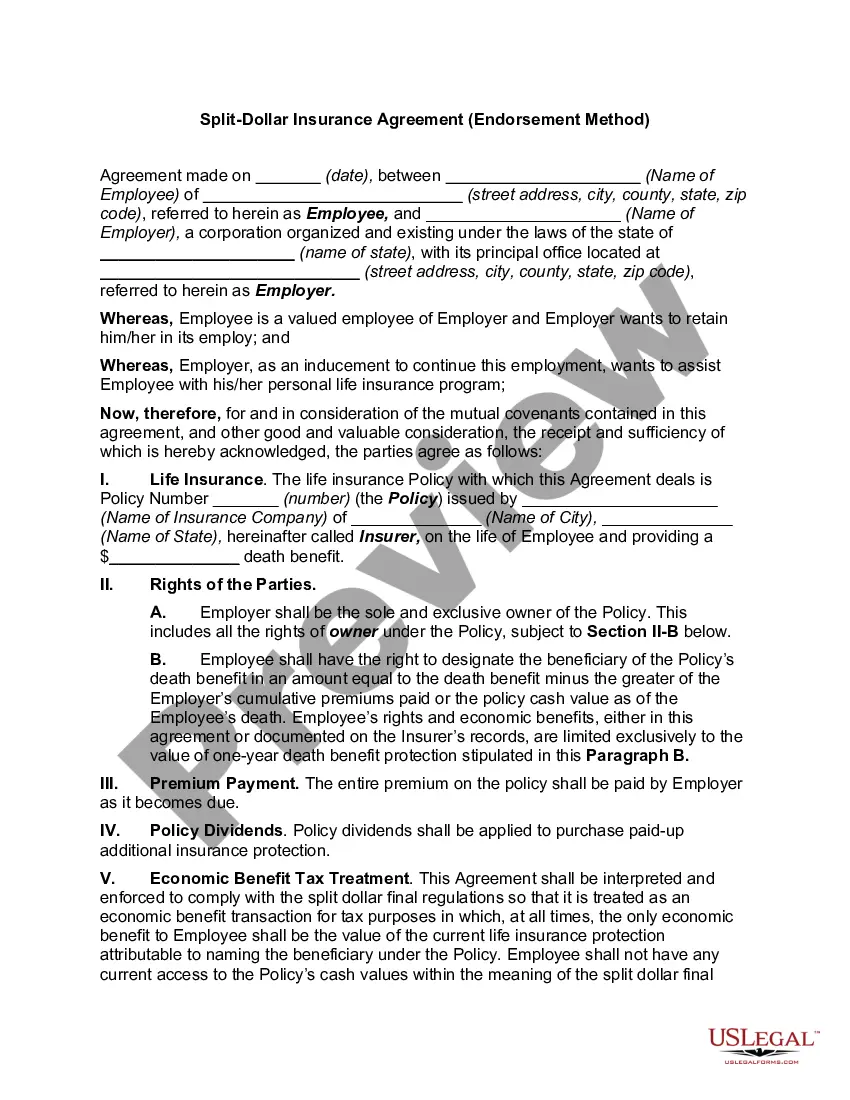

Indiana Split-Dollar Life Insurance

Description

How to fill out Split-Dollar Life Insurance?

Discovering the right legal document design could be a have difficulties. Of course, there are plenty of themes accessible on the Internet, but how would you obtain the legal type you need? Use the US Legal Forms web site. The support offers 1000s of themes, such as the Indiana Split-Dollar Life Insurance, that can be used for business and personal requirements. All of the kinds are examined by experts and meet federal and state needs.

Should you be presently listed, log in for your account and click on the Acquire key to have the Indiana Split-Dollar Life Insurance. Make use of your account to appear through the legal kinds you possess bought in the past. Visit the My Forms tab of your respective account and obtain an additional version of the document you need.

Should you be a whole new end user of US Legal Forms, here are simple recommendations that you can comply with:

- Very first, ensure you have chosen the right type for your metropolis/state. You can look through the form making use of the Preview key and browse the form explanation to make sure it is the right one for you.

- When the type will not meet your preferences, utilize the Seach industry to get the proper type.

- Once you are positive that the form is suitable, select the Acquire now key to have the type.

- Select the prices program you desire and enter in the needed information and facts. Build your account and pay money for your order utilizing your PayPal account or Visa or Mastercard.

- Opt for the document file format and download the legal document design for your system.

- Comprehensive, modify and print out and indication the obtained Indiana Split-Dollar Life Insurance.

US Legal Forms is definitely the most significant library of legal kinds for which you can discover a variety of document themes. Use the service to download expertly-made files that comply with status needs.

Form popularity

FAQ

If the employer is the owner of the split-dollar policy, the employer's premium payments are treated as providing taxable economic benefits to the executive. The economic benefits include the executive's interest in the policy's accessible cash value and current life insurance protection.

Split Dollar Loan Regime Agreement & Contract Generally, at the employee's death, the employer receives a portion of the death benefit (usually equal to the total premiums plus interest from the loan) and the employee's beneficiary receives the balance.

While split-dollar life insurance arrangements offer numerous advantages, they also come with potential drawbacks, such as complexity, tax considerations, and limited availability. Both employers and employees must carefully weigh the benefits and disadvantages of this type of arrangement before deciding to pursue it.

There is no cost to the employee-participant unless the policy is transferred to them. This endorsement split-dollar plan is most often used to provide a low-cost death benefit to the employee-participant as a fringe benefit or where the employer wishes to own the policy and/or obtain key person protection.

If you withdraw up to the amount of the total premiums paid into the policy, the transaction is not taxable as it is considered a return of premiums. If, however, you then withdraw any gains on the policy (like dividends), then these amounts could be taxed as ordinary income.

Answer: Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren't includable in gross income and you don't have to report them. However, any interest you receive is taxable and you should report it as interest received.

There is no cost to the employee-participant unless the policy is transferred to them. This endorsement split-dollar plan is most often used to provide a low-cost death benefit to the employee-participant as a fringe benefit or where the employer wishes to own the policy and/or obtain key person protection.

There are 2 types of split dollar plans. Collateral assignment / loan regime. Endorsement split dollar / economic benefit regime.