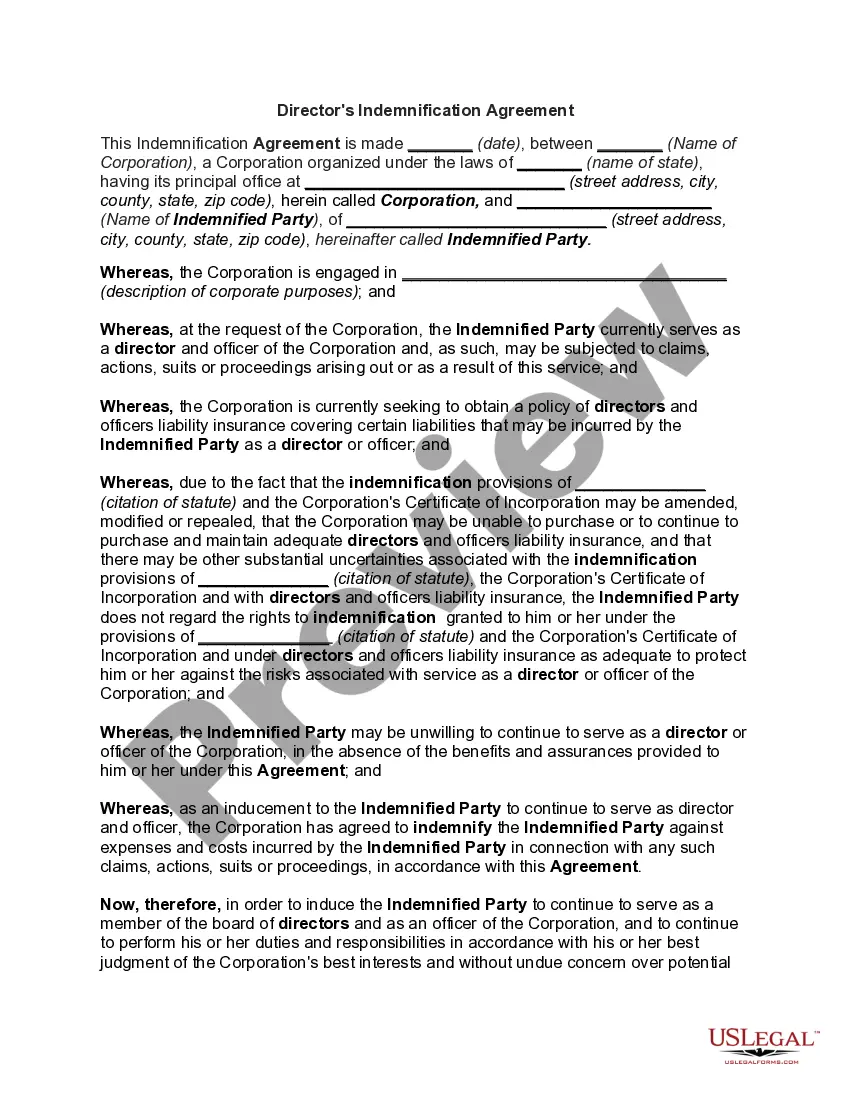

Indiana Indemnification Agreement between corporation and its current and future directors

Category:

State:

Multi-State

Control #:

US-CC-17-197C

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Indemnification Agreement Between Corporation And Its Current And Future Directors?

Are you in a situation the place you will need paperwork for sometimes enterprise or person reasons nearly every day? There are plenty of legal record templates accessible on the Internet, but discovering kinds you can rely is not easy. US Legal Forms provides thousands of type templates, like the Indiana Indemnification Agreement between corporation and its current and future directors, that happen to be published to satisfy state and federal demands.

In case you are currently acquainted with US Legal Forms web site and have your account, just log in. Afterward, you may acquire the Indiana Indemnification Agreement between corporation and its current and future directors web template.

Should you not come with an profile and need to begin to use US Legal Forms, abide by these steps:

- Find the type you will need and make sure it is for your right area/region.

- Make use of the Preview button to analyze the shape.

- See the description to actually have selected the right type.

- In the event the type is not what you`re seeking, utilize the Lookup field to find the type that suits you and demands.

- Once you discover the right type, click on Buy now.

- Pick the prices program you would like, fill out the necessary information to create your money, and pay money for your order utilizing your PayPal or charge card.

- Select a hassle-free data file file format and acquire your copy.

Get all the record templates you possess bought in the My Forms food selection. You may get a more copy of Indiana Indemnification Agreement between corporation and its current and future directors anytime, if needed. Just click the required type to acquire or print out the record web template.

