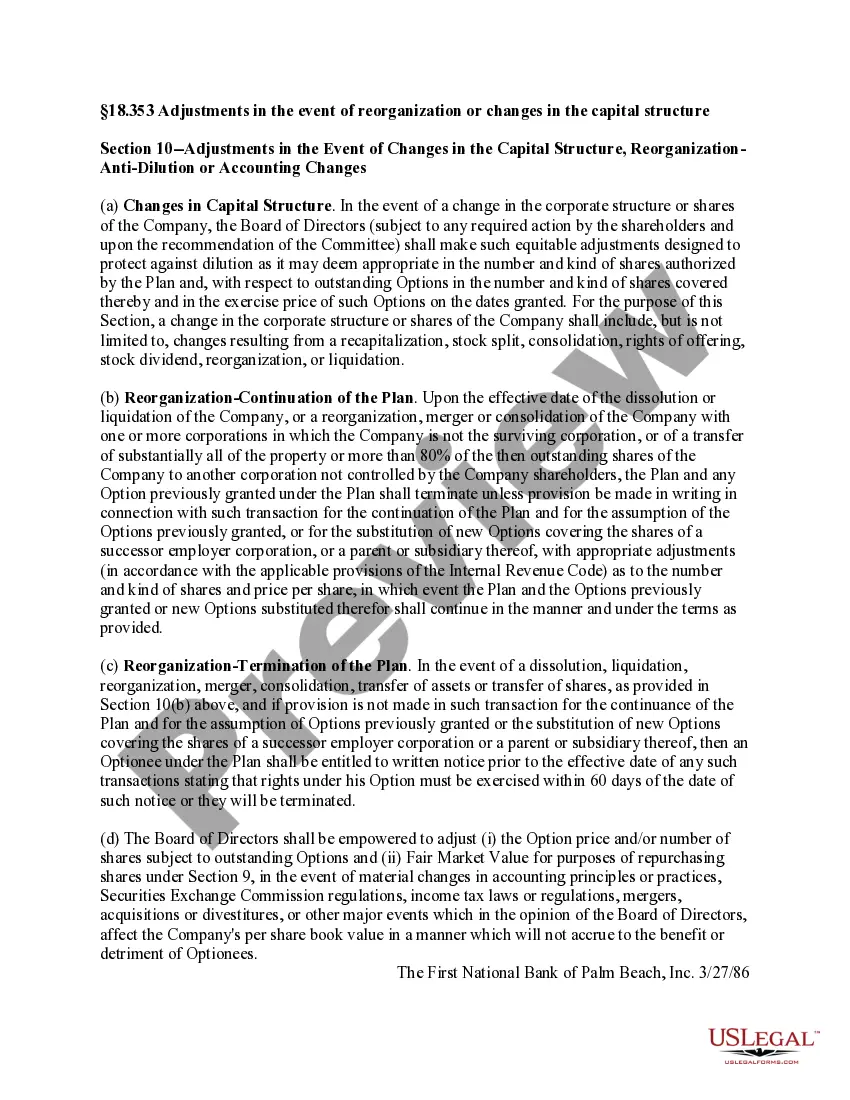

Indiana Adjustments refer to specific changes or modifications made in the event of reorganization or alterations in the capital structure of a business entity in the state of Indiana. These adjustments are integral to ensuring compliance with the state's corporate laws and regulations while managing the financial aspects of a company's restructuring. When a business undergoes reorganization or experiences changes in its capital structure, it may need to undertake the following types of Indiana Adjustments: 1. Conversion Adjustments: Conversion adjustments are made when a company converts its existing securities or financial instruments from one form to another. For example, a company may convert its debt into equity or preferred shares into common shares during a reorganization process. Such conversions often aim to improve the company's financial position or align its capital structure with the changing business dynamics. 2. Stock Split or Reverse Stock Split Adjustments: A stock split or a reverse stock split adjustment occurs when a company decides to increase or decrease the number of outstanding shares it has in the market. A stock split involves proportionally increasing the number of shares outstanding, whereas a reverse stock split involves proportionally reducing the number of shares. The purpose of these adjustments is to adjust the per-share value of the stock and ensure liquidity in the market. 3. Merger or Acquisition Adjustments: When two companies combine through a merger or one company acquires another, various adjustments are required to harmonize their capital structures. These adjustments might involve restructuring debt, realigning equity stakes, or changing the ownership rights and preferences associated with different classes of shares. The objective is to integrate the entities seamlessly while maintaining legal compliance and maximizing synergies. 4. Recapitalization Adjustments: In certain situations, a company may undergo recapitalization to improve its financial structure, often by rebalancing its debt-to-equity ratio. Recapitalization adjustments may include issuing new debt instruments, repurchasing existing securities, or exchanging debt for equity. These adjustments aim to enhance financial stability, reduce interest costs, or address underperforming or unsustainable capital structures. 5. Dividend Adjustments: Changes in the capital structure may necessitate adjustments to dividend policies. For instance, a company experiencing financial distress might choose to suspend or reduce dividends to preserve cash flow or redirect funds towards debt repayment. Conversely, a company with a strengthened financial position might increase dividend payments to reward shareholders. These adjustments ensure that shareholder interests align with the company's financial goals. 6. Change in Voting Rights Adjustments: Re organizational changes can impact the voting rights associated with different classes of shares or securities. Adjustments in voting rights aim to maintain fairness and balance among shareholders in decision-making processes. For example, when a company issues new shares, existing shareholders may experience dilution of their voting power. Adjustments may be made to address such concerns and maintain equitable representation. By implementing these Indiana Adjustments while navigating reorganizations or capital structure changes, businesses can ensure legal and financial compliance while optimizing their operations for sustained growth and success. It is crucial to consult legal and financial professionals well-versed in Indiana corporate laws to manage these adjustments accurately and efficiently.

