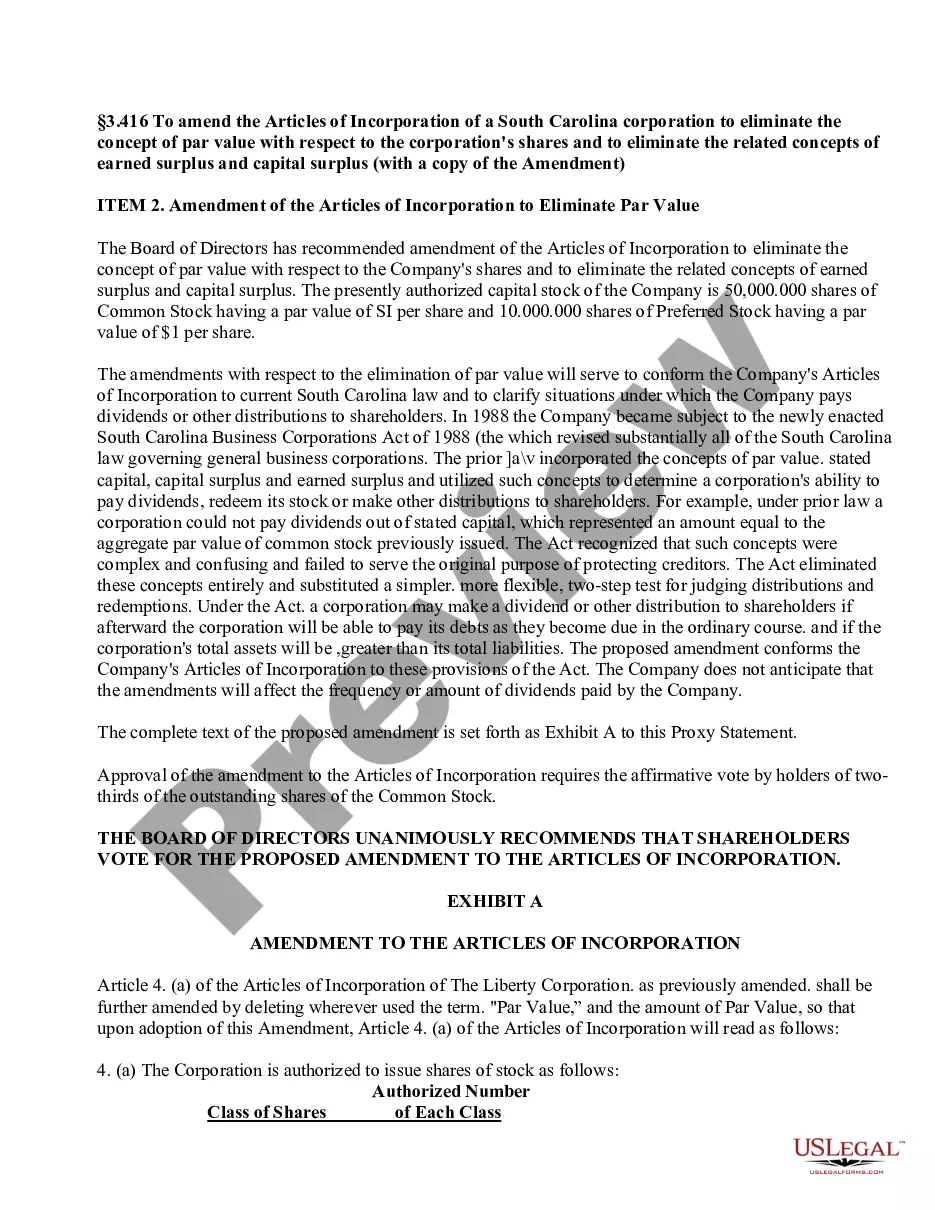

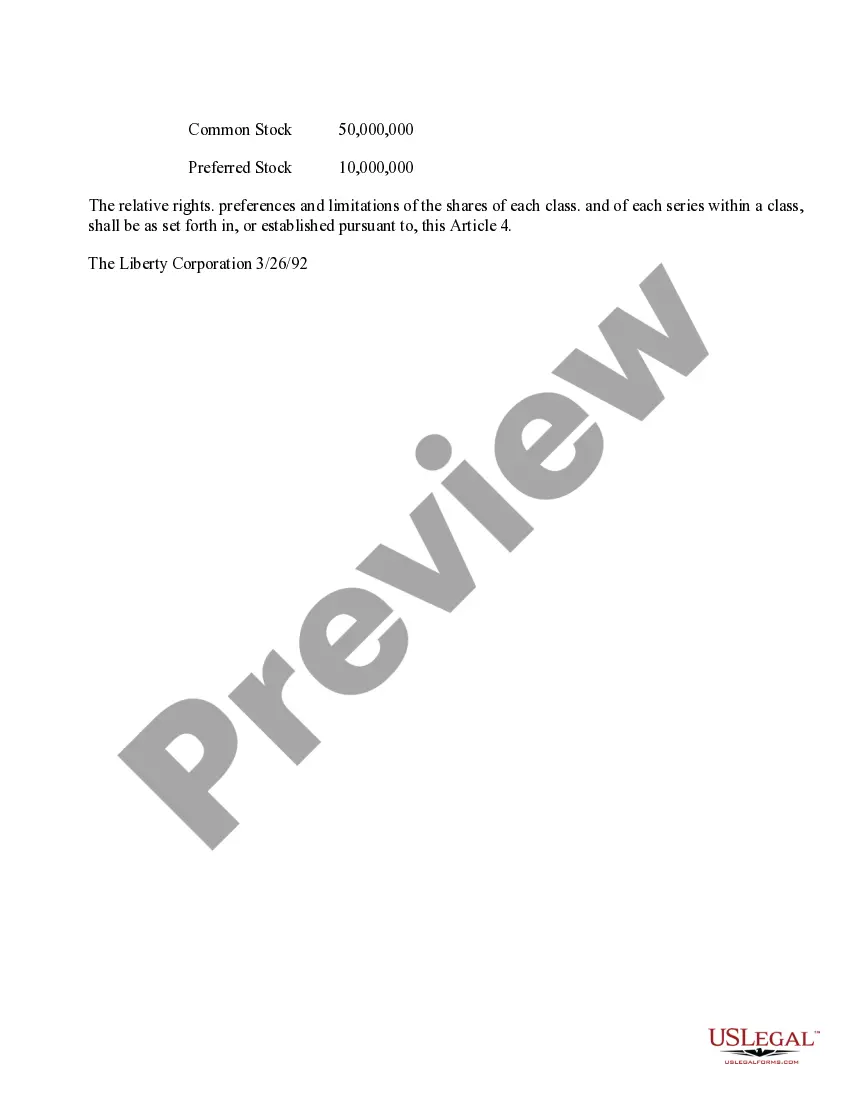

Indiana Amendment to the Articles of Incorporation to Eliminate Par Value: A Detailed Description In the state of Indiana, businesses have the option to file an Amendment to the Articles of Incorporation to eliminate par value for their corporation's shares. This amendment is a significant step for businesses looking to adjust the value of their shares or provide more flexibility in their corporate structure. In this article, we will provide a detailed description of this process, highlighting its importance, key features, and any variations or types of amendments related to eliminating par value. The concept of par value represents the minimum price at which shares are issued by a corporation. By eliminating par value, businesses gain the ability to issue shares with greater flexibility, allowing them to adjust the value of their shares based on market conditions or business requirements. An Indiana Amendment to the Articles of Incorporation serves as the legal instrument to modify the initial terms and conditions set forth in the original incorporation documents. To initiate the process of eliminating par value, a business in Indiana must draft an Amendment to the Articles of Incorporation. The amendment should include specific details regarding the decision to eliminate par value, such as the reasoning behind it and the impact it could have on the corporation. The amendment needs to be approved by the board of directors, and in some cases, by the shareholders, depending on the corporation's bylaws and the magnitude of the change. Once the board of directors has approved the amendment, it should be filed with the Indiana Secretary of State's office, typically accompanied by a filing fee. The Secretary of State will review the amendment to ensure