Use US Legal Forms, by far the most substantial collection of legal varieties, in order to save time as well as prevent blunders. The assistance provides skillfully manufactured legal record templates that can be used for a range of reasons. Generate your account on US Legal Forms and initiate making your daily life a little easier.

Form popularity

FAQ

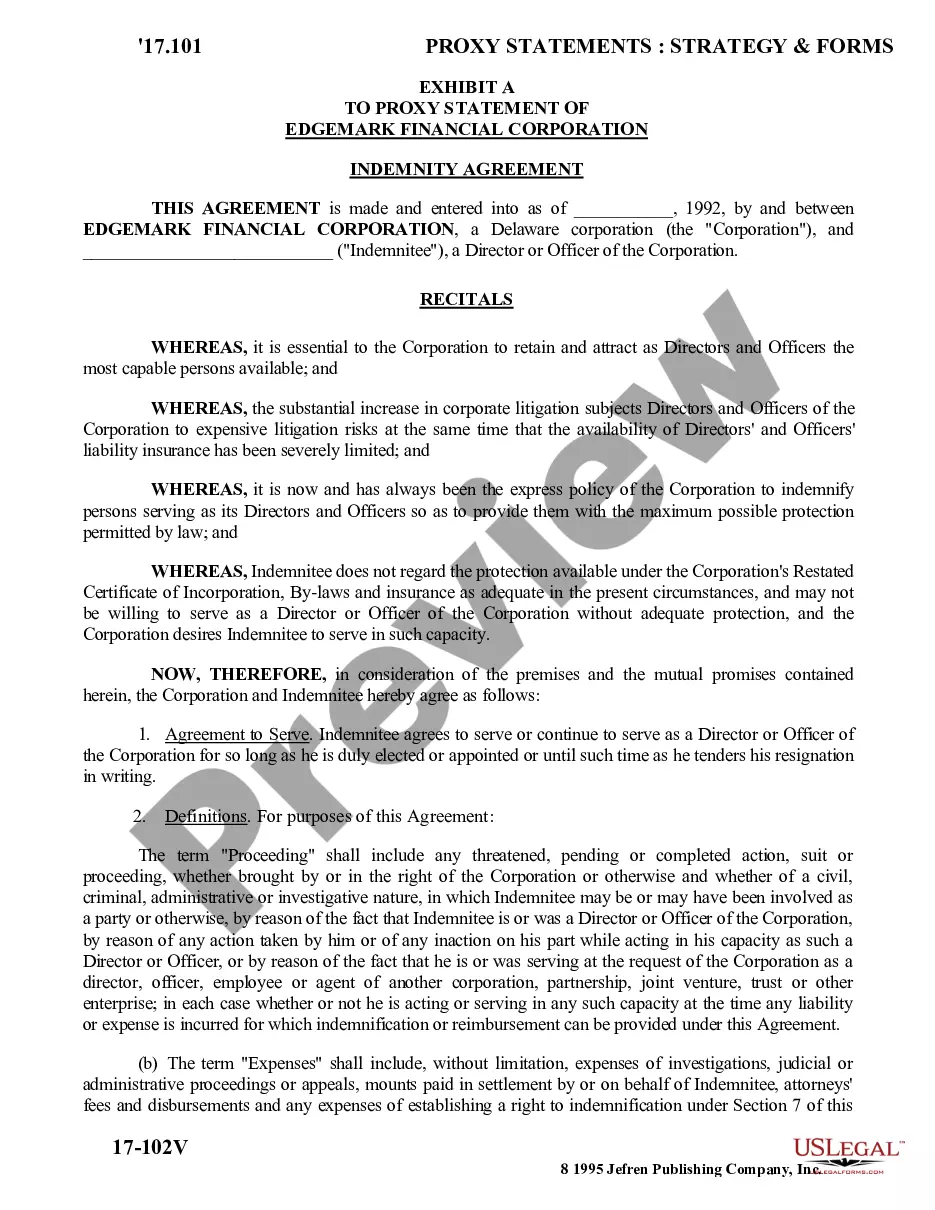

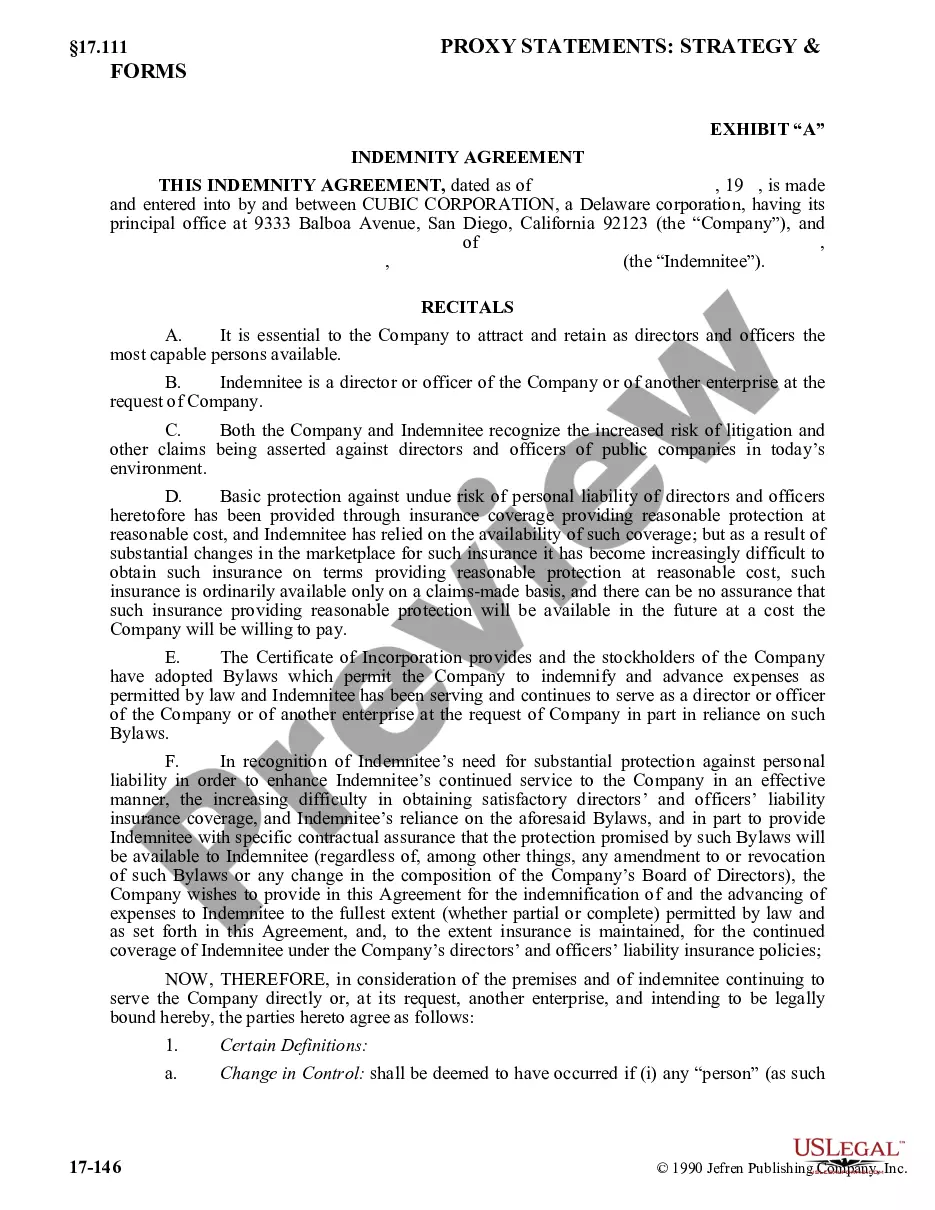

The Certificate of Incorporation (the ?Charter?) and the Bylaws (the ?Bylaws?) of the Company require indemnification of the officers and directors of the Company.

A company may, however, lend money to a director to fund the director's defence costs. Frequently, an indemnity will include a provision under which the company agrees to lend the director the amounts necessary to fund the director's defence costs.

Indemnification is, generally speaking, a reimbursement by a company of its Ds&Os for expenses or losses they have incurred in connection with litigation or other proceedings relating to their service to the company.

Section 145(b) empowers a corporation to indemnify its directors against expenses incurred in connection with the defense or settlement of an action brought by or in the right of the corporation, subject to the standard of conduct determination, and except that no indemnification may be made as to any claim to which ...

In the indemnification agreement, the corporation agrees to reimburse the director or officer for losses incurred in legal proceedings related to their service as a corporate director or officer to the maximum extent permitted by law.

A legal term that means one party agrees to compensate another party for loss or damage that has already occurred, or guarantees, through a contractual agreement, to repay another party for loss or damage that occurs in the future. Indemnification clauses are common in corporations and LLCs.

A director and officer indemnification agreement is a contract that allows executives to protect themselves from claims made against them while performing job. Indemnification means that in the event a lawsuit is filed against a company, the indemnified party is "held harmless" from claims.

The official must agree to pay back the funds received if it is found they are not entitled to indemnification. Advancement ensures that company officials have the resources to resist unjustified lawsuits without relieving them of responsibility for any bad faith conduct established.