Indiana Adjustments refer to specific changes or modifications made in the event of reorganization or alterations in the capital structure of a business entity in the state of Indiana. These adjustments are integral to ensuring compliance with the state's corporate laws and regulations while managing the financial aspects of a company's restructuring. When a business undergoes reorganization or experiences changes in its capital structure, it may need to undertake the following types of Indiana Adjustments: 1. Conversion Adjustments: Conversion adjustments are made when a company converts its existing securities or financial instruments from one form to another. For example, a company may convert its debt into equity or preferred shares into common shares during a reorganization process. Such conversions often aim to improve the company's financial position or align its capital structure with the changing business dynamics. 2. Stock Split or Reverse Stock Split Adjustments: A stock split or a reverse stock split adjustment occurs when a company decides to increase or decrease the number of outstanding shares it has in the market. A stock split involves proportionally increasing the number of shares outstanding, whereas a reverse stock split involves proportionally reducing the number of shares. The purpose of these adjustments is to adjust the per-share value of the stock and ensure liquidity in the market. 3. Merger or Acquisition Adjustments: When two companies combine through a merger or one company acquires another, various adjustments are required to harmonize their capital structures. These adjustments might involve restructuring debt, realigning equity stakes, or changing the ownership rights and preferences associated with different classes of shares. The objective is to integrate the entities seamlessly while maintaining legal compliance and maximizing synergies. 4. Recapitalization Adjustments: In certain situations, a company may undergo recapitalization to improve its financial structure, often by rebalancing its debt-to-equity ratio. Recapitalization adjustments may include issuing new debt instruments, repurchasing existing securities, or exchanging debt for equity. These adjustments aim to enhance financial stability, reduce interest costs, or address underperforming or unsustainable capital structures. 5. Dividend Adjustments: Changes in the capital structure may necessitate adjustments to dividend policies. For instance, a company experiencing financial distress might choose to suspend or reduce dividends to preserve cash flow or redirect funds towards debt repayment. Conversely, a company with a strengthened financial position might increase dividend payments to reward shareholders. These adjustments ensure that shareholder interests align with the company's financial goals. 6. Change in Voting Rights Adjustments: Re organizational changes can impact the voting rights associated with different classes of shares or securities. Adjustments in voting rights aim to maintain fairness and balance among shareholders in decision-making processes. For example, when a company issues new shares, existing shareholders may experience dilution of their voting power. Adjustments may be made to address such concerns and maintain equitable representation. By implementing these Indiana Adjustments while navigating reorganizations or capital structure changes, businesses can ensure legal and financial compliance while optimizing their operations for sustained growth and success. It is crucial to consult legal and financial professionals well-versed in Indiana corporate laws to manage these adjustments accurately and efficiently.