compliance with state laws and regulations. If approved, the updated information will be reflected in the corporation's official record and the amended Articles of Incorporation will be issued. It is worth mentioning that there are variations or types of Indiana Amendments to the Articles of Incorporation related to eliminating par value that may be relevant to different situations or business needs. These may include: 1. General Elimination of Par Value Amendment: This is the most common type of amendment, where the par value is completely removed from the corporation's shares. It provides significant flexibility in setting the price of shares. 2. Partial Elimination of Par Value Amendment: In some cases, businesses may choose to eliminate par value for a particular class or series of shares, while maintaining it for others. This option can be beneficial for businesses wishing to differentiate various classes of shares based on specific rights or privileges. 3. Adoption of No-Par Stock Amendment: This type of amendment replaces the concept of par value with a no-par or no-stated value for all shares. It completely removes the requirement of assigning a minimum value to shares. In conclusion, the Indiana Amendment to the Articles of Incorporation to eliminate par value provides corporations with increased flexibility in setting the value of their shares. This process requires drafting a clear amendment, obtaining approval from the board of directors (and possibly shareholders) and filing the amendment with the Indiana Secretary of State. By eliminating par value, businesses can adapt to market conditions, attract investors, or adjust their corporate structure as needed. Different variations of this amendment exist, allowing businesses to tailor their decision based on specific requirements or differentiation among their shares.

Indiana Amendment to the articles of incorporation to eliminate par value

Description

How to fill out Indiana Amendment To The Articles Of Incorporation To Eliminate Par Value?

US Legal Forms - among the biggest libraries of lawful kinds in the States - gives a wide range of lawful document themes you may download or print out. Making use of the internet site, you may get a huge number of kinds for enterprise and person uses, sorted by groups, suggests, or search phrases.You will discover the latest models of kinds such as the Indiana Amendment to the articles of incorporation to eliminate par value in seconds.

If you already have a registration, log in and download Indiana Amendment to the articles of incorporation to eliminate par value from the US Legal Forms library. The Download button will appear on every single form you look at. You gain access to all earlier acquired kinds inside the My Forms tab of your account.

In order to use US Legal Forms the very first time, listed below are basic recommendations to help you started off:

- Ensure you have chosen the best form for your metropolis/state. Select the Review button to review the form`s information. Read the form description to ensure that you have selected the right form.

- In case the form does not suit your demands, make use of the Search discipline at the top of the display screen to discover the the one that does.

- Should you be happy with the form, confirm your selection by clicking the Buy now button. Then, select the costs program you prefer and provide your accreditations to register on an account.

- Approach the deal. Make use of charge card or PayPal account to accomplish the deal.

- Pick the formatting and download the form on the device.

- Make changes. Complete, revise and print out and indication the acquired Indiana Amendment to the articles of incorporation to eliminate par value.

Every single format you included in your bank account does not have an expiry particular date and is your own property permanently. So, if you would like download or print out yet another backup, just check out the My Forms section and click on on the form you will need.

Obtain access to the Indiana Amendment to the articles of incorporation to eliminate par value with US Legal Forms, by far the most considerable library of lawful document themes. Use a huge number of professional and express-particular themes that fulfill your organization or person requires and demands.

Form popularity

FAQ

The par value, or face value, is the stated value per share. This price was printed on paper stock certificates before they became antiquated for newer electronic versions. If a company did not set a par value, its certificates were issued as no-par value stocks.

Authorized Stock: the number of shares that a corporation's charter allows it to sell.

Authorized Stock Authorized Stock - is the maximum amount of stock that the company is allowed to issue as per mentioned the company charter. Common Stock: is a security that represents ownership?

?Authorized shares? refers to the number of shares the corporation is allowed to issue under its certificate or articles of incorporation. 10 to 15 million is a commonly used range (we set 10 million as default for the Cooley GO Docs Incorporation Package).

What Is the Difference Between Authorized Shares and Issued Shares? Authorized shares are the maximum number of shares that can legally be issued to shareholders. This number is established by the company's articles of incorporation. Issued shares are the number of shares actually given to shareholders.

Authorized Stock: the number of shares that a corporation's charter allows it to sell.

A corporation's business and affairs are managed by or under the direction of its board of directors. Although the board has the power to make all decisions on behalf of its corporation, many business decisions are actually made by the corporation's officers.

Articles of Incorporation refers to the highest governing document in a corporation. It is also known known as the corporate charter. The Articles of Incorporation generally include the purpose of the corporation, the type and number of shares, and the process of electing a board of directors.